- Please see the snap photo below for further instructions

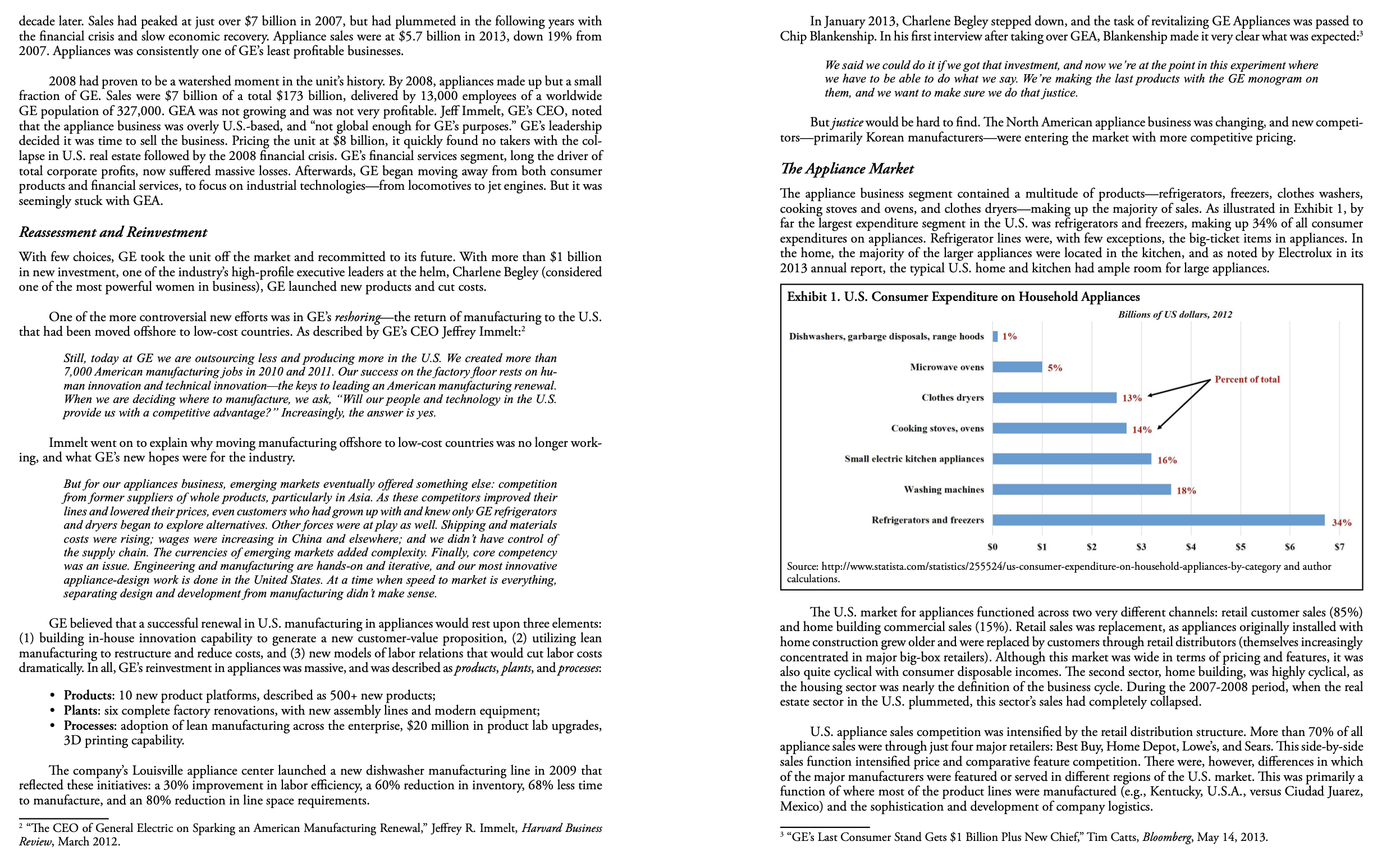

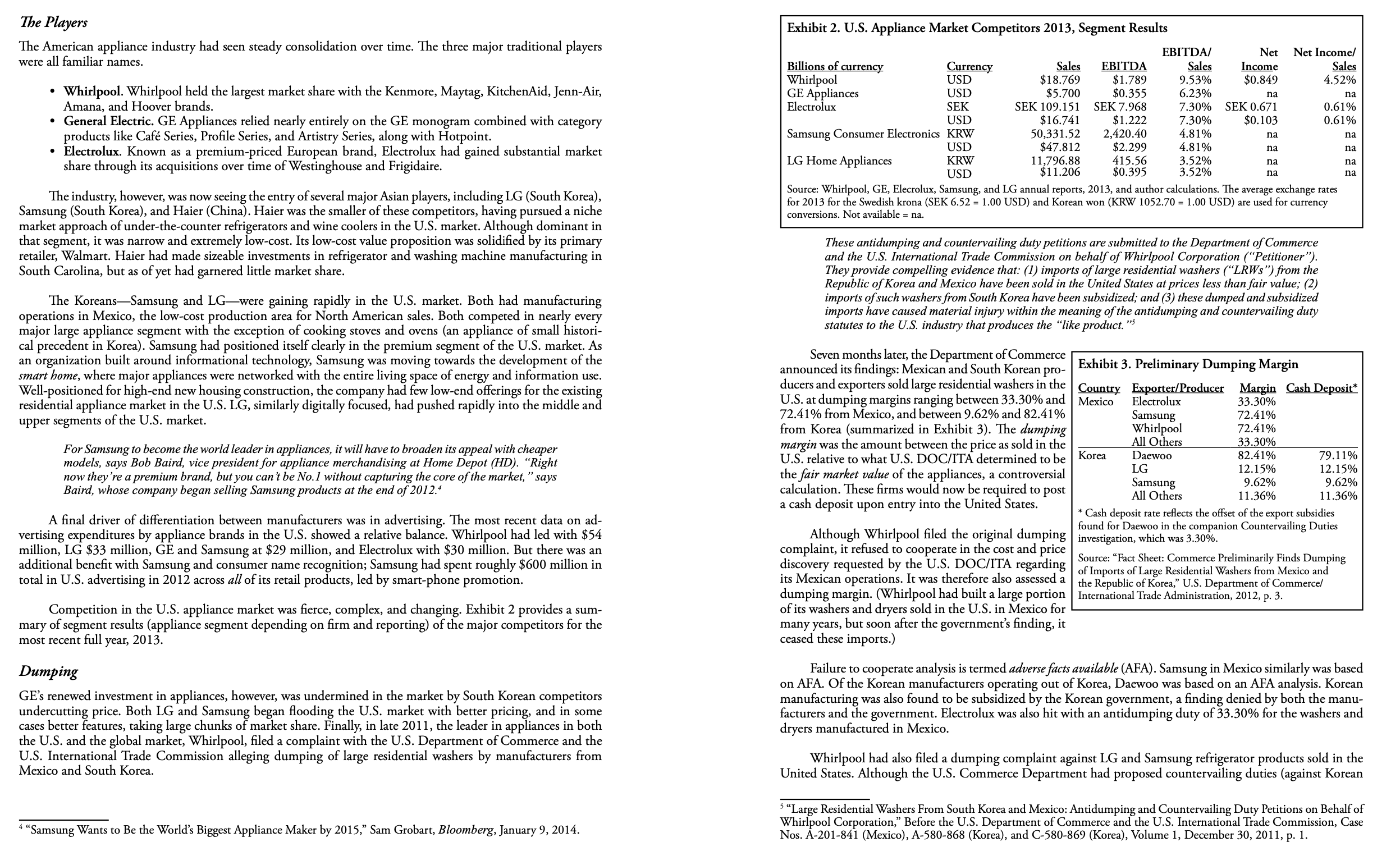

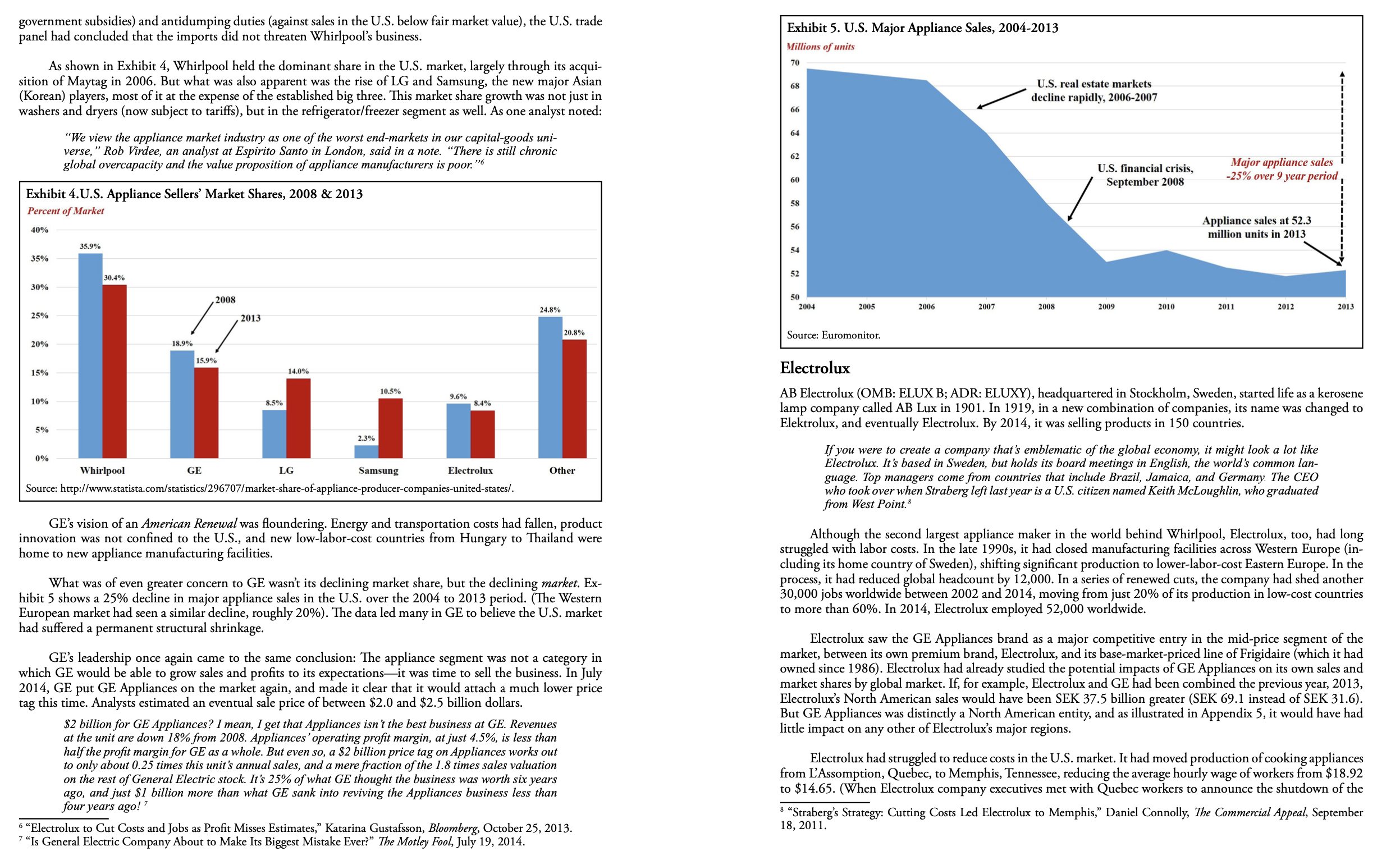

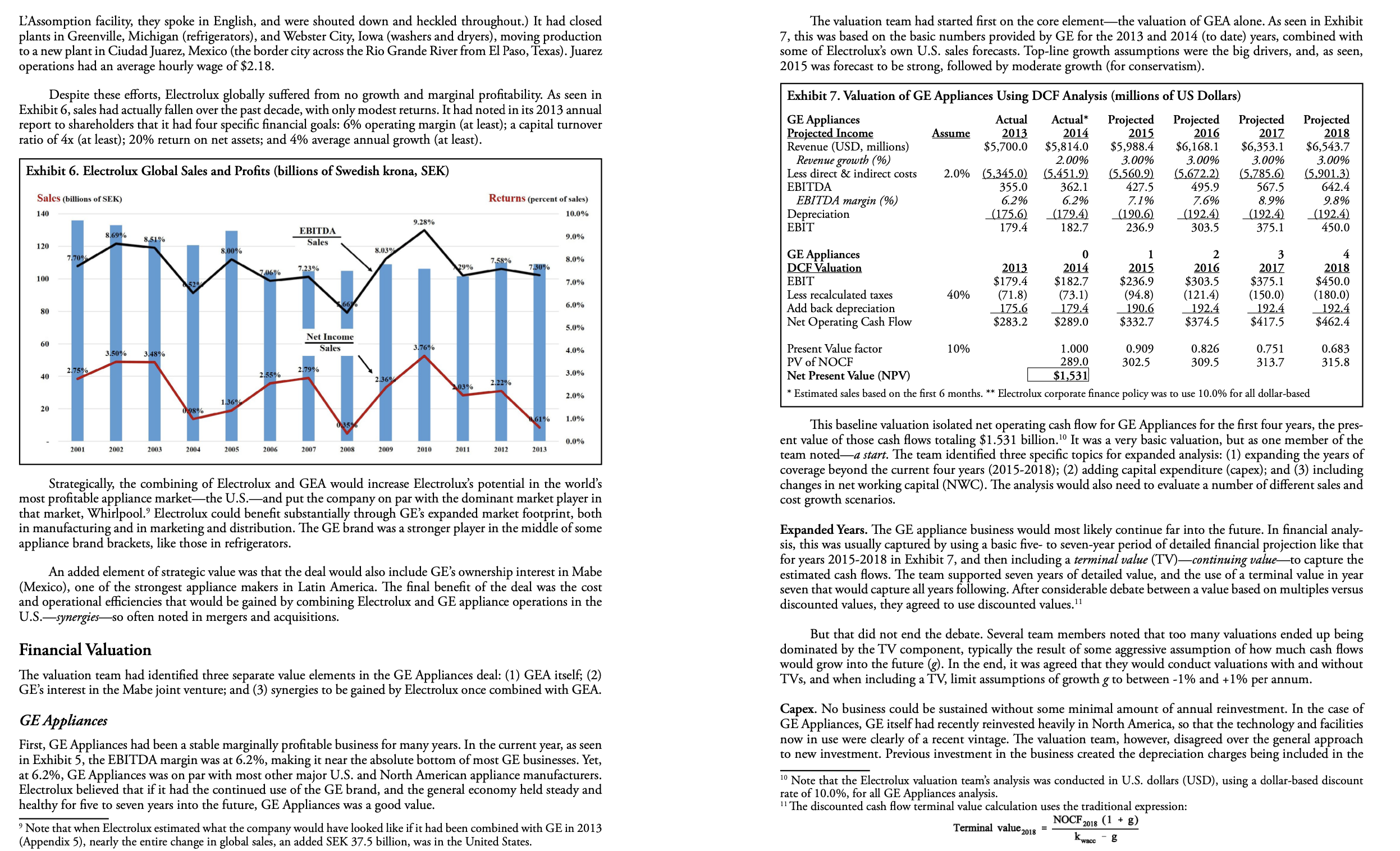

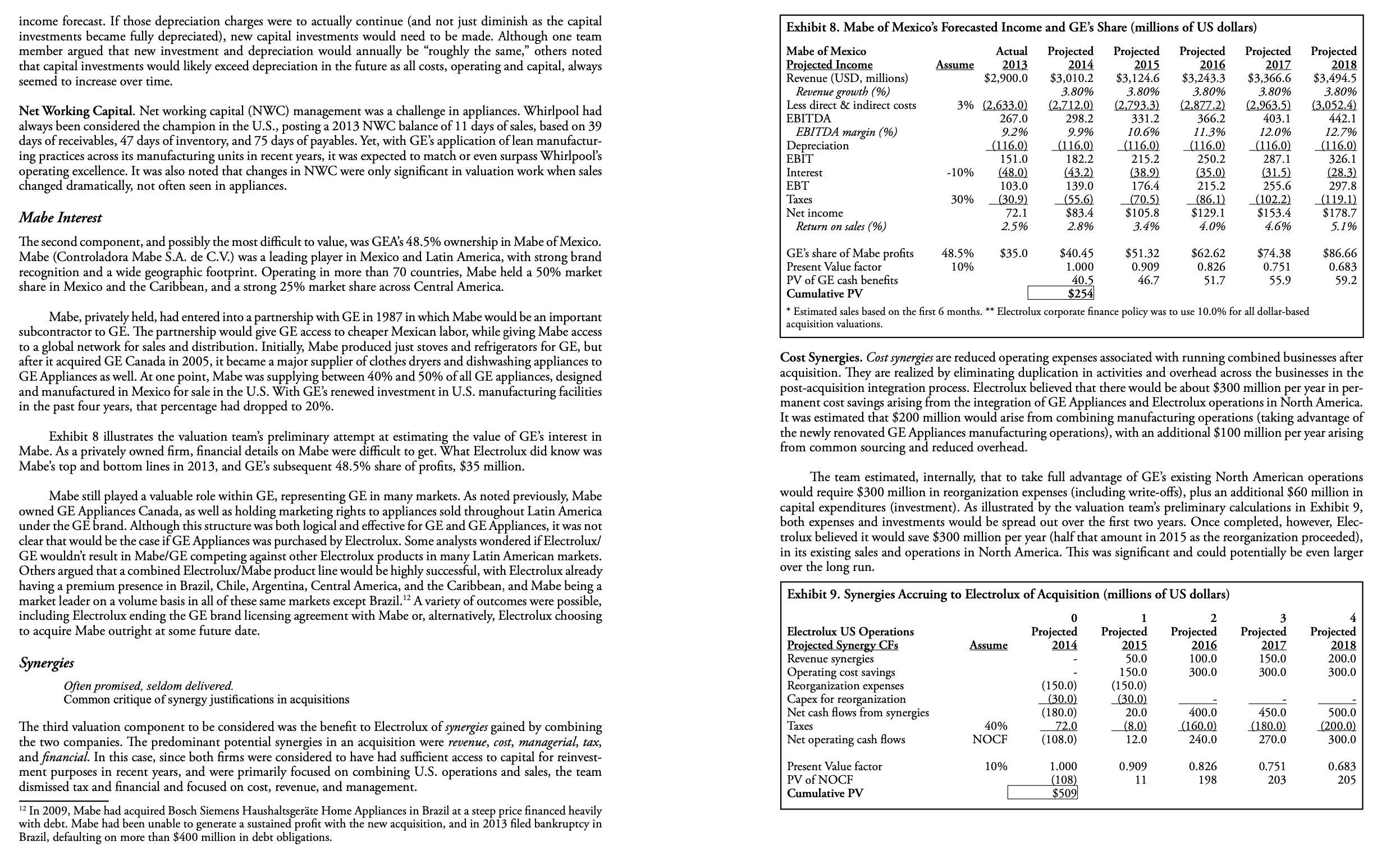

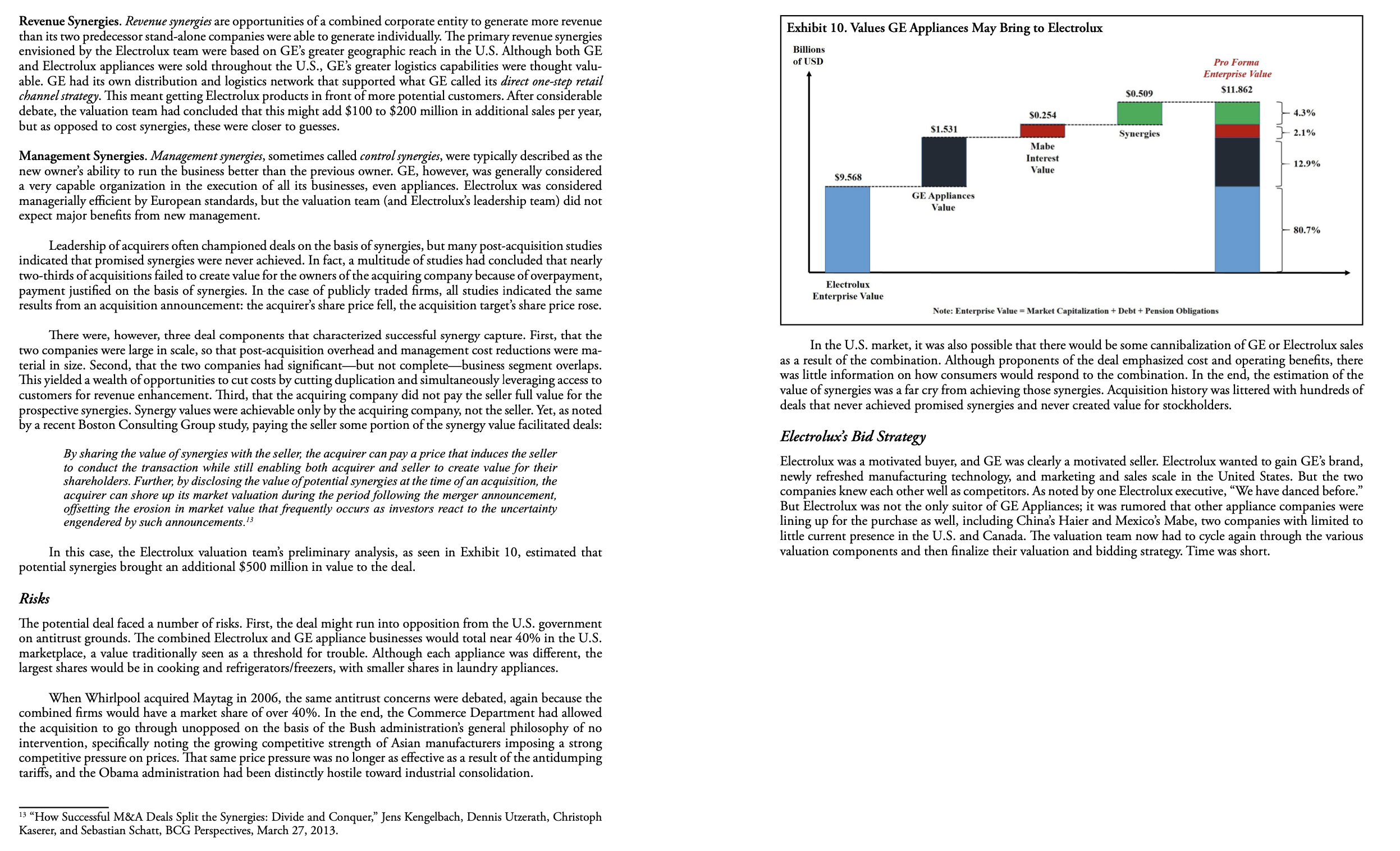

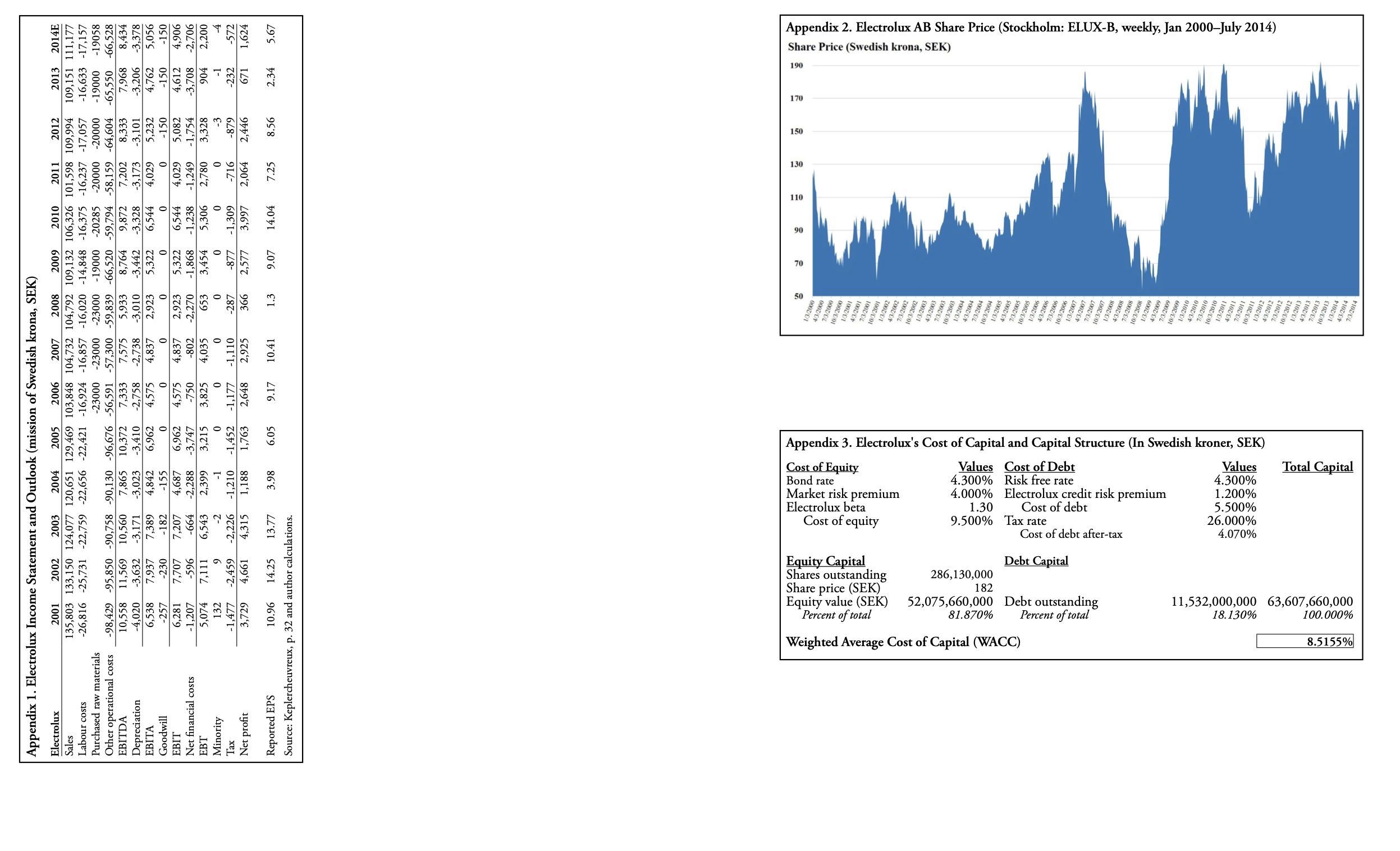

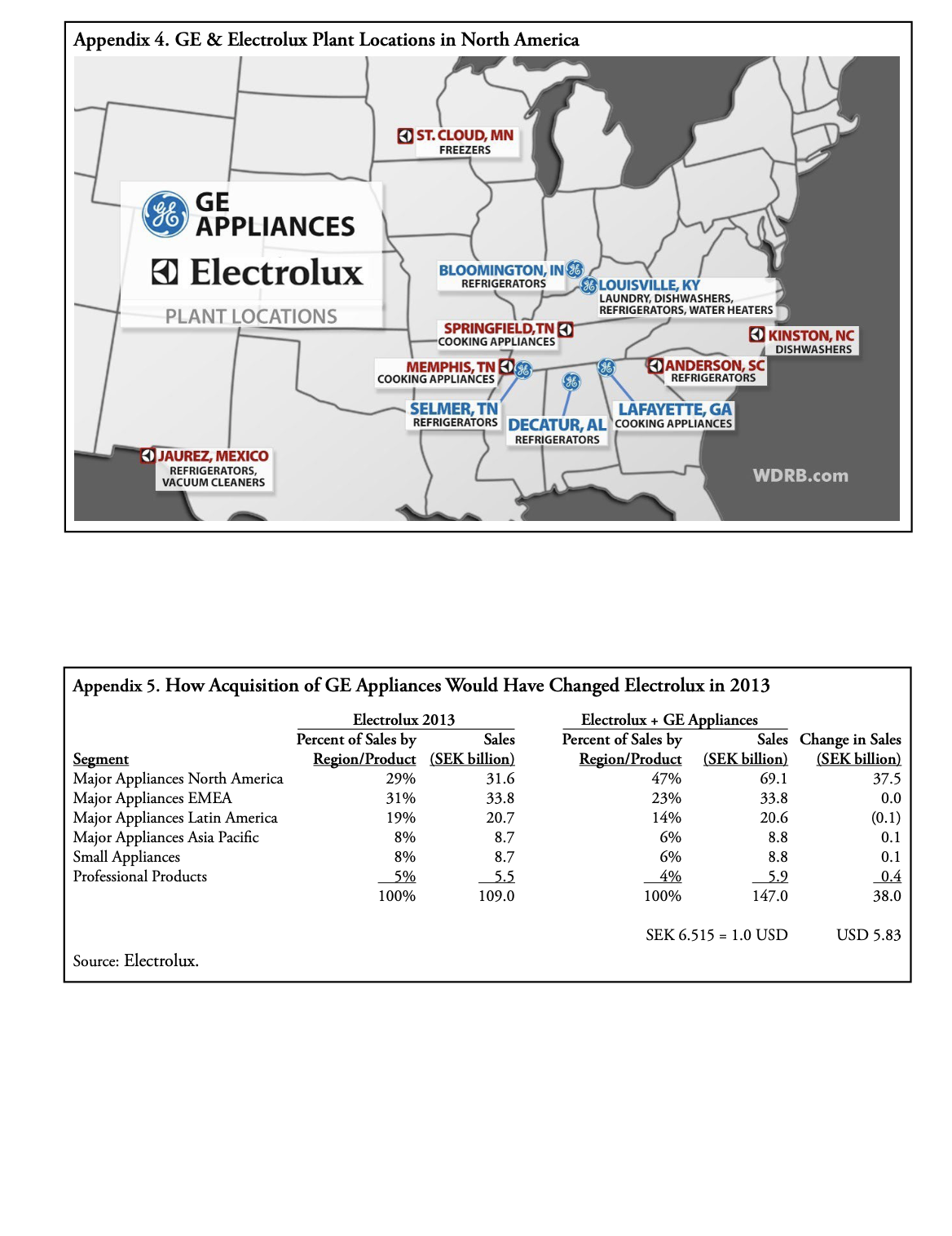

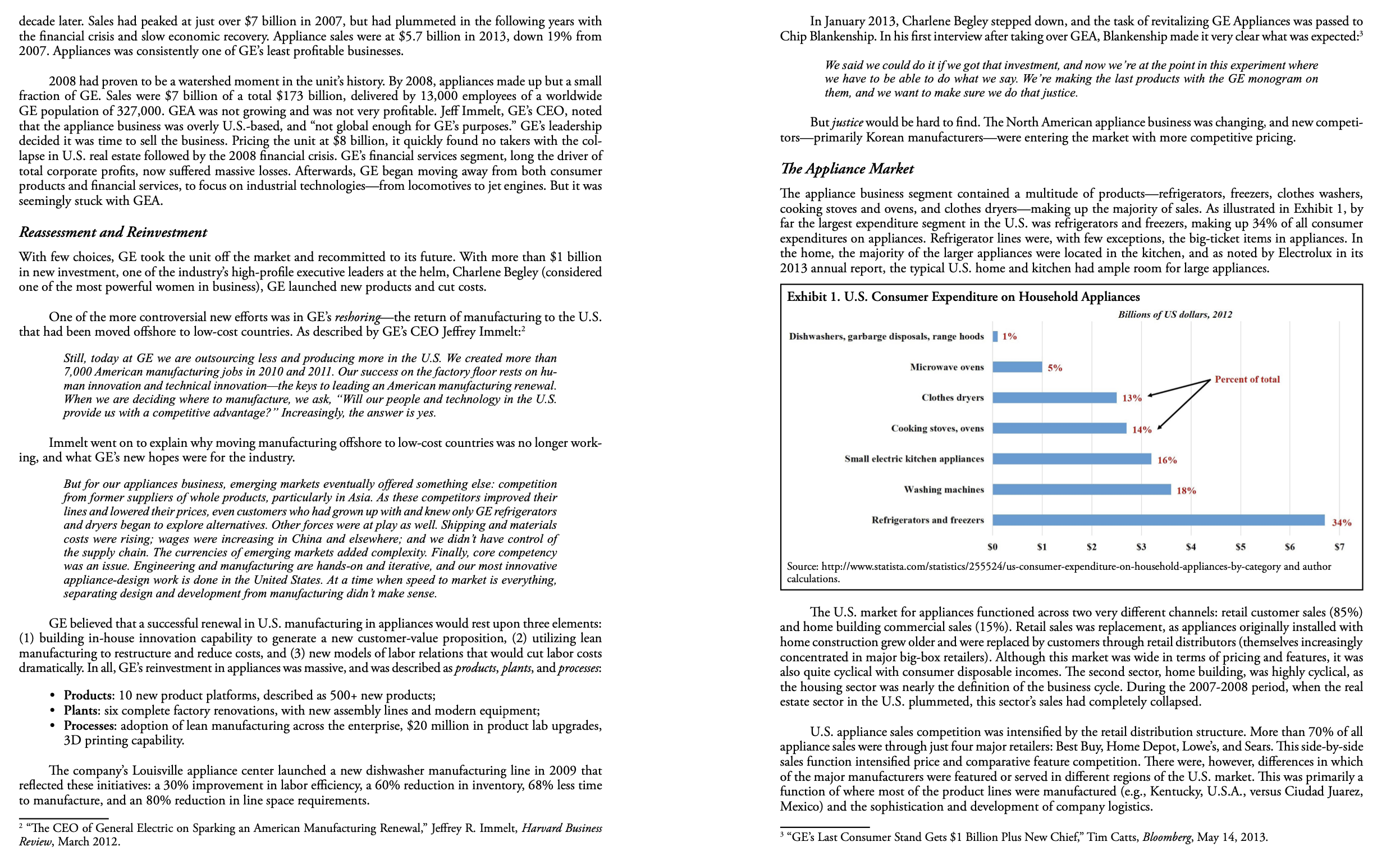

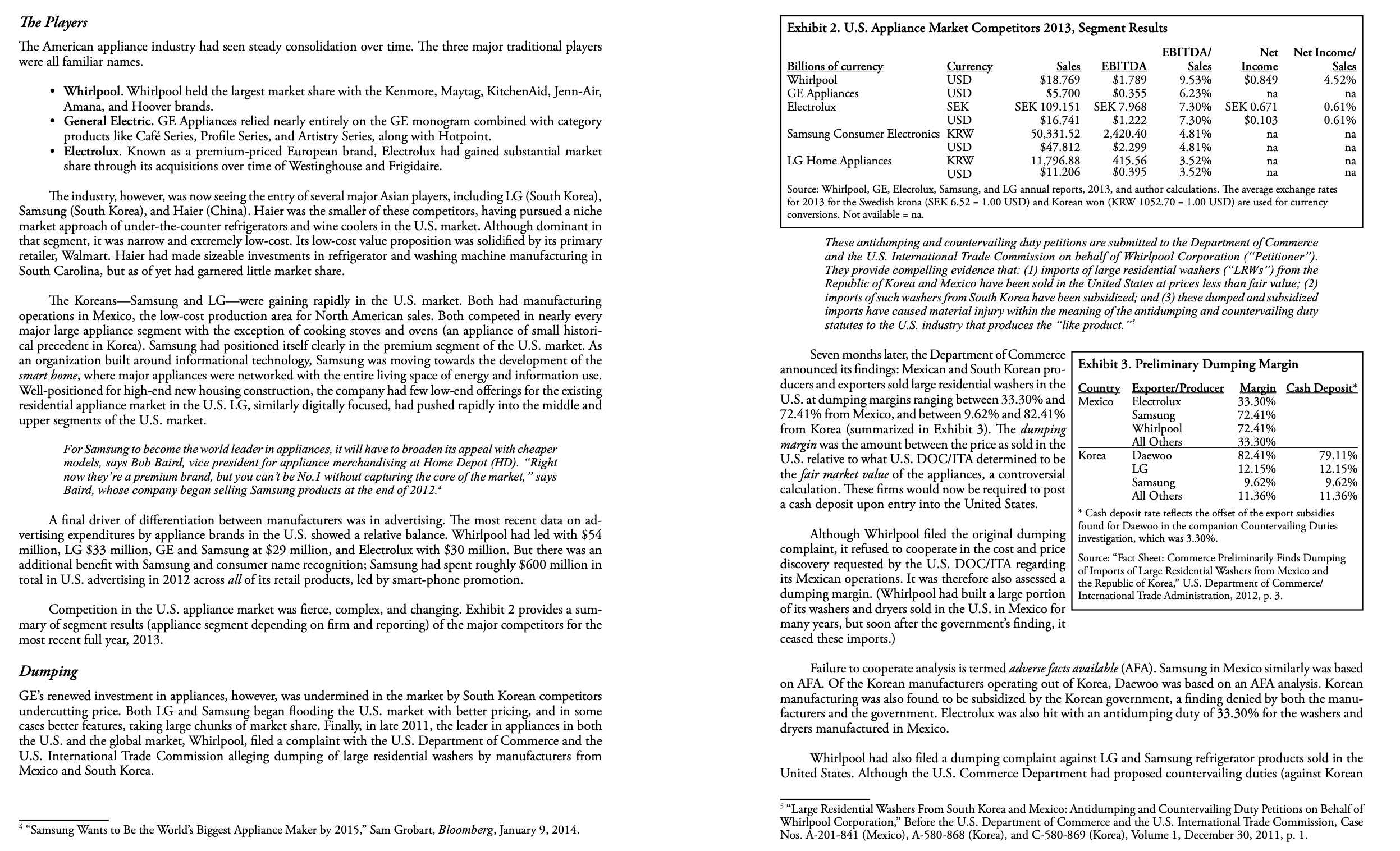

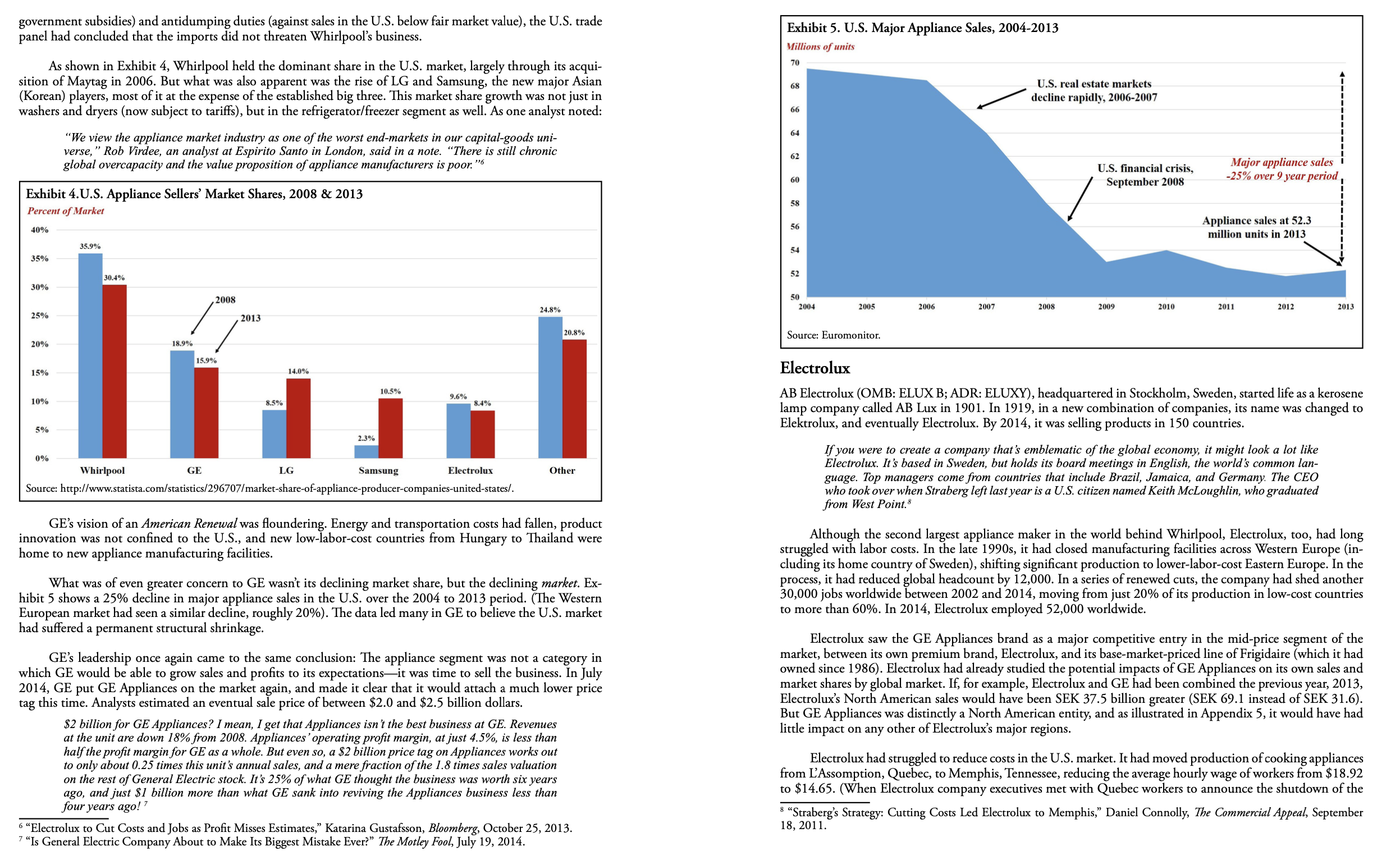

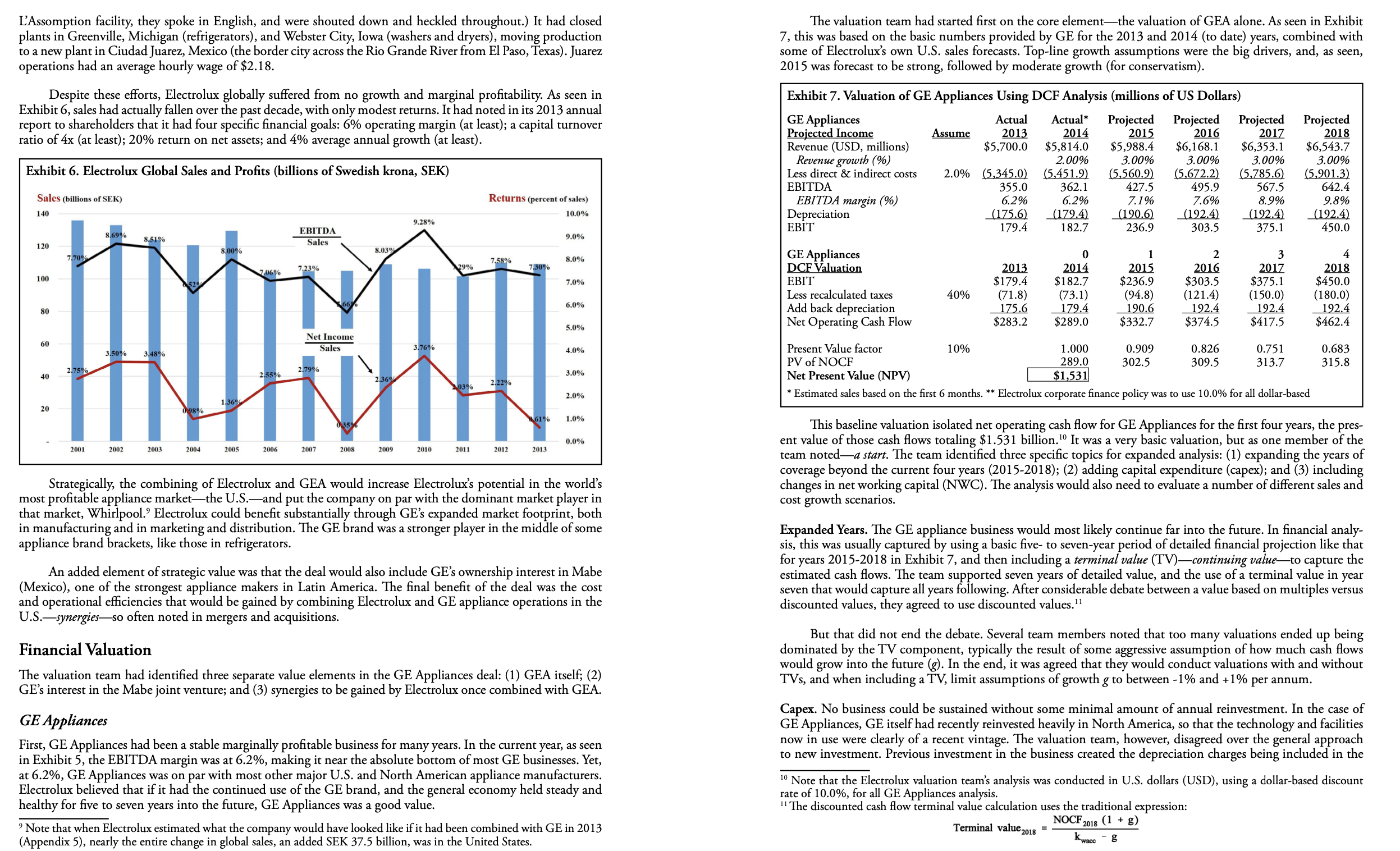

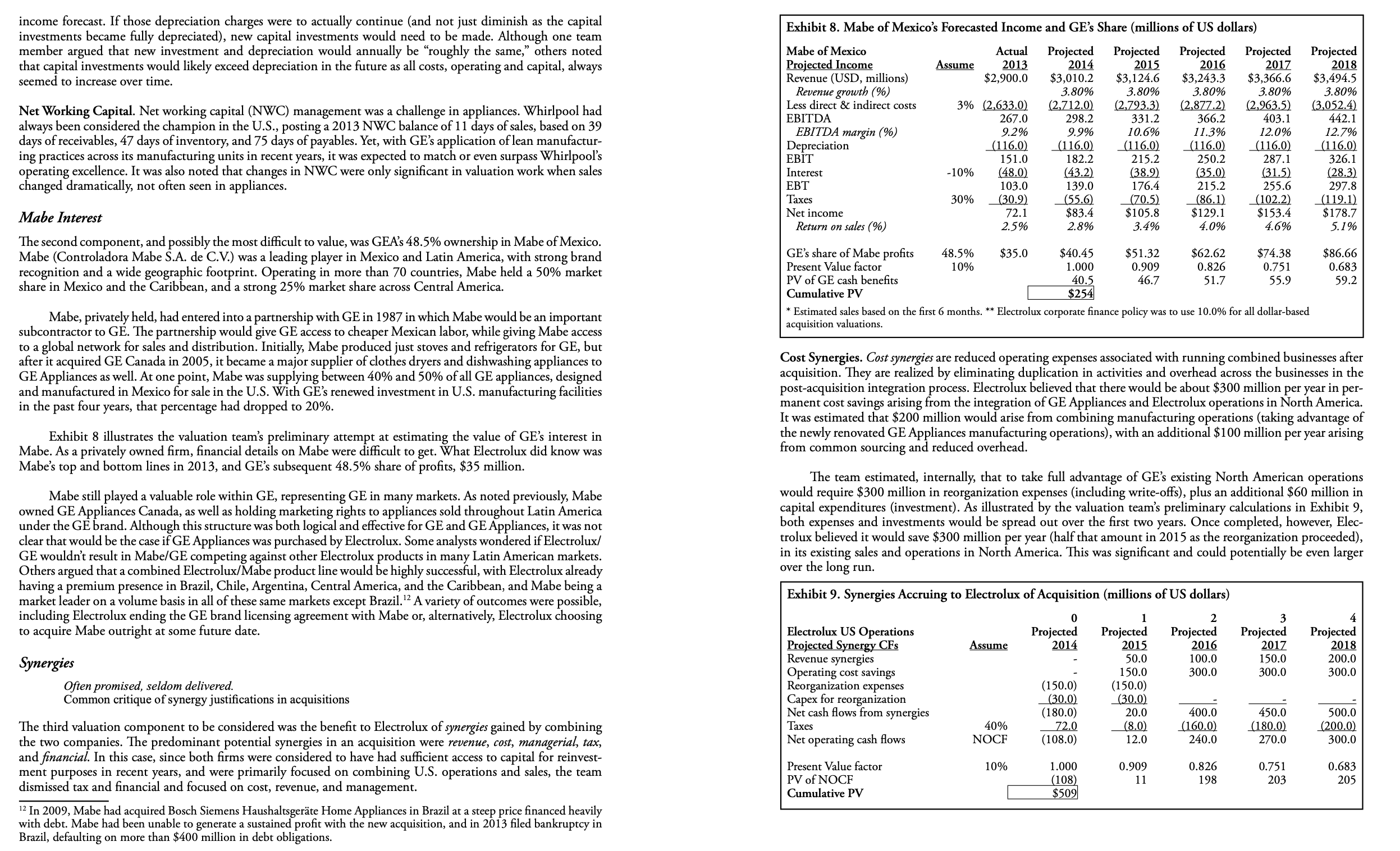

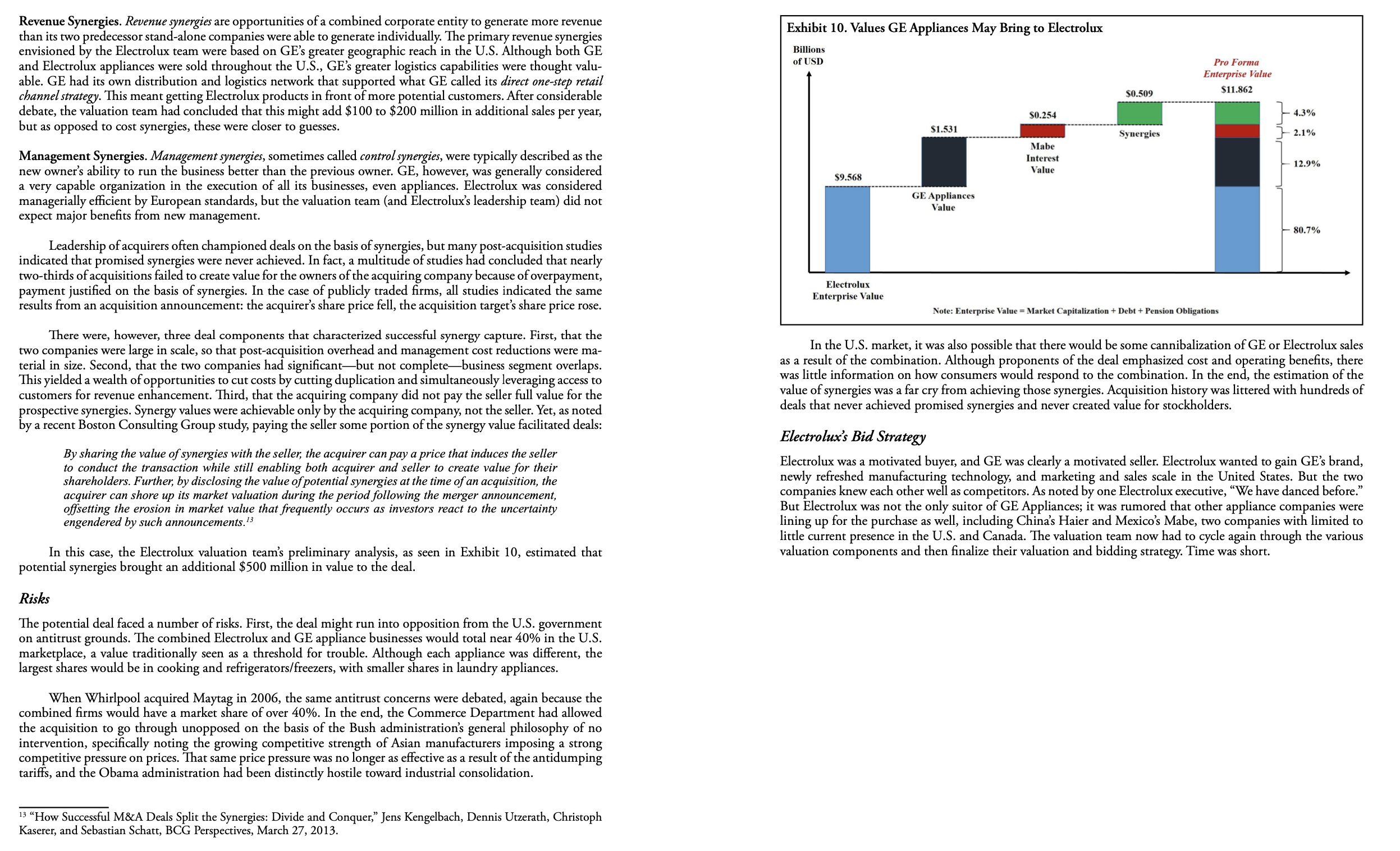

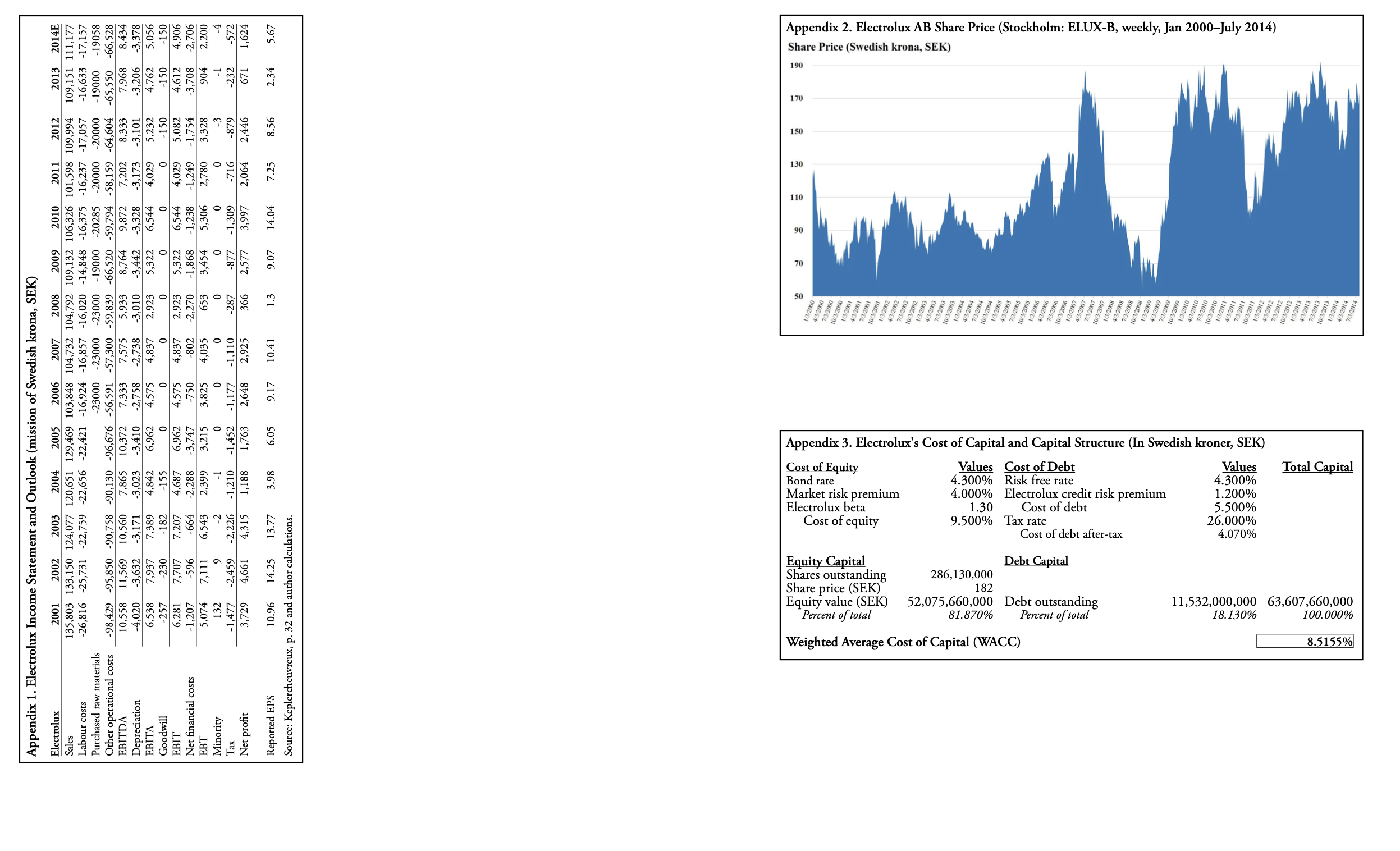

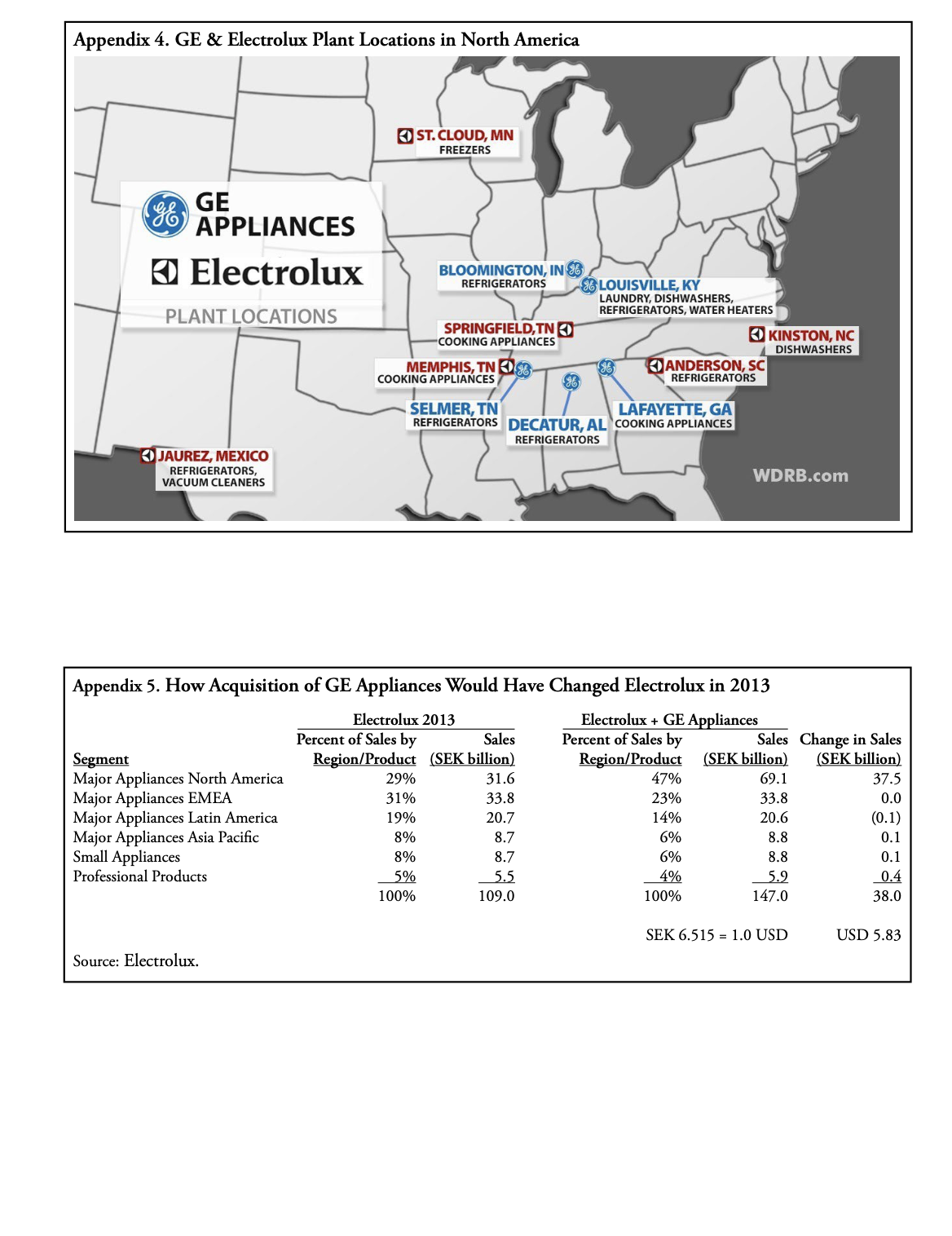

1. Read the Electrolux and GE Appliance". 3. Answer the following questions. ___-____-- \L _ ' Case Questions You are leading the valuation team at Electrolux. Your task is to prepare the nancial valuation, for Electrolux, for your upcoming negotiations to buy GE Appliances. 1. Value in depth the GE Appliances business. What is GE Appliances worth to Electrolux? 2. What do you recommend as your bid, including your assessment of the prospective value including synergies and GE's likely position on the sale? Do not assume that the valuations or calculations in the preliminary analysis are in any way correct or complete. Its your job to make sure they are done right. The template is only to get you started. Electrolux and GE Appliances GE math. Consider: Let's assume GE mispriced Appliances when it tried to sell it six years ago (a safe assumption, since it didn't sell). So, let's say the Appliances business was worth not $8 billion back then, but rather just half that-$4 billion. Add the $1 billion spent spiffing up the business, and divide the resulting $5 billion value into the best-case price GE is expected to get for the unit today: $2.5 billion. That works out to a 50% loss for GE shareholders. "Is General Electric Company About to Make Its Biggest Mistake Ever?" The Motley Fool, 19 July 2014. Electrolux's valuation team was working out of the company's corporate headquarters in Stockholm, Sweden. Its task was to complete both a valuation and suggested final offer for GE's appliance unit by mid-August 2014, which meant that the summer holiday sailing on the archipelago would be lost. The team's challenge was in capturing the value of GE's appliance unit, both as a stand-alone business and as combined with Electrolux. GE would know that Electrolux would see added value in it-so-called synergies-and would be building that differential into its asking price. But the value of GE Appliances (GEA) had also fallen over time, as demonstrated by GE's own efforts at selling the business repeatedly. There were two questions to answer: (1) what was GE Appliances worth; and (2) what should Electrolux offer? General Electric General Electric (NYSE: GE) was a conglomerate-a portfolio of businesses spanning many different industries. In an age of single industry pure plays and core competency, GE was strikingly different, continuing to compete in everything from turbine engines to financial services to appliances. GE, now in its 13th year under CEO Jeffrey Immelt, was in the midst of a transformation-as described by The Economist the previous month-to transform GE from a misfiring finance-heavy conglomerate into a more focused maker of industrial equipment.' The company was shedding many of the businesses which it did not believe were capable of significant growth and profitability. GEA is at the top of that list. Appliances GE Appliances, a sub-unit of Home and Business Solutions, headquartered in Louisville, Kentucky, generated more than 90% of its revenue in North America. The product portfolio included refrigerators, freezers, cooking products, dishwashers, washers, dryers, air conditioners, water filtration systems, and water heaters. Its revenue split by major product category was approximately 35% cooking, 25% refrigeration, 20% laundry, 10% dish- washers, and 10% home comfort (air conditioning). GE Appliances was largely a U.S.-based business. Operations in the U.S. consisted of refrigeration units in Selmer, Tennessee, Decatur, Alabama, and Bloomington, Indiana; a cooking unit in LaFayette, Georgia; in addition to the largest and most diversified unit (laundry, dishwashers, refrigerators, water heaters) in Louisville, Kentucky. Louisville also served as the corporate center for GE Appliances. GE's appliances, along with its lighting products, is in many ways the GE brand image. Founded in 1907, GE's first products were cooking appliances. It continued to be a leader in appliance innovation for more than half-century, being the first to launch air conditioners (1950), the combined washer/dryer (1954), and the toaster oven (1956). Despite that track record, GE's appliance business had shown little growth or profitability for more than two decades. GE's appliance sales in 1990 were $5.3 billion, but only $5.7 billion in 2000, a fulldecade later. Sales had peaked at just over $7 billion in 2007, but had plummeted in the following years with the financial crisis and slow economic recovery. Appliance sales were at $5.7 billion in 2013, down 19% from In January 2013, Charlene Begley stepped down, and the task of revitalizing GE Appliances was passed to Chip Blankenship. In his first interview after taking over GEA, Blankenship made it very clear what was expected:3 2007. Appliances was consistently one of GE's least profitable businesses. We said we could do it if we got that investment, and now we're at the point in this experiment where 2008 had proven to be a watershed moment in the unit's history. By 2008, appliances made up but a small we have to be able to do what we say. We're making the last products with the GE monogram on fraction of GE. Sales were $7 billion of a total $173 billion, delivered by 13,000 employees of a worldwide hem, and we want to make sure we do that justice GE population of 327,000. GEA was not growing and was not very profitable. Jeff Immelt, GE's CEO, noted that the appliance business was overly U.S.