Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please see the attached photos containing a case study go White Hen Pantry inc. Answer the questions following the case description. It is an APV

please see the attached photos containing a case study go White Hen Pantry inc. Answer the questions following the case description. It is an APV valuation of a leveraged buyout. thank you.

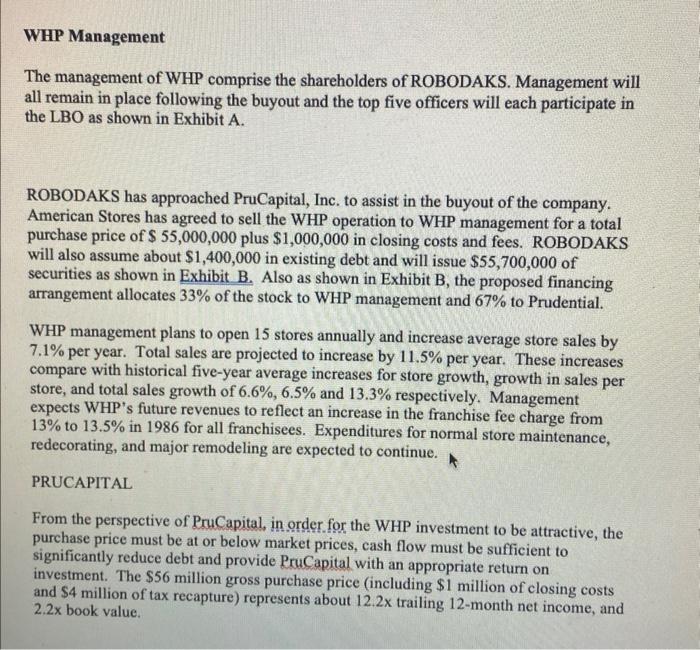

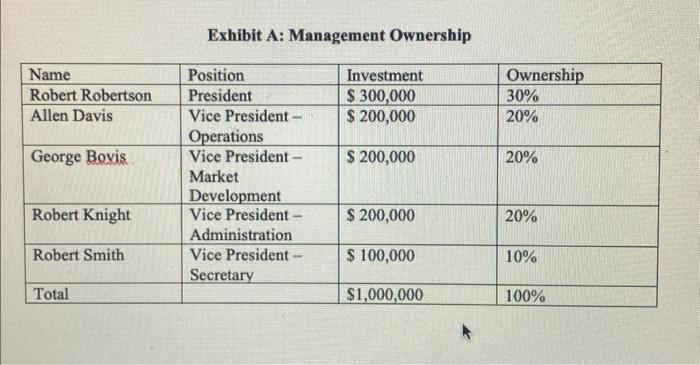

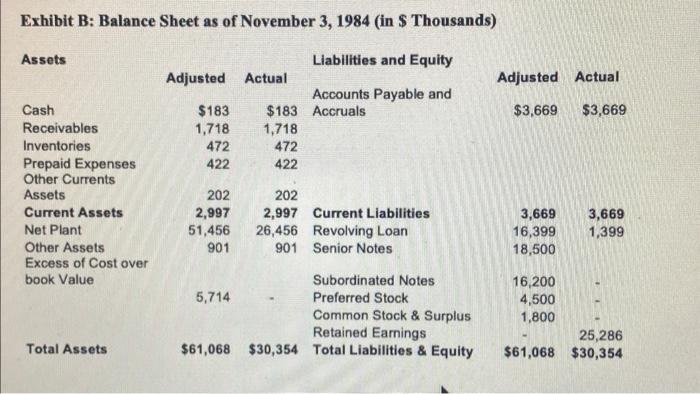

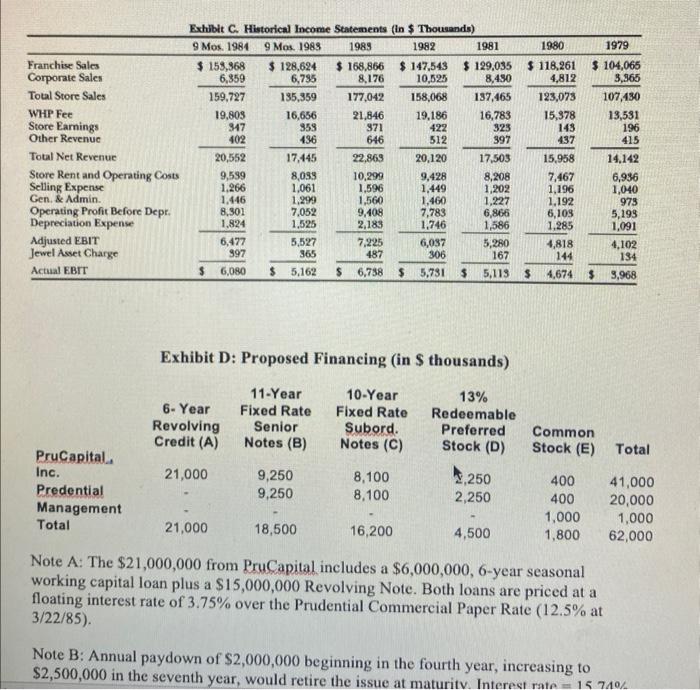

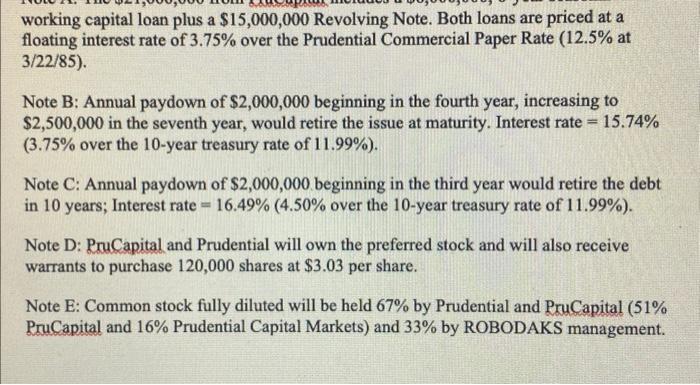

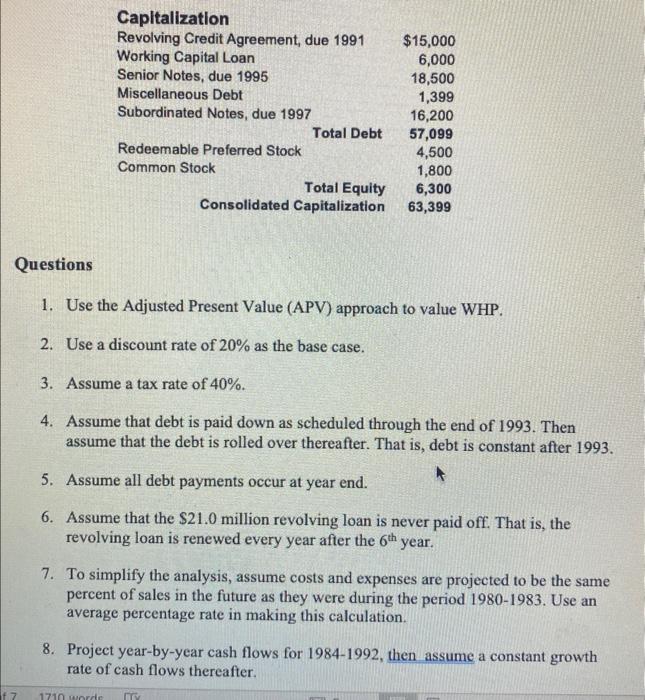

The Management Buyout of Whit Hen Pantry, Inc. Abstract Management of White Hen Pantry, a subsidiary of Jewel Stores, undertook a leveraged buyout of the subsidiary in 1985 with the assistance of PruCapital. The case focuses on the valuation of the subsidiary and the structure of the financing of the transaction. Introduction In February 1985, management of White Hen Pantry (WHP), led by its President Bob Robertson, is considering buying the company from its parent, Jewel Companies, Inc., for \$55 million. The management group has formed a company named ROBODAKS for the purposes of buying WHP. After the transaction, the company will retain the name White Hen Pantry. The leveraged buyout (LBO) is to be financed largely with loans made by PruCapital, Inc., a financing unit of Prudential Insurance Company of America. Among the issues to be considered are the price of the company and the structure of the financial agreement. American Stores acquired Jewel Cos. (Jewel) in a hostile takeover in June of 1984 in a transaction valued at nearly $1.2 billion. This acquisition created the nation's thirdlargest drug and supermarket retailing chain. American Stores has decided to sell certain units of Jewel including WHP to reduce its debt and to concentrate on drug store supermarket retailing. Franchise Arrangement WHP operates a chain of 317 convenience stores, 302 of which are franchise stores and 15 of which are operated by WHP. These stores average approximately 2,500 square feet in size, offer up-front parking, and are generally open 24 hours a day. WHP stores offer a broad array of grocery items and high quality items in delicatessen products, fresh baked goods and produce. WHP is the only company among the industry's top 50 that does not sell gas. Management strongly believes this policy contributes to a higher quality image and helps attract a broader group of customers. Franchise Arrangement WHP operates a chain of 317 convenience stores, 302 of which are franchise stores and 15 of which are operated by WHP. These stores average approximately 2,500 square feet in size, offer up-front parking, and are generally open 24 hours a day. WHP stores