Answered step by step

Verified Expert Solution

Question

1 Approved Answer

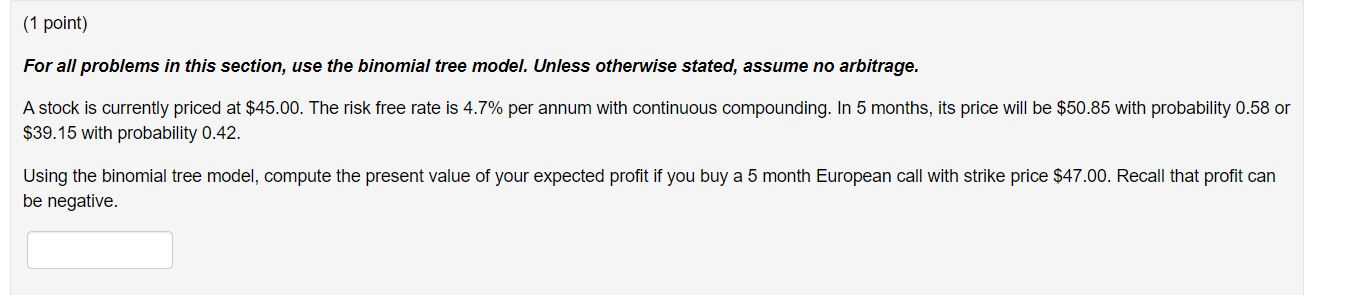

Please show all work thank you! (1 point) For all problems in this section, use the binomial tree model. Unless otherwise stated, assume no arbitrage.

Please show all work thank you!

(1 point) For all problems in this section, use the binomial tree model. Unless otherwise stated, assume no arbitrage. A stock is currently priced at $45.00. The risk free rate is 4.7% per annum with continuous compounding. In 5 months, its price will be $50.85 with probability 0.58 or $39.15 with probability 0.42. Using the binomial tree model, compute the present value of your expected profit if you buy a 5 month European call with strike price $47.00. Recall that profit can be negativeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Money Banking And Financial Markets

Authors: Stephen G. Cecchetti

2nd International Edition

0071287728, 9780071287722