Please show full solutions step by step, please and thank you so much. Truly appreciate it!

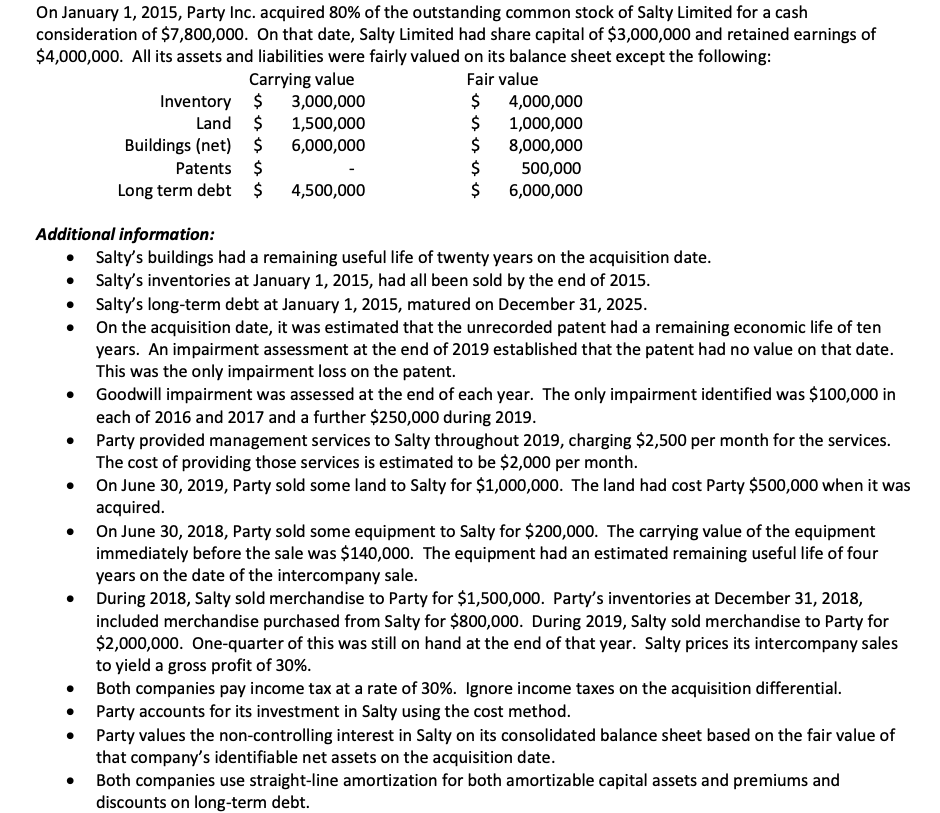

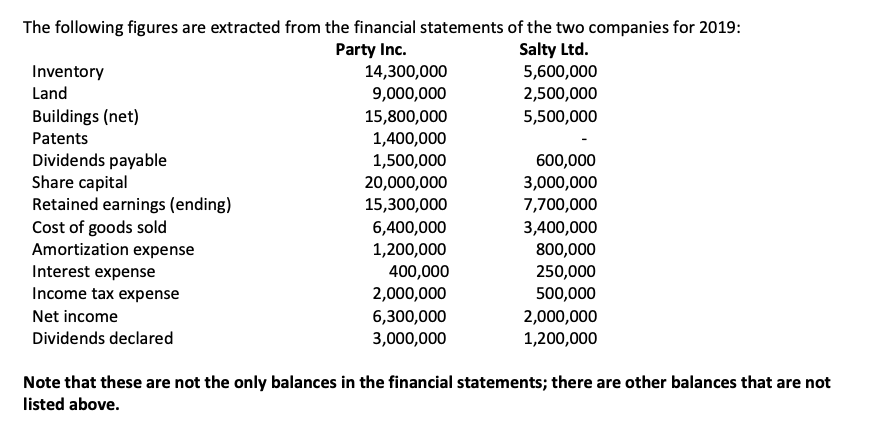

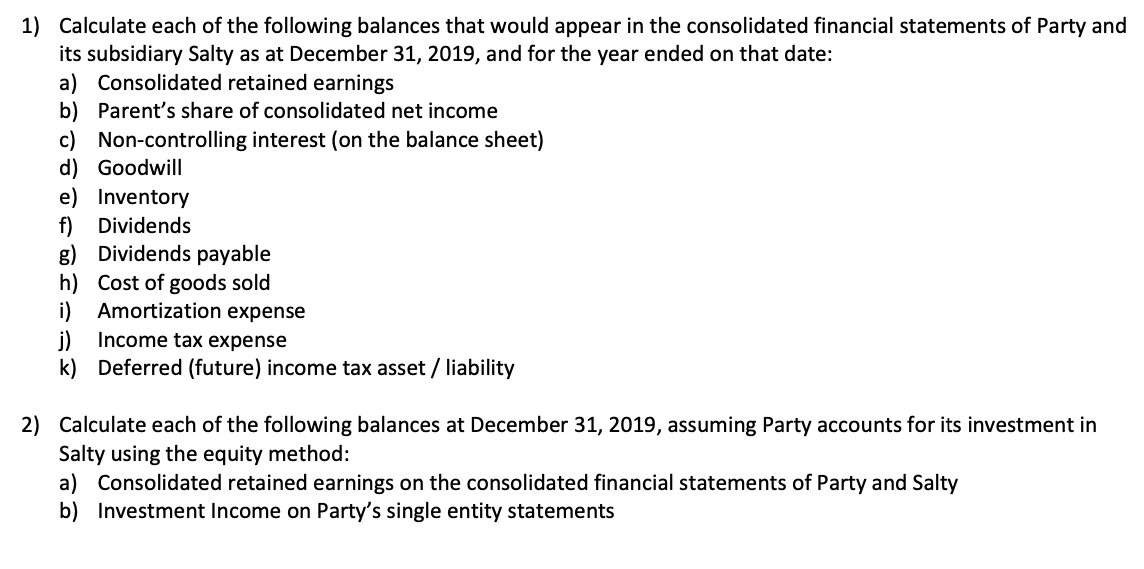

On January 1, 2015, Party Inc. acquired 80% of the outstanding common stock of Salty Limited for a cash consideration of $7,800,000. On that date, Salty Limited had share capital of $3,000,000 and retained earnings of $4,000,000. All its assets and liabilities were fairly valued on its balance sheet except the following: Additional information: - Salty's buildings had a remaining useful life of twenty years on the acquisition date. - Salty's inventories at January 1, 2015, had all been sold by the end of 2015. - Salty's long-term debt at January 1, 2015, matured on December 31, 2025. - On the acquisition date, it was estimated that the unrecorded patent had a remaining economic life of ten years. An impairment assessment at the end of 2019 established that the patent had no value on that date. This was the only impairment loss on the patent. - Goodwill impairment was assessed at the end of each year. The only impairment identified was $100,000 in each of 2016 and 2017 and a further $250,000 during 2019. - Party provided management services to Salty throughout 2019, charging $2,500 per month for the services. The cost of providing those services is estimated to be $2,000 per month. - On June 30, 2019, Party sold some land to Salty for $1,000,000. The land had cost Party $500,000 when it was acquired. - On June 30, 2018, Party sold some equipment to Salty for $200,000. The carrying value of the equipment immediately before the sale was $140,000. The equipment had an estimated remaining useful life of four years on the date of the intercompany sale. - During 2018, Salty sold merchandise to Party for $1,500,000. Party's inventories at December 31, 2018, included merchandise purchased from Salty for $800,000. During 2019 , Salty sold merchandise to Party for $2,000,000. One-quarter of this was still on hand at the end of that year. Salty prices its intercompany sales to yield a gross profit of 30%. - Both companies pay income tax at a rate of 30%. Ignore income taxes on the acquisition differential. - Party accounts for its investment in Salty using the cost method. - Party values the non-controlling