-based, and "not global enough for GE's purposes." GE's leadership But justice would be hard to find. The North American appliance business was changing, and new competi- decided it was time to sell the business. Pricing the unit at $8 billion, it quickly found no takers with the col- tors-primarily Korean manufacturers-were entering the market with more competitive pricing. lapse in U.S. real estate followed by the 2008 financial crisis. GE's financial services segment, long the driver of total corporate profits, now suffered massive losses. Afterwards, GE began moving away from both consumer The Appliance Market products and financial services, to focus on industrial technologies-from locomotives to jet engines. But it was seemingly stuck with GEA. The appliance business segment contained a multitude of products-refrigerators, freezers, clothes washers, cooking stoves and ovens, and clothes dryers-making up the majority of sales. As illustrated in Exhibit 1, by Reassessment and Reinvestment ar the largest expenditure segment in the U.S. was refrigerators and freezers, making up 34% of all consumer expenditures on appliances. Refrigerator lines were, with few exceptions, the big-ticket items in appliances. In With few choices, GE took the unit off the market and recommitted to its future. With more than $1 billion the home, the majority of the larger appliances were located in the kitchen, and as noted by Electrolux in its in new investment, one of the industry's high-profile executive leaders at the helm, Charlene Begley (considered 2013 annual report, the typical U.S. home and kitchen had ample room for large appliances. one of the most powerful women in business), GE launched new products and cut costs. Exhibit 1. U.S. Consumer Expenditure on Household Appliances One of the more controversial new efforts was in GE's reshoring-the return of manufacturing to the U.S. Billions of US dollars, 2012 that had been moved offshore to low-cost countries. As described by GE's CEO Jeffrey Immelt:2 Dishwashers, garbarge disposals, range hoods | 1% Still, today at GE we are outsourcing less and producing more in the U.S. We created more than 7,000 American manufacturing jobs in 2010 and 2011. Our success on the factory floor rests on hu- Microwave ovens 5% man innovation and technical innovation-the keys to leading an American manufacturing renewal. Percent of total When we are deciding where to manufacture, we ask, "Will our people and technology in the U.S. Clothes dryers 13% provide us with a competitive advantage? " Increasingly, the answer is yes Cooking stoves, ovens 14% Immelt went on to explain why moving manufacturing offshore to low-cost countries was no longer work- ing, and what GE's new hopes were for the industry. Small electric kitchen appliances 16% But for our appliances business, emerging markets eventually offered something else: competition from former suppliers of whole products, particularly in Asia. As these competitors improved their Washing machines 18% lines and lowered their prices, even customers who had grown up with and knew only GE refrigerators and dryers began to explore alternatives. Other forces were at play as well. Shipping and materials Refrigerators and freezers 34% costs were rising; wages were increasing in China and elsewhere; and we didn't have control of the supply chain. The currencies of emerging markets added complexity. Finally, core competency $0 $1 $2 $3 $4 $5 $6 $7 was an issue. Engineering and manufacturing are hands-on and iterative, and our most innovative Source: http://www.statista.com/statistics/255524/us-consumer-expenditure-on-household-appliances-by-category and author appliance-design work is done in the United States. At a time when speed to market is everything, calculations. separating design and development from manufacturing didn't make sense. GE believed that a successful renewal in U.S. manufacturing in appliances would rest upon three elements: The U.S. market for appliances functioned across two very different channels: retail customer sales (85%) (1) building in-house innovation capability to generate a new customer-value proposition, (2) utilizing lean and home building commercial sales (15%). Retail sales was replacement, as appliances originally installed with manufacturing to restructure and reduce costs, and (3) new models of labor relations that would cut labor costs home construction grew older and were replaced by customers through retail distributors (themselves increasingly dramatically. In all, GE's reinvestment in appliances was massive, and was described as products, plants, and processes: concentrated in major big-box retailers). Although this market was wide in terms of pricing and features, it was also quite cyclical with consumer disposable incomes. The second sector, home building, was highly cyclical, as Products: 10 new product platforms, described as 500+ new products; the housing sector was nearly the definition of the business cycle. During the 2007-2008 period, when the real Plants: six complete factory renovations, with new assembly lines and modern equipment; estate sector in the U.S. plummeted, this sector's sales had completely collapsed. Processes: adoption of lean manufacturing across the enterprise, $20 million in product lab upgrades, 3D printing capability. U.S. appliance sales competition was intensified by the retail distribution structure. More than 70% of all appliance sales were through just four major retailers: Best Buy, Home Depot, Lowe's, and Sears. This side-by-side The company's Louisville appliance center launched a new dishwasher manufacturing line in 2009 that sales function intensified price and comparative feature competition. There were, however, differences in which reflected these initiatives: a 30% improvement in labor efficiency, a 60% reduction in inventory, 68% less time of the major manufacturers were featured or served in different regions of the U.S. market. This was primarily a to manufacture, and an 80% reduction in line space requirements. function of where most of the product lines were manufactured (e.g., Kentucky, U.S.A., versus Ciudad Juarez, Mexico) and the sophistication and development of company logistics. "The CEO of General Electric on Sparking an American Manufacturing Renewal," Jeffrey R. Immelt, Harvard Business Review, March 2012. "GE's Last Consumer Stand Gets $1 Billion Plus New Chief," Tim Catts, Bloomberg, May 14, 2013.The Players Exhibit 2. U.S. Appliance Market Competitors 2013, Segment Results The American appliance industry had seen steady consolidation over time. The three major