Please see the Chapter 8 section in your textbook entitled "using your judgement" and read the financial statement analysis case listed as Case 1: T J International.

A- how much income before taxes have been if FIFO costing had been used to value all inventories? Show computations to support answer.

B- If the income tax rate is 46.6%, what would income tax have been if FIFO costing had been used to value all inventories? Show computations.

In your opinion, is this difference in net income between the two methods material? Explain

C- Does the use of a different costing system for different types of inventory mean that there is a different physical flow of goods among the different types of inventory? Explain

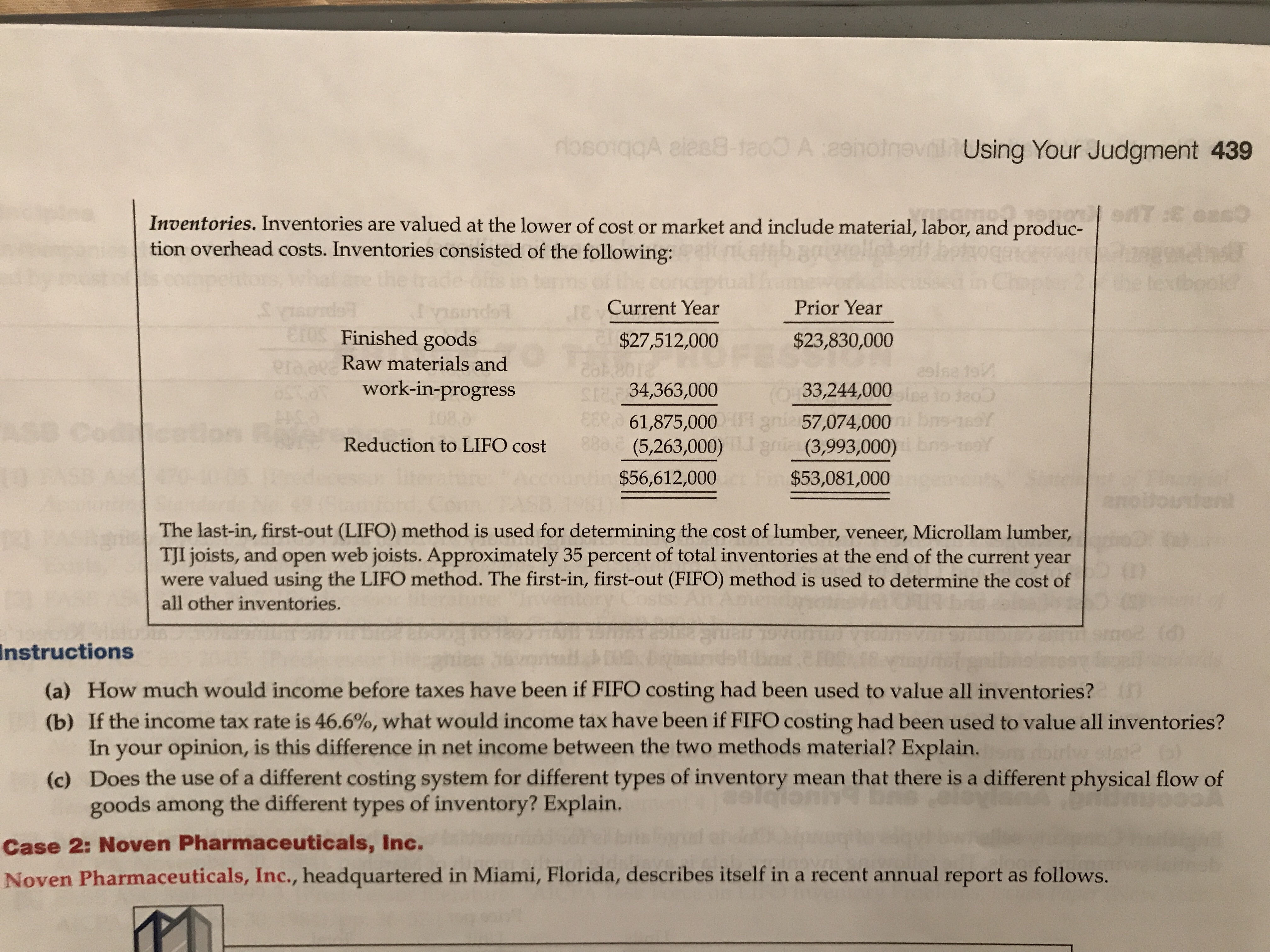

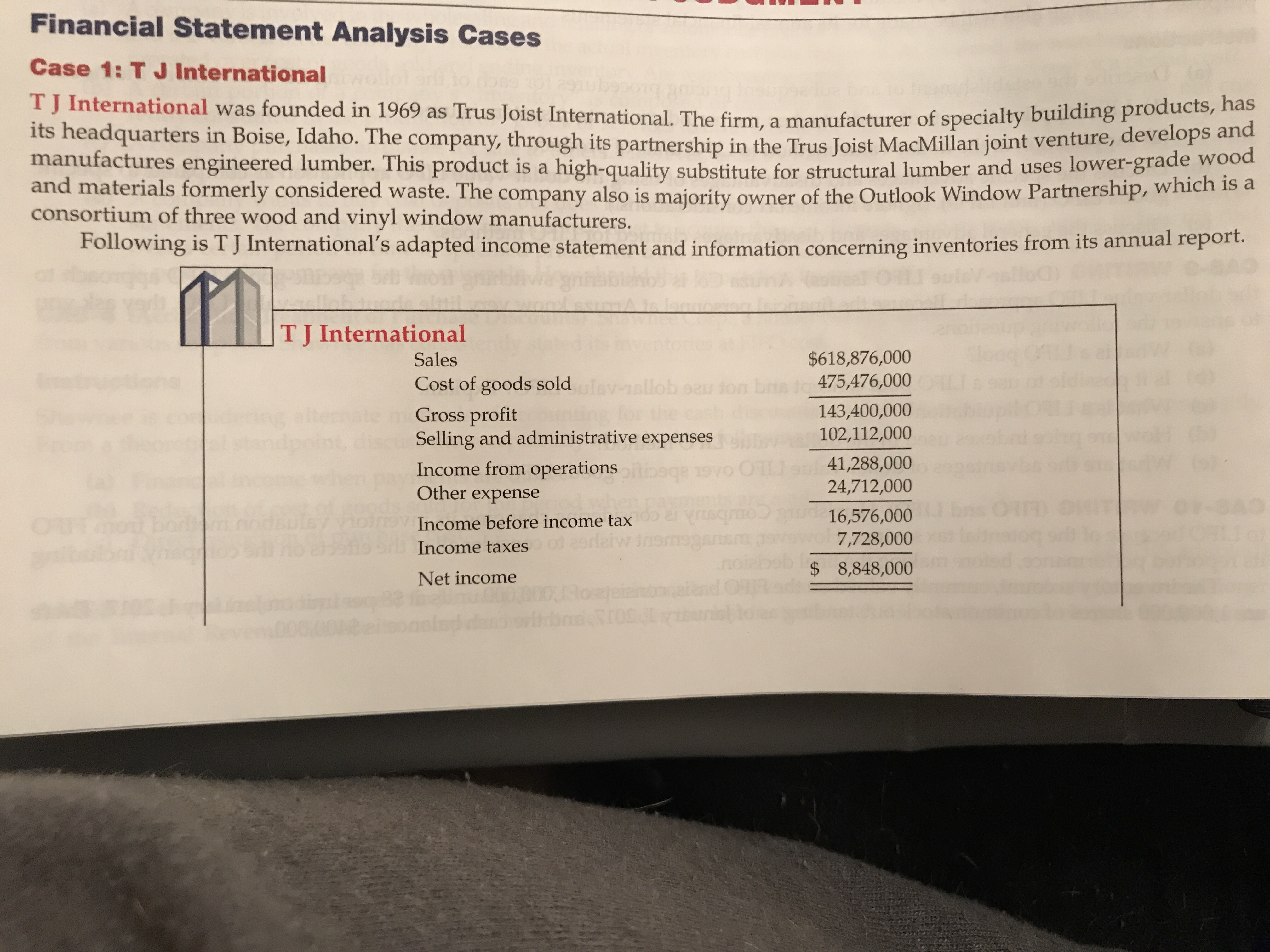

nstructions Case 2: Noven Pharmaceuticals, Inc. in some all other inventories. esti osto eralove goods among the different types of inventory? Explain. Eros Finished goods tion overhead costs. Inventories consisted of the following: Raw materials and work-in-progress Reduction to LIFO cost viGuTdot In your opinion, is this difference in net income between the two methods material? Explain. Noven Pharmaceuticals, Inc., headquartered in Miami, Florida, describes itself in a recent annual report as follows. A31 (a) How much would income before taxes have been if FIFO costing had been used to value all inventories?( ARTS 8 102 The last-in, first-out (LIFO) method is used for determining the cost of lumber, veneer, Microllam lumber, were valued using the LIFO method. The first-in, first-out (FIFO) method is used to determine the cost of TJI joists, and open web joists. Approximately 35 percent of total inventories at the end of the current year (b) If the