offer a broad array of grocery items and high quality items in delicatessen products, fresh baked goods and produce. WHP is the only company among the industry's top 50 that does not sell gas. Management strongly believes this policy contributes to a higher quality image and helps attract a broader group of customers. WHP and Jewel management decided early in the development of the company to operate under a franchise system. The Franchise agreement covers a ten-year period and is conditionally renewable. Under the agreement, WHP owns the store and the franchisee owns the inventory and has the right to use the store premises, fixtures and equipment. The franchisee has no ownership interest in the physical property. The franchisee has total authority to manage the store with respect to purchasing, pricing, hiring, firing and other store operation matters provided he or she adheres to the company's strict quality standards. Each franchisee is required to maintain a certain minimum sales level. A franchise fee is paid to WHP on all store sales to cover rent expense and all services it provides. The fee was increased in 1984 from 13% to 13.5% for all new franchisees. It is expected to be increased to 13.5% for all franchises in January, 1986. After paying the franchisee fee, the franchisee retains all profits from the store operation. Franchisee store income is perhaps the most crucial factor determining turnover and the overall financial quality of WHP. Average franchisee earnings increased from $35,000 in 1979 to approximately $50,000 in 1984. Finances and Operations Exhibit B gives a condensed balance sheet as of November 3, 1984. Both an actual and an adjusted balance sheet are shown. The adjusted balance sheet is revised upward to reflect the write-up of assets that will occur as a result of the buyout by RODODAKS. As shown in Exhibit B, the company's working capital needs are minimal. The investment in inventory is primarily for the WHP-operated stores since the franchisees are responsible for their own inventory. About 50 percent of receivables represent amounts due from franchisees are generally collected within 14 days from franchisee. The company does not have any significant trade payables since it acts primarily as paying agent for franchisees and makes inventory purchases only for corporate stores. Trade payables were only $301,000 as of November 3,1984. WHP's minimal working capital requirements are a distinctive advantage over other nonfranchised convenience store organizations. Other organizations must commit about 20% to 30% of incremental sales revenues to support increased working capital needs. In contrast, as WHP grows, it can devote its cash flow mainly to reducing debt rather than reinvesting it to support higher working capital requirements. Exhibit C