traditional players were all familiar names. EBITDA/ Net Net Income/ Billions of currency Currency Sales EBITDA Sales Income Sales Whirlpool USD $18.769 $1.789 9.53% $0.849 . Whirlpool. Whirlpool held the largest market share with the Kenmore, Maytag, KitchenAid, Jenn-Air, 1.52% GE Appliances USD $5.700 $0.355 6.23% Amana, and Hoover brands. Electrolux SEK SEK 109.151 SEK 7.968 7.30% SEK 0.671 na na 0.61% . General Electric. GE Appliances relied nearly entirely on the GE monogram combined with category USD $16.741 $1.222 7.30% $0.103 0.61% products like Cafe Series, Profile Series, and Artistry Series, along with Hotpoint. Samsung Consumer Electronics KRW 0,331.52 2,420.40 4.81% na na . Electrolux. Known as a premium-priced European brand, Electrolux had gained substantial market USD $47.812 $2.299 4.81% na share through its acquisitions over time of Westinghouse and Frigidaire. LG Home Appliances KRW 1,796.88 na $11.206 415.56 3.52% na na JSD $0.395 3.52% na na The industry, however, was now seeing the entry of several major Asian players, including LG (South Korea), Source: Whirlpool, GE, Elecrolux, Samsung, and LG annual reports, 2013, and author calculations. The average exchange rates Samsung (South Korea), and Haier (China). Haier was the smaller of these competitors, having pursued a niche for 2013 for the Swedish krona (SEK 6.52 = 1.00 USD) and Korean won (KRW 1052.70 = 1.00 USD) are used for currency market approach of under-the-counter refrigerators and wine coolers in the U.S. market. Although dominant in conversions. Not available = na. that segment, it was narrow and extremely low-cost. Its low-cost value proposition was solidified by its primary These antidumping and countervailing duty petitions are submitted to the Department of Commerce retailer, Walmart. Haier had made sizeable investments in refrigerator and washing machine manufacturing in and the U.S. International Trade Commission on behalf of Whirlpool Corporation ("Petitioner"). South Carolina, but as of yet had garnered little market share. They provide compelling evidence that: (1) imports of large residential washers ("LRWs") from the Republic of Korea and Mexico have been sold in the United States at prices less than fair value; (2) The Koreans-Samsung and LG-were gaining rapidly in the U.S. market. Both had manufacturing imports of such washers from South Korea have been subsidized; and (3) these dumped and subsidized operations in Mexico, the low-cost production area for North American sales. Both competed in nearly every imports have caused material injury within the meaning of the antidumping and countervailing duty major large appliance segment with the exception of cooking stoves and ovens (an appliance of small histori- statutes to the U.S. industry that produces the "like product. "s cal precedent in Korea). Samsung had positioned itself clearly in the premium segment of the U.S. market. As an organization built around informational technology, Samsung was moving towards the development of the Seven months later, the Department of Commerce smart home, where major appliances were networked with the entire living space of energy and information use. announced its findings: Mexican and South Korean pro- Exhibit 3. Preliminary Dumping Margin Well-positioned for high-end new housing construction, the company had few low-end offerings for the existing ducers and exporters sold large residential washers in the | Country residential appliance market in the U.S. LG, similarly digitally focused, had pushed rapidly into the middle and U.S. at dumping margins ranging between 33.30% and |Mexico Exporter/Producer Margin Cash Deposit* 72.41% from Mexico, and between 9.62% and 82.41% Electrolux 33.30% upper segments of the U.S. market. Samsung 72.41% from Korea (summarized in Exhibit 3). The dumping Whirlpool 72.41% For Samsung to become the world leader in appliances, it will have to broaden its appeal with cheaper margin was the amount between the price as sold in the All Other 33.30% models, says Bob Baird, vice president for appliance merchandising at Home Depot (HD). "Right U.S. relative to what U.S. DOC/ITA determined to be | Korea Daewoo 82.41% 79.11% now they're a premium brand, but you can't be No. I without capturing the core of the market, " says the fair market value of the appliances, a controversial LG 12.15%% 12.15% Baird, whose company began selling Samsung products at the end of 2012.4 calculation. These firms would now be required to post Samsung 9.62% 9.620 a cash deposit upon entry into the United States. All Others 1.36% 11.36% A final driver of differentiation between manufacturers was in advertising. The most recent data on ad- * Cash deposit rate reflects the offset of the export subsidies vertising expenditures by appliance brands in the U.S. showed a relative balance. Whirlpool had led with $54 found for Daewoo in the companion Countervailing Duties million, LG $33 million, GE and Samsung at $29 million, and Electrolux with $30 million. But there was an Although Whirlpool filed the original dumping | investigation, which was 3.30%. complaint, it refused to cooperate in the cost and price additional benefit with Samsung and consumer name recognition; Samsung had spent roughly $600 million in discovery requested by the U.S. DOC/ITA regarding Source: "Fact Sheet: Commerce Preliminarily Finds Dumping total in U.S. advertising in 2012 across all of its retail products, led by smart-phone promotion. of Imports of Large Residential Washers from Mexico and its Mexican operations. It was therefore also assessed a | the Republic of Korea," U.S. Department of Commerce/ Competition in the U.S. appliance market was fierce, complex, and changing. Exhibit 2 provides a sum- dumping margin. (Whirlpool had built a large portion |International Trade Administration, 2012, p. 3. of its washers and dryers sold in the U.S. in Mexico for mary of segment results (appliance segment depending on firm and reporting) of the major competitors for the many years, but soon after the government's finding, it most recent full year, 2013. ceased these imports.) Dumping Failure to cooperate analysis is termed adverse facts available (AFA). Samsung in Mexico similarly was based GE's renewed investment in appliances, however, was undermined in the market by South Korean competitors on AFA. Of the Korean manufacturers operating