Question

PLEASE SHOW ALL STEPS WITHOUT USING EXCEL OR SPREADSHEETS! ABC Life Insurance Company enters into a one-year interest rate swap with a notional value of

PLEASE SHOW ALL STEPS WITHOUT USING EXCEL OR SPREADSHEETS!

ABC Life Insurance Company enters into a one-year interest rate swap with a notional value of 10 million. Under this swap, ABC will pay a variable interest rate each quarter and in return will receive a fixed interest rate each quarter. The variable interest rate will adjust each quarter to be the three-month spot interest rate at the start of each quarter.

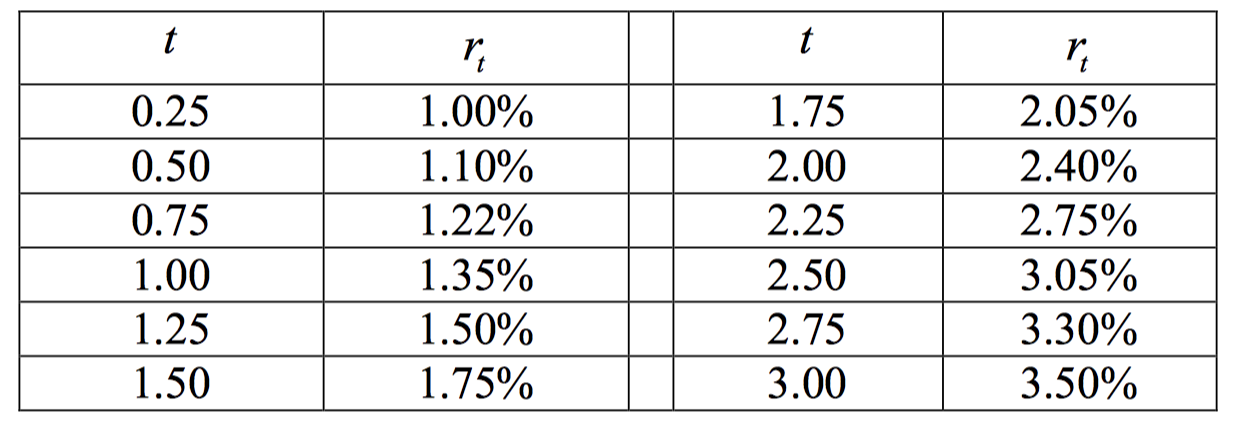

The spot interest rates at the time of the purchase of the swap are those in Table 1 but are repeated here for your convenience:

a. Determine the swap interest rate per quarter.

b. Determine the net swap payment that will be made at the end of the first quarter.

c. State whether ABC will receive the payment in b. or be required to make the payment in b.

t t 0.25 0.50 0.75 1.00 1.25 1.50 r 1.00% 1.10% 1.22% 1.35% 1.50% 1.75% 1.75 2.00 2.25 2.50 2.75 3.00 2.05% 2.40% 2.75% 3.05% 3.30% 3.50% t t 0.25 0.50 0.75 1.00 1.25 1.50 r 1.00% 1.10% 1.22% 1.35% 1.50% 1.75% 1.75 2.00 2.25 2.50 2.75 3.00 2.05% 2.40% 2.75% 3.05% 3.30% 3.50%Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance Turning Money Into Wealth

Authors: Arthur J Keown

5th Edition

0136070620, 9780136070627