interest in Salty on its consolidated balance sheet based on the fair value of that company's identifiable net assets on the acquisition date. - Both companies use straight-line amortization for both amortizable capital assets and premiums and discounts on long-term debt The following figures are extracted from the financial statements of the two companies for 2019: Note that these are not the only balances in the financial statements; there are other balances that are not listed above. 1) Calculate each of the following balances that would appear in the consolidated financial statements of Party and its subsidiary Salty as at December 31, 2019, and for the year ended on that date: a) Consolidated retained earnings b) Parent's share of consolidated net income c) Non-controlling interest (on the balance sheet) d) Goodwill e) Inventory f) Dividends g) Dividends payable h) Cost of goods sold i) Amortization expense j) Income tax expense k) Deferred (future) income tax asset / liability 2) Calculate each of the following balances at December 31, 2019, assuming Party accounts for its investment in Salty using the equity method: a) Consolidated retained earnings on the consolidated financial statements of Party and Salty b) Investment Income on Party's single entity statements On January 1, 2015, Party Inc. acquired 80% of the outstanding common stock of Salty Limited for a cash consideration of $7,800,000. On that date, Salty Limited had share capital of $3,000,000 and retained earnings of $4,000,000. All its assets and liabilities were fairly valued on its balance sheet except the following: Additional information: - Salty's buildings had a remaining useful life of twenty years on the acquisition date. - Salty's inventories at January 1, 2015, had all been sold by the end of 2015. - Salty's long-term debt at January 1, 2015, matured on December 31, 2025. - On the acquisition date, it was estimated that the unrecorded patent had a remaining economic life of ten years. An impairment assessment at the end of 2019 established that the patent had no value on that date. This was the only impairment loss on the patent. - Goodwill impairment was assessed at the end of each year. The only impairment identified was $100,000 in each of 2016 and 2017 and a further $250,000 during 2019. - Party provided management services to Salty