out of Korea, Daewoo was based on an AFA analysis. Korean undercutting price. Both LG and Samsung began flooding the U.S. market with better pricing, and in some manufacturing was also found to be subsidized by the Korean government, a finding denied by both the manu- cases better features, taking large chunks of market share. Finally, in late 2011, the leader in appliances in both facturers and the government. Electrolux was also hit with an antidumping duty of 33.30% for the washers and the U.S. and the global market, Whirlpool, filed a complaint with the U.S. Department of Commerce and the dryers manufactured in Mexico. U.S. International Trade Commission alleging dumping of large residential washers by manufacturers from Mexico and South Korea. Whirlpool had also filed a dumping complaint against LG and Samsung refrigerator products sold in the United States. Although the U.S. Commerce Department had proposed countervailing duties (against Korean "Large Residential Washers From South Korea and Mexico: Antidumping and Countervailing Duty Petitions on Behalf of "Samsung Wants to Be the World's Biggest Appliance Maker by 2015," Sam Grobart, Bloomberg, January 9, 2014. Whirlpool Corporation," Before the U.S. Department of Commerce and the U.S. International Trade Commission, Case Nos. A-201-841 (Mexico), A-580-868 (Korea), and C-580-869 (Korea), Volume 1, December 30, 2011, p. 1.government subsidies) and antidumping duties (against sales in the U.S. below fair market value), the U.S. trade panel had concluded that the imports did not threaten Whirlpool's business. Exhibit 5. U.S. Major Appliance Sales, 2004-2013 Millions of unit As shown in Exhibit 4, Whirlpool held the dominant share in the U.S. market, largely through its acqui- 70 sition of Maytag in 2006. But what was also apparent was the rise of LG and Samsung, the new major Asian U.S. real estate markets (Korean) players, most of it at the expense of the established big three. This market share growth was not just in decline rapidly, 2006-2007 washers and dryers (now subject to tariffs), but in the refrigerator/freezer segment as well. As one analyst noted: 'We view the appliance market industry as one of the worst end-markets in our capital-goods uni- 64 verse, " Rob Virdee, an analyst at Espirito Santo in London, said in a note. "There is still chronic global overcapacity and the value proposition of appliance manufacturers is poor. " 62 U.S. financial crisis, Major appliance sales 60 September 2008 -25% over 9 year period Exhibit 4. U.S. Appliance Sellers' Market Shares, 2008 & 2013 Percent of Market 58 40% Appliance sales at 52.3 million units in 2013 35.9% 54 35% 52 30% 30.4% 2008 50 24.8% 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 25% 2013 20.8% 20% 18.9% Source: Euromonitor. 15.9% 15% 14.0% Electrolux 10.5% 10% 8.5% 9.6 8.4% AB Electrolux (OMB: ELUX B; ADR: ELUXY), headquartered in Stockholm, Sweden, started life as a kerosene amp company called AB Lux in 1901. In 1919, in a new combination of companies, its name was changed to 5% Elektrolux, and eventually Electrolux. By 2014, it was selling products in 150 countries. 2.3% If you were to create a company that's emblematic of the global economy, it might look a lot like Whirlpool GE LG Samsung Electrolux Other Electrolux. It's based in Sweden, but holds its board meetings in English, the world's common lan- Source: http://www.statista.com/statistics/296707/market-share-of-appliance-producer-companies-united-states/. guage. Top managers come from countries that include Brazil, Jamaica, and Germany. The CEO from West Point.8 who took over when Straberg left last year is a U.S. citizen named Keith McLoughlin, who graduated GE's vision of an American Renewal was floundering. Energy and transportation costs had fallen, product innovation was not confined to the U.S., and new low-labor-cost countries from Hungary to Thailand were Although the second largest appliance maker in the world behind Whirlpool, Electrolux, too, had long home to new appliance manufacturing facilities. struggled with labor costs. In the late 1990s, it had closed manufacturing facilities across Western Europe (in- cluding its home country of Sweden), shifting significant production to lower-labor-cost Eastern Europe. In the What was of even greater concern to GE wasn't its declining market share, but the declining market. Ex- process, it had reduced global headcount by 12,000. In a series of renewed cuts, the company had shed another hibit 5 shows a 25% decline in major appliance sales in the U.S. over the 2004 to 2013 period. (The Western 30,000 jobs worldwide between 2002 and 2014, moving from just 20% of its production in low-cost countries European market had seen a similar decline, roughly 20%). The data led many in GE to believe the U.S. market to more than 60%. In 2014, Electrolux employed 52,000 worldwide. had suffered a permanent structural shrinkage. Electrolux saw the GE Appliances brand as a major competitive entry in the mid-price segment of the GE's leadership once again came to the same conclusion: The appliance segment was not a category in market, between its own premium brand, Electrolux, and its base-market-priced line of Frigidaire (which it had which GE would be able to grow sales and profits to its expectations-it was time to sell the business. In July owned since 1986). Electrolux had already studied the potential impacts of GE Appliances on its own sales and 2014, GE put GE Appliances on the market again, and made it clear that it would attach a much lower price market shares by global market. If, for example, Electrolux and GE had been combined the previous year, 2013, tag this time. Analysts estimated an eventual sale price of between $2.0 and $2.5 billion dollars. Electrolux's North American sales would have been SEK 37.5 billion greater (SEK 69.1 instead of SEK 31.6). $2 billion for GE Appliances? I mean, I get that Appliances isn't the best business at GE. Revenues But GE Appliances was distinctly a North American entity, and as illustrated in Appendix 5, it would have had at the unit are down 18% from 2008. Appliances' operating profit margin, at just 4.5%, is less than little impact on any other of Electrolux's major regions. half the profit margin for GE as a whole. But even so, a $2 billion price tag on Appliances works out to only about 0.25 times this unit's annual sales, and a mere fraction of the 1.8 times sales valuation Electrolux had struggled to reduce costs in the U.S. market. It had moved production of cooking appliances on the rest of General Electric stock. It's 25% of what GE thought the business was worth six years from L'Assomption, Quebec, to Memphis, Tennessee, reducing the average hourly wage of workers from $18.92 ago, and just $1 billion more than what GE sank into reviving the Appliances business less than to $14.65. (When Electrolux company executives met with Quebec workers to announce the shutdown of the four years ago! ? "Straberg's Strategy: Cutting Costs Led Electrolux to Memphis," Daniel Connolly, The Commercial Appeal, September "Electrolux to Cut Costs and Jobs as Profit Misses Estimates," Katarina Gustafsson, Bloomberg, October 25, 2013. 