income tax rate is 46.6%, what would income tax have been if FIFO costing had been used to value all inventories? (c) Does the use of a different costing system for different types of inventory mean that there is a different physical flow of 88 (5,263,000) Current Year $56,612,000 34,363,000 $27,512,000 61,875,000 Inventories. Inventories are valued at the lower of cost or market and include material, labor, and produc. otual IN an 57,074,000 i. gra (3,993,000) Prior Year $53,081,000 $23,830,000 33,244,000 dosoiggA eles8-1200 A :esholnevill/Using Your Judgment 439 bno-160Y 168 10 3200 bno-ingY colse tak seed in Chap the texthCase 1: T J International Financial Statement Analysis Cases consortium of three wood and vinyl window manufacturers. soocloone ettoonoind of T J International Sales Gross profit Net income Income taxes Other expense Income from operations Income before income tax Selling and administrative expenses Cost of goods sold givens llob sau ton bris its headquarters in Boise, Idaho. The company, through its partnership in the Trus Joist MacMillan joint venture, develops and T J International was founded in 1969 as Trus Joist International. The firm, a manufacturer of specialty building products, has and materials formerly considered waste. The company also is majority owner of the Outlook Window Partnership, which is a manufactures engineered lumber. This product is a high-quality substitute for structural lumber and uses lower-grade wood Following is T J International's adapted income statement and information concerning inventories from its annual report. 105 al vrisamo_ Jnomsgansme Jave page 1970 OTL. 1 9 .not dom $618,876,000 $ 8,848,000 143,400,000 102, 112,000 475,476,000 24,712,000 41,288,000 16,576,000 7,728,000 10 CEILO S