Answered step by step

Verified Expert Solution

Question

1 Approved Answer

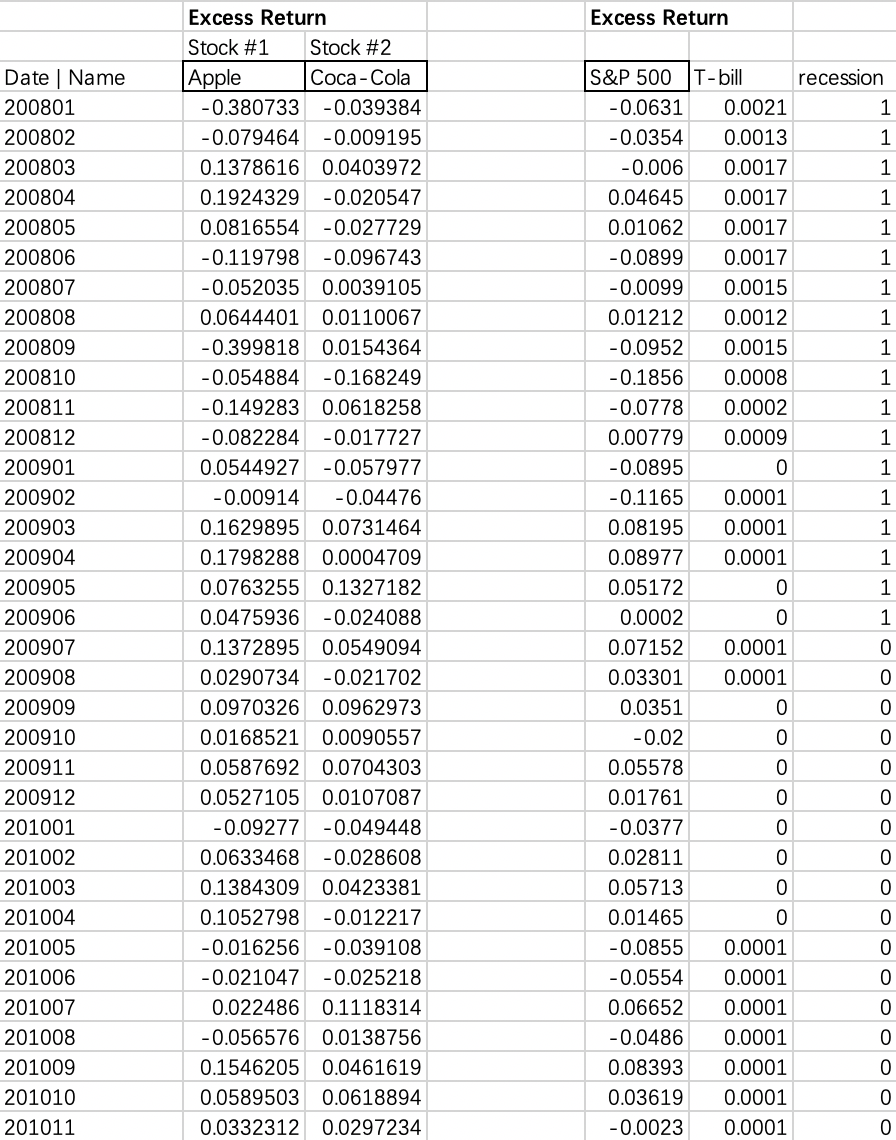

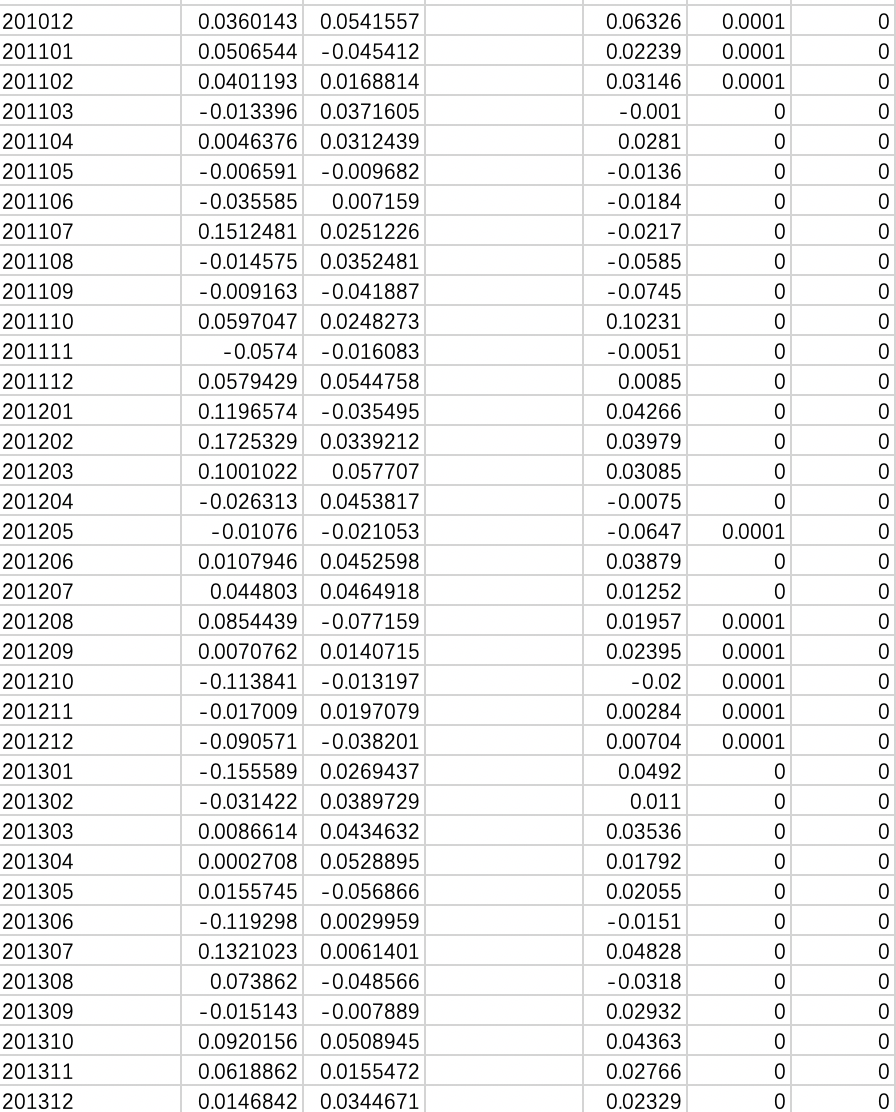

please show the formula, I don't know how to do it. Excess Return Date Name 200801 200802 200803 200804 200805 200806 200807 200808 200809 200810

please show the formula, I don't know how to do it.