18, 2011. "Is General Electric Company About to Make Its Biggest Mistake Ever?" The Motley Fool, July 19, 2014.L'Assomption facility, they spoke in English, and were shouted down and heckled throughout.) It had closed The valuation team had started first on the core element-the valuation of GEA alone. As seen in Exhibit plants in Greenville, Michigan (refrigerators), and Webster City, Iowa (washers and dryers), moving production 7, this was based on the basic numbers provided by GE for the 2013 and 2014 (to date) years, combined with to a new plant in Ciudad Juarez, Mexico (the border city across the Rio Grande River from El Paso, Texas). Juarez some of Electrolux's own U.S. sales forecasts. Top-line growth assumptions were the big drivers, and, as seen, operations had an average hourly wage of $2.18. 2015 was forecast to be strong, followed by moderate growth (for conservatism). Despite these efforts, Electrolux globally suffered from no growth and marginal profitability. As seen in Exhibit 7. Valuation of GE Appliances Using DCF Analysis (millions of US Dollars sales had actually fallen over the past decade, with only modest returns. It had noted in its 2013 annual report to shareholders that it had four specific financial goals: 6% operating margin (at least); a capital turnover GE Appliances Actual Actual Projected Projected Projected Projected ratio of 4x (at least); 20% return on net assets; and 4% average annual growth (at least). Projected Income Assume 2013 2014 2015 $5,988.4 2016 2017 2018 Revenue (USD, millions) $5,700.0 $5,814.0 $6,168.1 $6,353.1 $6,543.7 Revenue growth (%) 2.00% 3.00% 3.00% 3.00% 3.00% Exhibit 6. Electrolux Global Sales and Profits (billions of Swedish krona, SEK) Less direct & indirect costs 2.0% (5,345.0) (5,451.9) 5,560.9) (5,672.2) (5,785.6) (5,901.3) EBITDA 355.0 362.1 427.5 495.9 567.5 642.4 Sales (billions of SEK) Returns (percent of sales) EBITDA margin (%) 6.2% 6.2% 7.1% 7.6% 3.9% 9.8% 140 9.28% 10.0% Depreciation (175.6) (179.4) (190.6) (192.4) (192.4) (192.4) EBITDA EBIT 179.4 182.7 236.9 303.5 375.1 120 Sales 9.0% 450.0 8.03 206% 7,23% 7.58% 8.0% GE Appliances 4 DCF Valuation 2013 2014 2015 2016 2017 2018 100 7.0% EBIT $179.4 $182.7 $236.9 $303.5 $375.1 $450.0 6.0% Less recalculated taxes 40% (71.8) (73.1) (94.8) (121.4) (150.0) (180.0) Add back depreciation 175.6 179.4 190.6 192.4 192.4 5.0% Net Operating Cash Flow $283.2 $332.7 $374.5 192.4 $289.0 $417.5 $462.4 60 Net Income 3.50% Sales 4.0% Present Value factor 10% 1.000 0.909 0.826 0.751 0.683 PV of NOCH 289.0 302.5 309.5 313.7 315.8 40 3.0% Net Present Value (NPV) $1,531 2.0% * Estimated sales based on the first 6 months. ** Electrolux corporate finance policy was to use 10.0% for all dollar 1.0% This baseline valuation isolated net operating cash flow for GE Appliances for the first four years, the pres- 0.0% 2001 2002 2005 2006 2007 2008 2010 2011 2012 2013 ent value of those cash flows totaling $1.531 billion. It was a very basic valuation, but as one member of the team noted-a start. The team identified three specific topics for expanded analysis: (1) expanding the years of coverage beyond the current four years (2015-2018); (2) adding capital expenditure (capex); and (3) including Strategically, the combining of Electrolux and GEA would increase Electrolux's potential in the world's changes in net working capital (NWC). The analysis would also need to evaluate a number of different sales and most profitable appliance market-the U.S.-and put the company on par with the dominant market player in cost growth scenarios. that market, Whirlpool.' Electrolux could benefit substantially through GE's expanded market footprint, both in manufacturing and in marketing and distribution. The GE brand was a stronger player in the middle of some Expanded Years. The GE appliance business would most likely continue far into the future. In financial analy- appliance brand brackets, like those in refrigerators. sis, this was usually captured by using a basic five- to seven-year period of detailed financial projection like that An added element of strategic value was that the deal would also include GE's ownership interest in Mabe for years 2015-2018 in Exhibit 7, and then including a terminal value (TV)-continuing value-to capture the (Mexico), one of the strongest appliance makers in Latin America. The final benefit of the deal was the cost estimated cash flows. The team supported seven years of detailed value, and the use of a terminal value in year and operational efficiencies that would be gained by combining Electrolux and GE appliance operations in the seven that would capture all years following. After considerable debate between a value based on multiples versus U.S.