represents WHPs historical income statements. Over 95 percent of the company's revenues are derived from franchise fees. Total franchise fees as a percentage of total WHP revenues decreased from 1979 through 1982 as the company added corporate operated stores. WHP operated stores are however less profitable than Exhibit C represents WHPs historical income statements. Over 95 percent of the company's revenues are derived from franchise fees. Total franchise fees as a percentage of total WHP revenues decreased from 1979 through 1982 as the company added corporate operated stores. WHP operated stores are however less profitable than franchised stores. Operating profit before depreciation as a percentage of sales has been very stable. Adjusted EBIT shown in Exhibit C excludes the Jewel corporate asset charge which would not continue in the future, hence, adjusted EBIT more appropriately reflects WHPs historical earnings. Management of WHP originally planned, under Jewel ownership, to add 30-40 stores annually for several years and expand the company's organizational staffing levels accordingly. This strategy changed when WHP was put up for sale. Under the buyout proposal, management plans to add only 15 new stores annually. A reduction in the number of new stores within the constraint of capital availability is appealing because the company can focus on market penetration wit the existing store base and still provide meaningful incremental growth. WHP Management The management of WHP comprise the shareholders of ROBODAKS. Management will all remain in place following the buyout and the top five officers will each participate in the LBO as shown in Exhibit A. ROBODAKS has approached PruCapital, Inc. to assist in the buyout of the company. American Stores has agreed to sell the WHP operation to WHP management for a total purchase price of $55,000,000 plus $1,000,000 in closing costs and fees. ROBODAKS will also assume about $1,400,000 in existing debt and will issue $55,700,000 of securities as shown in Exhibit B. Also as shown in Exhibit B, the proposed financing arrangement allocates 33% of the stock to WHP management and 67% to Prudential. WHP management plans to open 15 stores annually and increase average store sales by 7.1% per year. Total sales are projected to increase by 11.5% per year. These increases compare with historical five-year average increases for store growth, growth in sales per store, and total sales growth of 6.6%,6.5% and 13.3% respectively. Management expects WHP's future revenues to reflect an increase in the franchise fee charge from 13% to 13.5% in 1986 for all franchisees. Expenditures for normal store maintenance, redecorating, and major remodeling are expected to continue. PRUCAPITAL From the perspective of PruCapital, in order for the WHP