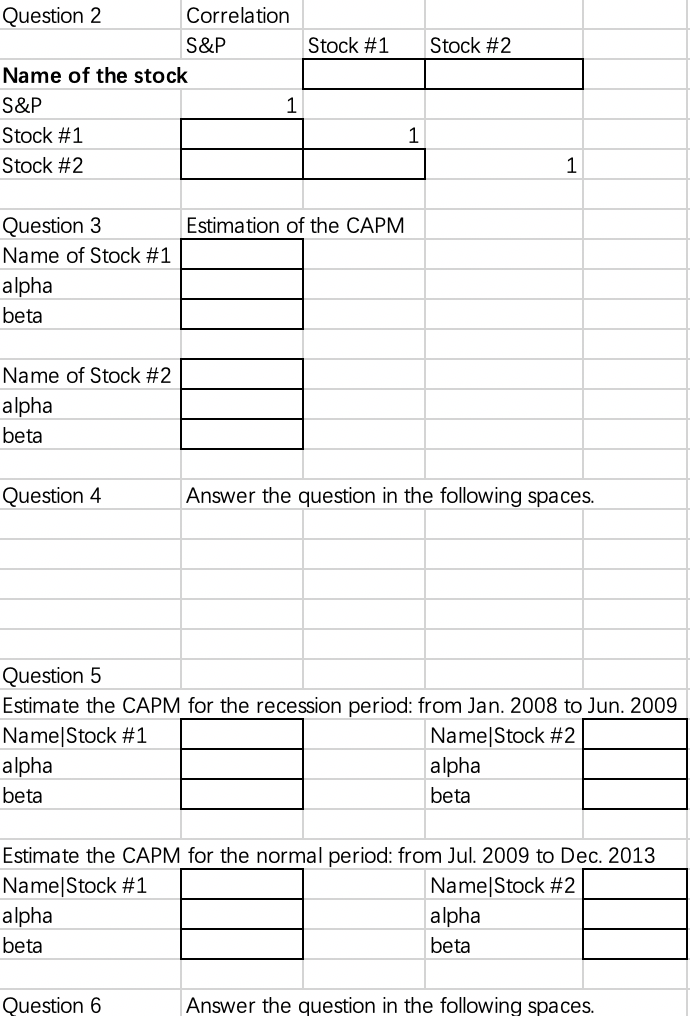

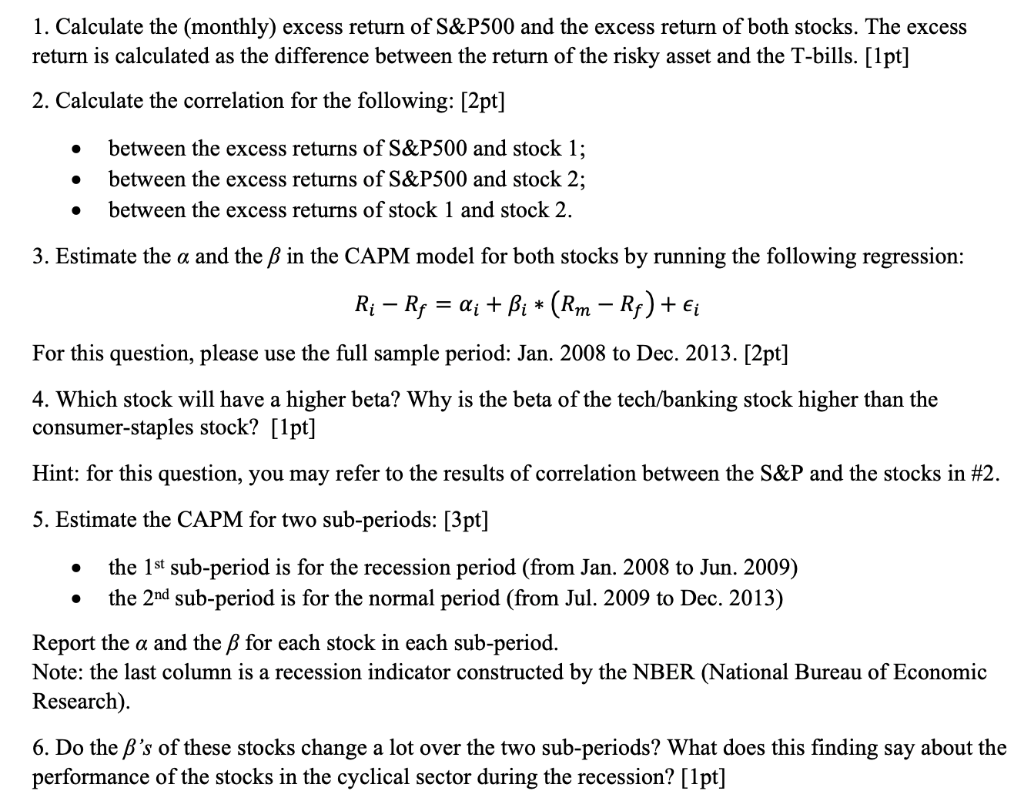

Excess Return Date Name 200801 200802 200803 200804 200805 200806 200807 200808 200809 200810 200811 200812 200901 200902 200903 200904 200905 200906 200907 200908 200909 200910 200911 200912 201001 201002 201003 201004 201005 201006 201007 201008 201009 201010 201011 Excess Return Stock #1 Stock #2 Apple Coca-Cola -0.380733 -0.039384 -0.079464 -0.009195 0.1378616 0.0403972 0.1924329 -0.020547 0.0816554 -0.027729 -0.119798 -0.096743 -0.052035 0.0039105 0.0644401 0.0110067 -0.399818 0.0154364 -0.054884 -0.168249 -0.149283 0.0618258 -0.082284 -0.017727 0.0544927 -0.057977 -0.00914 -0.04476 0.1629895 0.0731464 0.1798288 0.0004709 0.0763255 0.1327182 0.0475936 -0.024088 0.1372895 0.0549094 0.0290734 -0.021702 0.0970326 0.0962973 0.0168521 0.0090557 0.0587692 0.0704303 0.0527105 0.0107087 -0.09277 -0.049448 0.0633468 -0.028608 0.1384309 0.0423381 0.1052798 -0.012217 -0.016256 -0.039108 -0.021047 -0.025218 0.022486 0.1118314 -0.056576 0.0138756 0.1546205 0.0461619 0.0589503 0.0618894 0.0332312 0.0297234 S&P 500 T-bill recession -0.0631 0.0021 1 -0.0354 0.0013 1 -0.006 0.0017 1 0.04645 0.0017 1 0.01062 0.0017 1 -0.0899 0.0017 1 -0.0099 0.0015 1 0.01212 0.0012 1 -0.0952 0.0015 -0.1856 0.0008 -0.0778 0.0002 0.00779 0.0009 -0.0895 0 -0.1165 0.0001 1 0.08195 0.0001 0.08977 0.0001 0.05172 0 0.0002 0 1 0.07152 0.0001 0.03301 0.0001 0.0351 0 -0.02 0 0.05578 0 0.01761 0 -0.0377 0 0.02811 0 0.05713 0 0.01465 0 -0.0855 0.0001 -0.0554 0.0001 0.06652 0.0001 -0.0486 0.0001 0.08393 0.0001 0.03619 0.0001 -0.0023 0.0001 O O O O O O O O O O O O O O O O O O O O O O O O O O O O O O OOPPPPPPPPPPE 0.0001 0.0001 0.0001 0 0 0 0 0 0 0 0 0 0.0001 201012 201101 201102 201103 201104 201105 201106 201107 201108 201109 201110 201111 201112 201201 201202 201203 201204 201205 201206 201207 201208 201209 201210 201211 201212 201301 201302 201303 201304 201305 