-synergies-so often noted in mergers and acquisitions. discounted values, they agreed to use discounted values." But that did not end the debate. Several team members noted that too many valuations ended up being Financial Valuation dominated by the TV component, typically the result of some aggressive assumption of how much cash flows The valuation team had identified three separate value elements in the GE Appliances deal: (1) GEA itself; (2) would grow into the future (g). In the end, it was agreed that they would conduct valuations with and without GE's interest in the Mabe joint venture; and (3) synergies to be gained by Electrolux once combined with GEA. IVs, and when including a TV, limit assumptions of growth g to between -1% and +1% per annum. GE Appliances Capex. No business could be sustained without some minimal amount of annual reinvestment. In the case of GE Appliances, GE itself had recently reinvested heavily in North America, so that the technology and facilities First, GE Appliances had been a stable marginally profitable business for many years. In the current year, as seen now in use were clearly of a recent vintage. The valuation team, however, disagreed over the general approach in Exhibit 5, the EBITDA margin was at 6.2%, making it near the absolute bottom of most GE businesses. Yet, to new investment. Previous investment in the business created the depreciation charges being included in the at 6.2%, GE Appliances was on par with most other major U.S. and North American appliance manufacturers. Electrolux believed that if it had the continued use of the GE brand, and the general economy held steady and 10 Note that the Electrolux valuation team's analysis was conducted in U.S. dollars (USD), using a dollar-based discount healthy for five to seven years into the future, GE Appliances was a good value. rate of 10.0%, for all GE Appliances analysis. "The discounted cash flow terminal value calculation uses the traditional expression: Note that when Electrolux estimated what the company would have looked like if it had been combined with GE in 2013 Terminal value 2018 = NOCF 2018 (1 + 8) Appendix 5), nearly the entire change in global sales, an added SEK 37.5 billion, was in the United States. kwace - 8income forecast. If those depreciation charges were to actually continue (and not just diminish as the capital investments became fully depreciated), new capital investments would need to be made. Although one team Exhibit 8. Mabe of Mexico's Forecasted Income and GE's Share (millions of US dollars) member argued that new investment and depreciation would annually be "roughly the same," others noted Mabe of Mexico Actual Projected Projected Projected Projected Projected that capital investments would likely exceed depreciation in the future as all costs, operating and capital, always Projected Income Assume 2013 2014 2012 2016 2017 2018 seemed to increase over time. Revenue (USD, millions) $2,900.0 $3,010.2 $3,124.6 $3,243.3 $3,366.6 $3,494.5 Revenue growth (%) 3.80% 3.80% 3.80% 3.80% 3.80% Net Working Capital. Net working capital (NWC) management was a challenge in appliances. Whirlpool had Less direct & indirect costs 3% (2,633.0) (2,712.0) (2,793.3) (2,877.2) (2,963.5) (3,052.4) always been considered the champion in the U.S., posting a 2013 NWC balance of 1 1 days of sales, based on 39 EBITDA 267.0 298.2 331.2 366.2 403.1 442.1 days of receivables, 47 days of inventory, and 75 days of payables. Yet, with GE's application of lean manufactur EBITDA margin (%) 9.2% 9.9% 10.6% 11.3% 12.0% 12.7% ing practices across its manufacturing units in recent years, it was expected to match or even surpass Whirlpool's Depreciation (116.0) (116.0) (116.0) (116.0) (116.0) EBIT (1 16.0) 151.( 182.2 215.2 250.2 287.1 326.1 operating excellence. It was also noted that changes in NWC were only significant in valuation work when sales Interest -10% 48.0 (43.2) (38.9) (35.0) (31.5) (28.3) changed dramatically, not often seen in appliances. EBT 103.0 139.0 176.4 215.2 255.6 297.8 Taxes 30% (30.9) (55.6) (70.5) $105.8 (86.1) (102.2) (119.1) Mabe Interest Net income 72.1 $83.4 $129.1 $153.4 $178.7 Return on sales (%) 2.5% 2.8% 3.4% 4.0% 4.6% 5.1% The second component, and possibly the most difficult to value, was GEA's 48.5% ownership in Mabe of Mexico. Mabe (Controladora Mabe S.A. de C.V.) was a leading player in Mexico and Latin America, with strong brand GE's share of Mabe profits 48.5% $35.0 $40.45 $51.32 $62.62 $74.38 $86.66 recognition and a wide geographic footprint. Operating in more than 70 countries, Mabe held a 50% market Present Value factor 10% 1.000 0.909 0.826 0.751 0.683 share in Mexico and the Caribbean, and a strong 25% market share across Central America. PV of GE cash benefits 40.5 46.7 51.7 55.9 59.2 Cumulative PV $254 Mabe, privately held, had entered into a partnership with GE in 1987 in which Mabe would be an important * Estimated sales based on the first 6 months. ** Electrolux corporate finance policy was to use 10.0% for all dollar-based subcontractor to GE. The partnership would give GE access to cheaper Mexican labor, while giving Mabe access acquisition valuations. to a global network for sales and distribution. Initially, Mabe produced just stoves and refrigerators for GE, but after it acquired GE Canada in 2005, it became a major supplier of clothes dryers and dishwashing appliances to Cost Synergies. Cost synergies are reduced operating expenses associated with running combined businesses after GE Appliances as well. At one point, Mabe was supplying between 40% and 50% of all GE appliances, designed acquisition. They are realized by eliminating duplication in activities and overhead across the businesses in the and manufactured in Mexico for sale in the U.S. With GE's renewed investment in U.S. manufacturing facilities post-acquisition integration process. Electrolux believed that there would be about $300 million per year in per- in the past four years, that percentage had dropped to 20%. manent cost savings arising from the integration of GE Appliances and Electrolux operations in North America. It was estimated that $200 million would arise from combining manufacturing operations (taking advantage of Exhibit 8 illustrates the valuation team's preliminary attempt at estimating the value of GE's interest in the newly renovated GE Appliances manufacturing operations), with an additional $100 million per year arising Mabe. As a privately owned firm, financial details on Mabe were difficult to get. What Electrolux did know was from common sourcing and reduced overhead Mabe's top and bottom lines in 2013, and GE's subsequent 48.5% share of profits, $35 million. The team estimated, internally, that to take full advantage of GE's existing North American operations Mabe still played a valuable role within GE, representing GE in many markets. As noted previously, Mabe would require $300 million in reorganization expenses (including write-offs), plus an additional $60 million in owned GE Appliances Canada, as well as holding marketing rights to appliances sold throughout Latin America capital expenditures (investment). As illustrated by the valuation team's preliminary calculations