throughout 2019, charging $2,500 per month for the services. The cost of providing those services is estimated to be $2,000 per month. - On June 30, 2019, Party sold some land to Salty for $1,000,000. The land had cost Party $500,000 when it was acquired. - On June 30, 2018, Party sold some equipment to Salty for $200,000. The carrying value of the equipment immediately before the sale was $140,000. The equipment had an estimated remaining useful life of four years on the date of the intercompany sale. - During 2018, Salty sold merchandise to Party for $1,500,000. Party's inventories at December 31, 2018, included merchandise purchased from Salty for $800,000. During 2019 , Salty sold merchandise to Party for $2,000,000. One-quarter of this was still on hand at the end of that year. Salty prices its intercompany sales to yield a gross profit of 30%. - Both companies pay income tax at a rate of 30%. Ignore income taxes on the acquisition differential. - Party accounts for its investment in Salty using the cost method. - Party values the non-controlling interest in Salty on its consolidated balance sheet based on the fair value of that company's identifiable net assets on the acquisition date. - Both companies use straight-line amortization for both amortizable capital assets and premiums and discounts on long-term debt The following figures are extracted from the financial statements of the two companies for 2019: Note that these are not the only balances in the financial statements; there are other balances that are not listed above. 1) Calculate each of the following balances that would appear in the consolidated financial statements of Party and its subsidiary Salty as at December 31, 2019, and for the year ended on that date: a) Consolidated retained earnings b) Parent's share of consolidated net income c) Non-controlling interest (on the balance sheet) d) Goodwill e) Inventory f) Dividends g) Dividends payable h) Cost of goods sold i) Amortization expense j) Income tax expense k) Deferred (future) income tax asset / liability 2) Calculate each of the following balances at December 31, 2019, assuming Party accounts for its investment in Salty using the equity method: a) Consolidated retained earnings on the consolidated financial statements of Party and Salty b) Investment Income on Party's single entity statements