investment to be attractive, the purchase price must be at or below market prices, cash flow must be sufficient to significantly reduce debt and provide PruCapital with an appropriate return on investment. The $56 million gross purchase price (including $1 million of closing costs and $4 million of tax recapture) represents about 12.2x trailing 12 -month net income, and 2.2 book value. Exhibit A: Management Ownership Exhibit B: Balance Sheet as of November 3, 1984 (in \$ Thousands) Exhibit D: Proposed Financing (in S thousands) Note A: The $21,000,000 from PruCapital includes a $6,000,000,6-year seasonal working capital loan plus a $15,000,000 Revolving Note. Both loans are priced at a floating interest rate of 3.75% over the Prudential Commercial Paper Rate (12.5% at 3/22/85) Note B: Annual paydown of $2,000,000 beginning in the fourth year, increasing to $2,500,000 in the seventh year, would retire the issue at maturity. Interest rate =15740/ working capital loan plus a $15,000,000 Revolving Note. Both loans are priced at a floating interest rate of 3.75% over the Prudential Commercial Paper Rate (12.5% at 3/22/85 ) Note B: Annual paydown of $2,000,000 beginning in the fourth year, increasing to $2,500,000 in the seventh year, would retire the issue at maturity. Interest rate =15.74% (3.75% over the 10 -year treasury rate of 11.99%). Note C: Annual paydown of $2,000,000 beginning in the third year would retire the debt in 10 years; Interest rate =16.49%(4.50% over the 10 -year treasury rate of 11.99%). Note D: PruCapital and Prudential will own the preferred stock and will also receive warrants to purchase 120,000 shares at $3.03 per share. Note E: Common stock fully diluted will be held 67% by Prudential and PruCapital ( 51% PruCapital and 16% Prudential Capital Markets) and 33% by ROBODAKS management. Questions 1. Use the Adjusted Present Value (APV) approach to value WHP. 2. Use a discount rate of 20% as the base case. 3. Assume a tax rate of 40%. 4. Assume that debt is paid down as scheduled through the end of 1993. Then assume that the debt is rolled over thereafter. That is, debt is constant after 1993. 5. Assume all debt payments occur at year end. 6. Assume that the $21.0 million revolving loan is never paid off. That is, the revolving loan is renewed every year after the 6th year. 7. To simplify the analysis, assume costs and expenses are projected to be the same percent of sales in the future as they were during the period 1980-1983. Use an average percentage rate in making this calculation. 8. Project year-by-year cash flows for 1984-1992, then assume a constant growth rate of cash flows thereafter Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Technical Analysis Of Stock Trends

Authors: Robert D. Edwards, John Magee

1st Edition

1607962233, 978-1607962236