in Exhibit 9, under the GE brand. Although this structure was both logical and effective for GE and GE Appliances, it was not both expenses and investments would be spread out over the first two years. Once completed, however, Elec- clear that would be the case if GE Appliances was purchased by Electrolux. Some analysts wondered if Electrolux/ trolux believed it would save $300 million per year (half that amount in 2015 as the reorganization proceeded), GE wouldn't result in Mabe/GE competing against other Electrolux products in many Latin American markets. in its existing sales and operations in North America. This was significant and could potentially be even larger Others argued that a combined Electrolux/Mabe product line would be highly successful, with Electrolux already over the long run. having a premium presence in Brazil, Chile, Argentina, Central America, and the Caribbean, and Mabe being a market leader on a volume basis in all of these same markets except Brazil." A variety of outcomes were possible, Exhibit 9. Synergies Accruing to Electrolux of Acquisition (millions of US dollars) including Electrolux ending the GE brand licensing agreement with Mabe or, alternatively, Electrolux choosing to acquire Mabe outright at some future date. Electrolux US Operations Projected Projected Projected Projected Projected Projected Synergy CF Assume 2014 2015 2016 2017 2018 Synergies Revenue synergies 50.0 100.0 150.0 200.0 Operating cost savings 150.0 300.0 300.0 300.0 Often promised, seldom delivered. Reorganization expenses (150.0) 150.0) Common critique of synergy justifications in acquisitions Capex for reorganization (30.0) (30.0) Net cash flows from synergies (180.0) 20.0 400.0 450.0 500.0 The third valuation component to be considered was the benefit to Electrolux of synergies gained by combining Taxes 40% 72.0 (8.0) (160.0) (180.0) (200.0) the two companies. The predominant potential synergies in an acquisition were revenue, cost, managerial, tax, Net operating cash flows NOCF (108.0) 12.0 240.0 270.0 300.0 and financial. In this case, since both firms were considered to have had sufficient access to capital for reinvest- ment purposes in recent years, and were primarily focused on combining U.S. operations and sales, the team Value factor 10% 1.000 0.909 0.826 0.751 0.683 dismissed tax and financial and focused on cost, revenue, and management. PV of NOCF (108) 11 198 203 205 Cumulative PV $509 2 In 2009, Mabe had acquired Bosch Siemens Haushaltsgerate Home Appliances in Brazil at a steep price financed heavily with debt. Mabe had been unable to generate a sustained profit with the new acquisition, and in 2013 filed bankruptcy in Brazil, defaulting on more than $400 million in debt obligations.Revenue Synergies. Rev/mu: synergia are opportunities of a combined corporate entity to generate more revenue than its two predecessor stand-alone companies were able to generate individually. The primary revenue synergies envisioned by the Electrolux team were based on GE's greater geographic reach in the US. Although both GE and Electrolux appliances were sold throughout the U.S., GE's greater logistics capabilities were thought valu- able. GE had ils own distribution and logistics network that supported what GE called its direct ans-rte}: retail channel strategy. This meant getting Electrolux products in front of more potential customers. After considerable debate, the valuation team had concluded that this might add $100 to $200 million in additional sales per year, but as opposed to cost synergies, these were closer to guesses. Management Synetyes. Management synergies, sometimes called control synergies, were typitu described as the new owner's ability to run the business better than die previous owner. GE, however, was generally considered a very capable orynization in the execution of all its businesses, even appliances. Electrolux was considered managerially e'icient by European standards, but the valuation team (and Fleccrolux's leadership team) did not expect major benets from new management. Leadership of acquirers often championed deals on the basis of synergies, but many postacquisition studies indimted that promised synergies were never achieved. In fact. a multitude of studies had concluded that nearly twothirds of acquisitions failed to create value for the owners of the acquiring company bemuse of overpayment, payment justied on the basis of synergies. In the case of publicly traded rms, all studies indicated the same results from an acquisition announcement: the acquirer's share price fell. the acquisition target's share price rose. There were, however, three deal components that characterized successful synergy capture. First, that the two companies were large in scale, so that post-acquisition overhead and management cost reductions were ma- terial in size. Second, that the two companies had signicantbut not completebusiness segment overlaps. This yielded awealth of opportunities to cut costs by cutting duplication and simultaneously leveraging access to customers for revenue enhancement. Third, that the acquiring company did not pay the seller full value for the prospective synergies. Synergy values were achievable only by the acquiring company, not the seller. Yet, as noted by a recent Boston Consulting Group study, paying the seller some portion of the synergy wlue facilitated deals: By sharing the value of synergies with the seller, the acquirer can pay a price that induces the seller to conduct the transaction while still enabling bath acquirer and seller to create value for their shareholders. Further, by disclosing the value of potential synergies at the time of an acquisition, the acquirer can share up its market valuation during the period following the merger announcement, aimring the ems-inn in market value that frequently occurs as investors react to the uncertainty engendered by such announcements." In this case, the Electrolux valuation team's preliminary analysis, as seen in Exhibit 10, estimated that potential symergies brought an additional $500 million in value to the deal. Risk: The potential deal faced a number of risks. First, the deal might run into opposition from the US. government on antitrust grounds. The combined Electrolux and GE appliance businesses would total net 40% in the U.S. marketplace, a value traditionally seen as a