201306 201307 201308 201309 201310 201311 201312 0.0360143 0.0541557 0.0506544 -0.045412 0.0401193 0.0168814 -0.013396 0.0371605 0.0046376 0.0312439 -0.006591 -0.009682 -0.035585 0.007159 0.1512481 0.0251226 -0.014575 0.0352481 -0.009163 -0.041887 0.0597047 0.0248273 -0.0574 -0.016083 0.0579429 0.0544758 0.1196574 -0.035495 0.1725329 0.0339212 0.1001022 0.057707 -0.026313 0.0453817 -0.01076 -0.021053 0.0107946 0.0452598 0.044803 0.0464918 0.0854439 -0.077159 0.0070762 0.0140715 -0.113841 -0.013197 -0.017009 0.0197079 -0.090571 -0.038201 -0.155589 0.0269437 -0.031422 0.0389729 0.0086614 0.0434632 0.0002708 0.0528895 0.0155745 -0.056866 -0.119298 0.0029959 0.1321023 0.0061401 0.073862 -0.048566 -0.015143 -0.007889 0.0920156 0.0508945 0.0618862 0.0155472 0.0146842 0.0344671 0.06326 0.02239 0.03146 -0.001 0.0281 -0.0136 -0.0184 -0.0217 -0.0585 -0.0745 0.10231 -0.0051 0.0085 0.04266 0.03979 0.03085 -0.0075 -0.0647 0.03879 0.01252 0.01957 0.02395 -0.02 0.00284 0.00704 0.0492 0.011 0.03536 0.01792 0.02055 -0.0151 0.04828 -0.0318 0.02932 0.04363 0.02766 0.02329 0.0001 0.0001 0.0001 0.0001 0.0001 0 0 0 0 0 0 0 Stock #1 Stock #2 Question 2 Correlation S&P Name of the stock S&P 1 Stock #1 Stock #2 1 1 Estimation of the CAPM Question 3 Name of Stock #1 alpha beta Name of Stock #2 alpha beta Question 4 Answer the question in the following spaces. Question 5 Estimate the CAPM for the recession period: from Jan. 2008 to Jun. 2009 Name|Stock #1 Name|Stock #2 alpha alpha beta beta Estimate the CAPM for the normal period: from Jul. 2009 to Dec. 2013 Name Stock #1 Name Stock #2 alpha alpha beta beta Question 6 Answer the question in the following spaces. 1. Calculate the (monthly) excess return of S&P500 and the excess return of both stocks. The excess return is calculated as the difference between the return of the risky asset and the T-bills. [1pt] 2. Calculate the correlation for the following: [2pt] . between the excess returns of S&P500 and stock 1; between the excess returns of S&P500 and stock 2; between the excess returns of stock 1 and stock 2. 