Answered step by step

Verified Expert Solution

Question

1 Approved Answer

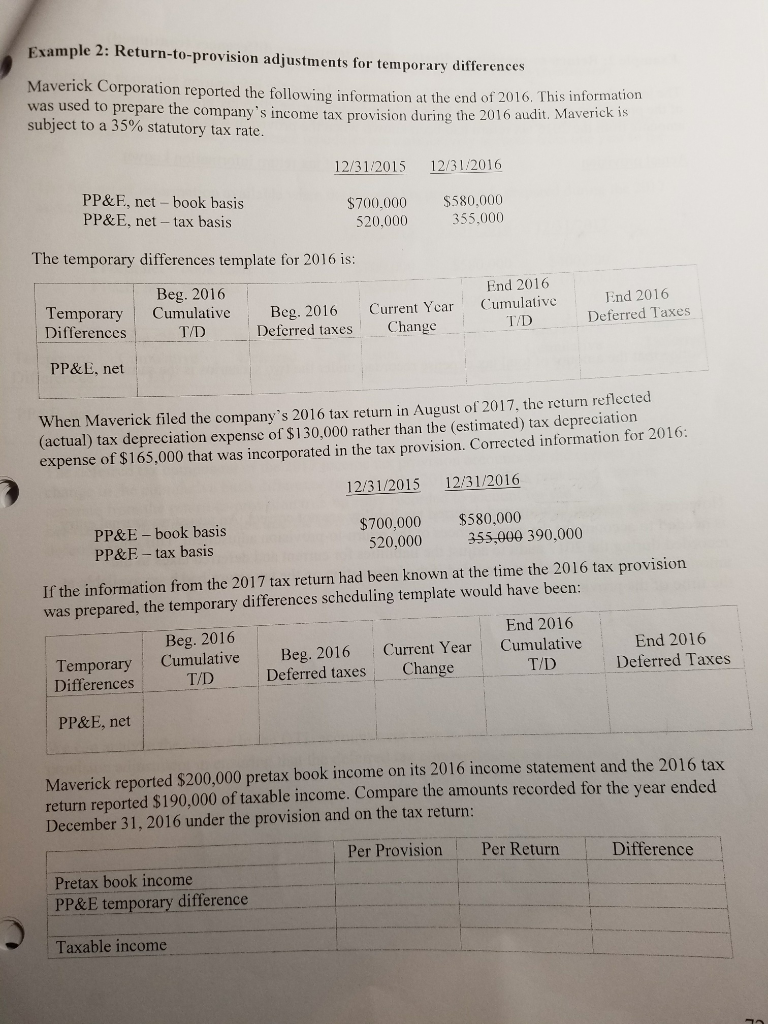

Please show solutions Example 2: Return-to-provision adjustments for temporary differences Maverick Corporation reported the following information at the end of 2016. This informati was used

Please show solutions

Example 2: Return-to-provision adjustments for temporary differences Maverick Corporation reported the following information at the end of 2016. This informati was used to prepare the company's income tax provision during the 2016 audit. subject to a 35% statutory tax rate. 12/31/2015 12/31/2016 PP&E, net - book basis PP&E, net-tax basis $700.000 520,000 $580,000 355.000 The temporary differences template for 2016 is: Beg. 2016 Cumulative T/D Temporary Differences Beg. 2016 Deferred taxes End 2016 Cumulative T/D Current Year Change End 2016 Deferred Taxes PP&E, net When Maverick filed the company's 2016 tax return in August of 2017, the return reflected (actual) tax depreciation expense of $130,000 rather than the estimated) tax depreciation expense of $165,000 that was incorporated in the tax provision Corrected information for 2016: 12/31/2015 12/31/2016 PP&E - book basis PP&F - tax basis $700,000 520,000 $580,000 355,000 390,000 If the information from the 2017 tax return had been known at the time the 2016 tax provision was prepared, the temporary differences scheduling template would have been: End 2016 Cumulative Beg. 2016 Cumulative T/D Beg. 2016 Deferred taxes Temporary Differences End 2016 Deferred Taxes Current Year Change T/D PP&E, net Maverick reported $200,000 pretax book income on its 2016 income statement and the 2016 tax return reported $190.000 of taxable income. Compare the amounts recorded for the vear ended December 31, 2016 under the provision and on the tax return: Per Provision Per Return Difference Pretax book income PP&E temporary difference Taxable income Example 2: Return-to-provision adjustments for temporary differences (continued The journal entries recorded for the 2016 tax provision (using the information known at the time of the provision) versus what would have been recorded for the 2016 tax provision if the amounts from the 2016 tax return had been known when the provision was prepared are: Actual provision Provision if tax return information known Notice that the amount of total tax expense recorded under the two scenarios is the same: However, the current liability and deferred tax liability are not correct. An adjusting journal entry is needed to account for the consequences of the return-to-provision adjustment. This entry is recorded during the 2017 audit to adjust the liabilities for current and deferred taxes to the amounts that should have been recorded if the information on the tax return had been available at the time of the provision. Example 2: Return-to-provision adjustments for temporary differences Maverick Corporation reported the following information at the end of 2016. This informati was used to prepare the company's income tax provision during the 2016 audit. subject to a 35% statutory tax rate. 12/31/2015 12/31/2016 PP&E, net - book basis PP&E, net-tax basis $700.000 520,000 $580,000 355.000 The temporary differences template for 2016 is: Beg. 2016 Cumulative T/D Temporary Differences Beg. 2016 Deferred taxes End 2016 Cumulative T/D Current Year Change End 2016 Deferred Taxes PP&E, net When Maverick filed the company's 2016 tax return in August of 2017, the return reflected (actual) tax depreciation expense of $130,000 rather than the estimated) tax depreciation expense of $165,000 that was incorporated in the tax provision Corrected information for 2016: 12/31/2015 12/31/2016 PP&E - book basis PP&F - tax basis $700,000 520,000 $580,000 355,000 390,000 If the information from the 2017 tax return had been known at the time the 2016 tax provision was prepared, the temporary differences scheduling template would have been: End 2016 Cumulative Beg. 2016 Cumulative T/D Beg. 2016 Deferred taxes Temporary Differences End 2016 Deferred Taxes Current Year Change T/D PP&E, net Maverick reported $200,000 pretax book income on its 2016 income statement and the 2016 tax return reported $190.000 of taxable income. Compare the amounts recorded for the vear ended December 31, 2016 under the provision and on the tax return: Per Provision Per Return Difference Pretax book income PP&E temporary difference Taxable income Example 2: Return-to-provision adjustments for temporary differences (continued The journal entries recorded for the 2016 tax provision (using the information known at the time of the provision) versus what would have been recorded for the 2016 tax provision if the amounts from the 2016 tax return had been known when the provision was prepared are: Actual provision Provision if tax return information known Notice that the amount of total tax expense recorded under the two scenarios is the same: However, the current liability and deferred tax liability are not correct. An adjusting journal entry is needed to account for the consequences of the return-to-provision adjustment. This entry is recorded during the 2017 audit to adjust the liabilities for current and deferred taxes to the amounts that should have been recorded if the information on the tax return had been available at the time of the provisionStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting And Finance An Introduction

Authors: Eddie McLaney, Peter Atrill

10th Edition

1292312262, 978-1292312262