Question

Please show all steps you take to get your answers. 1. The table below presents the returns on stocks ABC and XYZ for a five-year

Please show all steps you take to get your answers.

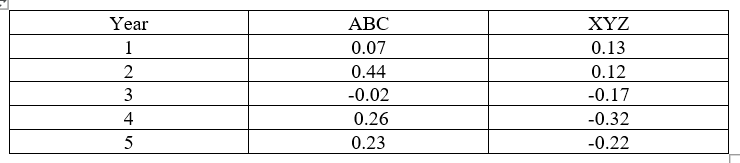

1. The table below presents the returns on stocks ABC and XYZ for a five-year period.

a. Calculate the average return and standard deviation of stock ABC and XYZ. Also, calculate the correlation between the two stocks. What does the correlation tell you about the return movements of the two stocks?

b. Calculate the weight of each stock in the minimum variance portfolio, assuming the expected return equals to average return for each stock.

c. Suppose the risk-free rate is 5%. Also assume the expected return equals to average return for each stock. Calculate the weights for the two stocks in the optimal risky portfolio; AND the return and risk (standard deviation) of the portfolio.

Year 1 2 3 4 5 ABC 0.07 0.44 -0.02 0.26 0.23 XYZ 0.13 0.12 -0.17 -0.32 -0.22 Year 1 2 3 4 5 ABC 0.07 0.44 -0.02 0.26 0.23 XYZ 0.13 0.12 -0.17 -0.32 -0.22Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Secured Finance Transactions Key Assets And Emergin Markets

Authors: Paul U Ali

1st Edition

1905783108, 978-1905783106