Answered step by step

Verified Expert Solution

Question

1 Approved Answer

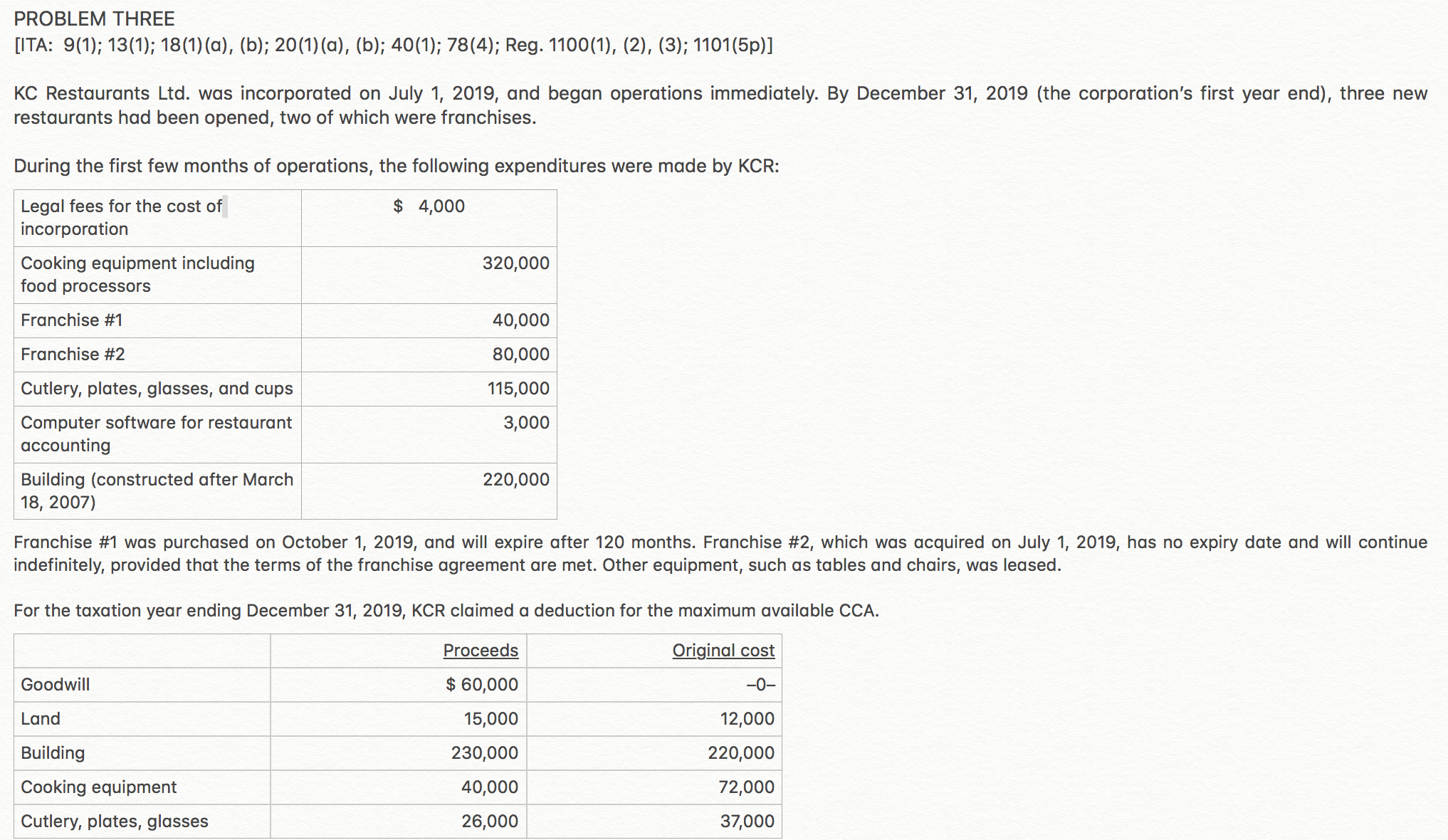

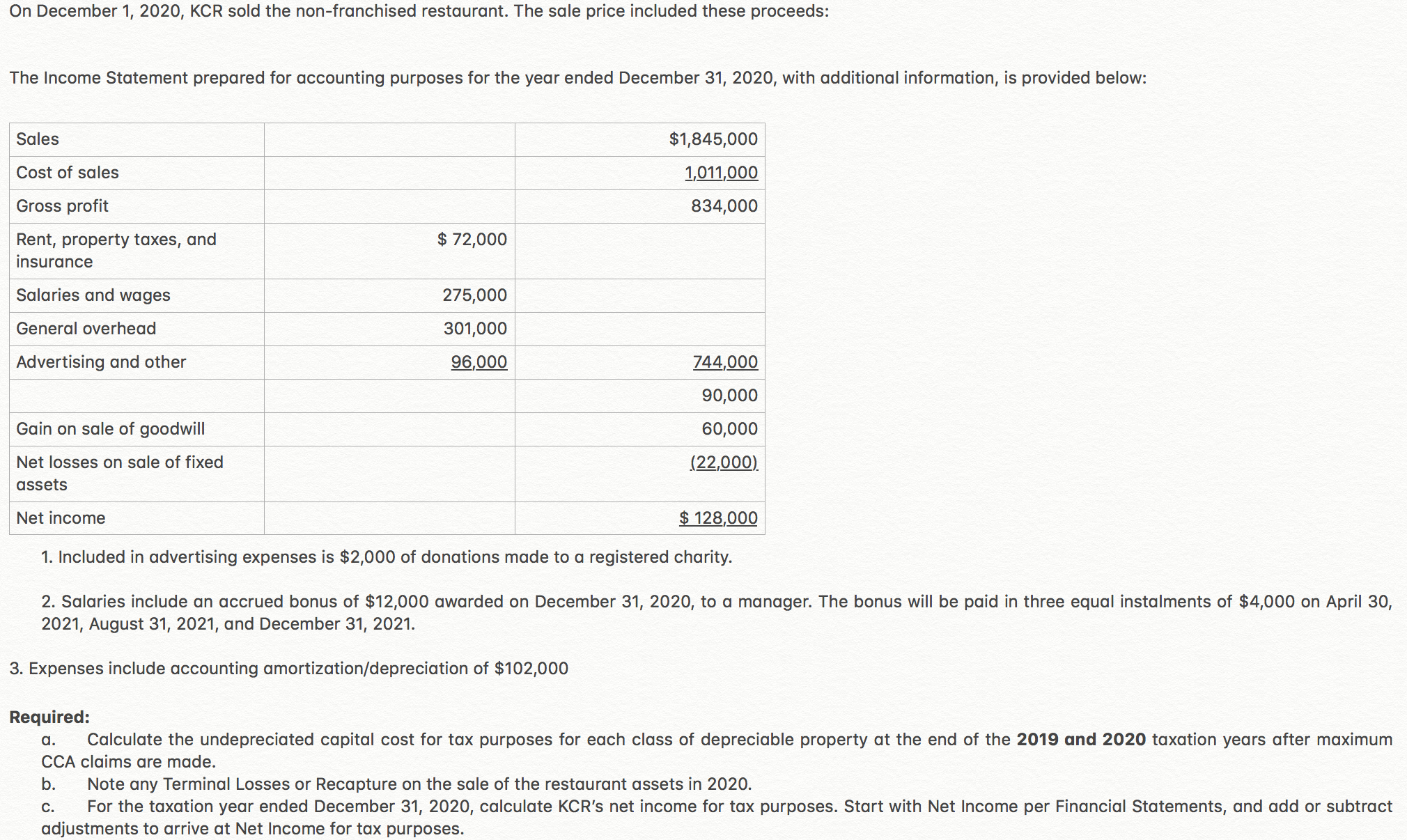

please see the two images attached for the full question PROBLEM THREE [ITA: 9(1);13(1),-18(1)(a),(b);20(1)(a),(b);40(1);78(4);Reg.11oo(1), (2). (3); 1101(5P)] KC Restaurants Ltd. was incorporated on July 1,

please see the two images attached for the full question

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Information Systems

Authors: George H Bodnar, William S Hopwood

10th Edition

013609712X, 978-0136097129