threshold for trouble. Although each appliance was different, the largest share: would be in cooking and refrigerators/freezers, with smaller shares in laundry appliances. When \Vhirlpool acquired Maytag in 2006, the same antitrust concerns were debated, again because the combined rms would have a market share of over 40%. In the end, the Commerce Department had allowed die acquisition to go through unopposed on the basis of the Bush administration's general philosophy of no intervention, specimlly noting the growing competitive strength of Asian manufacturers imposing a strong competitive pressure on prices. That same price pressure was no longer as eEective as a result of the antidumping tariffs, and the Obama administration had been distinctly hostile toward industrial consolidation. a "How Successful mam our: Split the Synerg'es: Divide and conquer," Jens Kengelbach, Dennis Urunlh, Christoph Kaseret, and Sebastian Schatt, BCG Perspectives, March 27, 2015. thibit 10. Values GE Appliances May Bring to Electrolux Billions of USD Pm Forum Enterprise m... $0.509 SIIJISZ } 4.3% } 2.1% cc Applllnres Value Electmlux Enterprise Vllur Nok: Enterprise v-ne- Mum capitalisation r Debi + Penslol Obligations In the US. market, it was also possible that there would be some cannibalization of GE or Electrolux sales as a result of the combination. Although proponents of the deal emphasized cost and operating benets, there was little information on how consumers would respond to the combination. In the end, the estimation of the value of synergies was a far cry from achieving those synergies. Acquisition history was littered with hundreds of deals that never achieved promised synergies and never created value for stockholders. Ekmlux's Bid Strategy Electrolux was a motivated buyer, and GE was clearly a motivated seller. Electrolux wanted to gain GE's brand, newly refreshed manufacturing technology, and marketing and sales sale in the United States. But the two companies knew each other well as competitors. As noted by one Electrolux executive, "We have danced before." But FJectrolux was not the only suitor of GE Appliances; it was rumored that other appliance companies were lining up for the purchase as well, including China's Haier and Mexico's Mabe, two companies with limited to little current presence in the U.S. and Canada. The valuation team now had to cycle again through the mious valuation components and then nalize their valuation and bidding strategy Time was short. Appendix 1. Electrolux Income Statement and Outlook (mission of Swedish krona, SEK) Electrolux 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E Sales 135,803 133,150 124,077 120,651 129,469 103,848 104,732 104,792 109,132 106,326 101,598 109,994 109,151 111,177 Labour costs -26,816 -25,731 -22,759 -22,656 -22,421 -16,924 -16,857 -16,020 -14,848 -16,375 -16,237 -17,057 -16,633 -17,157 Purchased raw material -23000 -23000 -23000 -19000 -20285 -20000 -20000 -19000 -19058 Other operational costs -98,429 -95,850 -90,758 -90,130 -96,676 -56,591 -57,300 -59,839 -66,520 -59,794 -58,159 -64,604 -65,550 -66,528 EBITDA 10,558 11,569 10,560 7,865 10,372 7,333 7,575 5,933 8,764 9,872 7,202 8,333 7,968 8,434 Depreciation -4,020 -3,171 -3,023 -3,410 -2,758 -2,738 -3,010 -3,442 -3,328 -3,173 -3,101 -3,206 -3,378 EBITA 6,538 7,937 7,389 4,842 6,962 4,575 4,837 2,923 5,322 6,544 4,029 5,232 4,762 5,056 Goodwil -257 -230 -182 -155 0 0 0 0 0 0 -150 -150 -150 EBIT 6,281 7,707 7,207 4,687 6,962 4,575 4,837 2,923 5,322 6,544 4,029 5,082 4,612 4,906 Net financial costs -1,207 -596 -664 -2,288 -3,747 -750 -802 -2,270 -1,868 -1,238 -1,249 -1,754 3,708 -2,706 EBT 5,074 7,111 6,543 2,399 3,215 3,825 4,035 653 3,454 5,306 2,780 3,328 904 2,200 Minority 132 -2 -1 0 0 0 0 0 0 - 3 -1 4 -1,477 -2,459 -2,226 -1,210 -1,452 -1,177 -1,110 -287 -877 -1,309 -716 -879 -232 -572 Tax Net profit 3,729 4,661 4,315 1,188 1,763 2,648 2,925 366 2,577 3,997 2,064 2,446 671 1,624 Reported EPS 0.96 14.25 13.77 3.98 6.05 9.17 10.41 1.3 9.07 14.04 7.25 8.56 2.34 5.67 Source: Keplercheuvreux, p. 32 and author calculations. Weighted Average Cost of Capital (WACC) Percent of total Equity value (SEK) Share price (SEK) Shares outstanding Equity Capital Cost of equity Electrolux beta Market risk premium Bond rate Cost of Equity 70 90 110 130 150 170 190 173/2000 4/3/2000 713 2000 10/3/2000 4/3/2001 10/3/2001 1/3/2002 4/32003 7/3/2002 52,075,660,000 Debt outstanding 10/3/2002 1/3/2003 286,130,000 /3/2003 10/3/20 23 Share Price (Swedish krona, SEK) 81.8/0% 182 Percent of total Debt Capital Cost of debt after-tax 9.500% Tax rate 1.30 Cost of debt 4.000% Electrolux credit risk premium 4.300% Risk free rate Values Cost of Debt Appendix 3. Electrolux's Cost of Capital and Capital Structure (In Swedish kroner, SEK) 1/3/200 10/3/2004 1/3/2005 43/2005 73 ROW 10/3/2005 2732006 102 5206 1/3/2007 4/3/2007 7/3/2007 10/3/2002 1/3/2008 7/32008 1/3/2009 4/3/2009 11,532,000,000 63,607,660,000 10/320 09 1/3/2010 4/3/2010 7/3/2010 26.000% 10/3/2010 18. 130% 4.070% 5.500% 1.200% 4.300% Values 1/3/201 1 7/3201/ 10/3/2011 732012 Appendix 2. Electrolux AB Share Price (Stockholm: ELUX-B, weekly, Jan 2000-July 2014) Total Capital 10/3/2012 1/3/2013 100.000% 4/3/2013 8.5155% 7/3/2013 10/32012 4/3/2014 7/3/2014Appendix 4. GE & Electrolux Plant Locations in North America ST. CLOUD, MN FREEZERS GE APPLIANCES E Electrolux BLOOMINGTON, IN 86 REFRIGERATORS 86 LOUISVILLE, KY LAUNDRY, DISHWASHERS, PLANT LOCATIONS REFRIGERATORS, WATER HEATERS SPRINGFIELD,TN [) COOKING APPLIANCES KINSTON, NC DISHWASHERS MEMPHIS, TN X96 COOKING APPLIANCES )ANDERSON, SC REFRIGERATORS SELMER, TN LAFAYETTE, GA REFRIGERATORS DECATUR, AL COOKING APPLIANCES REFRIGERATORS (JAUREZ, MEXICO REFRIGERATORS, VACUUM CLEANERS WDRB.com Appendix 5. How Acquisition of GE Appliances Would Have Changed Electrolux in 2013 Electrolux 2013 Electrolux + GE Appliances Percent of Sales by Sales Percent of Sales by Sales Change in Sales Segment Region/Product (SEK billion) Region/Product (SEK billion) (SEK billion) Major Appliances North America 29% 31.6 17% 69.1 37.5 Major Appliances EMEA 31% 33.8 23% 33.8 0.0 Major Appliances Latin America 19% 20.7 14% 20.6 (0.1) Major Appliances Asia Pacific 8% 8.7 6% 8.8 0.1 Small Appliances 8% 8.7 6% 8.8 0.1 Professional Products 5% 5.5 4% 5.9 0.4 100% 109.0 100% 147.0 38.0 SEK 6.515 = 1.0 USD USD 5.83 Source: Electrolux