3. Estimate the a and the in the CAPM model for both stocks by running the following regression: Ri Rs = di + Bi * (Rm Rp) + Ei + For this question, please use the full sample period: Jan. 2008 to Dec. 2013. [2pt] 4. Which stock will have a higher beta? Why is the beta of the tech/banking stock higher than the consumer-staples stock? [1pt] Hint: for this question, you may refer to the results of correlation between the S&P and the stocks in #2. 5. Estimate the CAPM for two sub-periods: [3pt] the 1st sub-period is for the recession period (from Jan. 2008 to Jun. 2009) the 2nd sub-period is for the normal period (from Jul. 2009 to Dec. 2013) Report the a and the B for each stock in each sub-period. Note: the last column is a recession indicator constructed by the NBER (National Bureau of Economic Research). 6. Do the B's of these stocks change a lot over the two sub-periods? What does this finding say about the performance of the stocks in the cyclical sector during the recession? [1pt] Excess Return Date Name 200801 200802 200803 200804 200805 200806 200807 200808 200809 200810 200811 200812 200901 200902 200903 200904 200905 200906 200907 200908 200909 200910 200911 200912 201001 201002 201003 201004 201005 201006 201007 201008 201009 201010 201011 Excess Return Stock #1 Stock #2 Apple Coca-Cola -0.380733 -0.039384 -0.079464 -0.009195 0.1378616 0.0403972 0.1924329 -0.020547 0.0816554 -0.027729 -0.119798 -0.096743 -0.052035 0.0039105 0.0644401 0.0110067 -0.399818 0.0154364 -0.054884 -0.168249 -0.149283 0.0618258 -0.082284 -0.017727 0.0544927 -0.057977 -0.00914 -0.04476 0.1629895 0.0731464 0.1798288 0.0004709 0.0763255 0.1327182 0.0475936 -0.024088 0.1372895 0.0549094 0.0290734 -0.021702 0.0970326 0.0962973 0.0168521 0.0090557 0.0587692 0.0704303 0.0527105 0.0107087 -0.09277 -0.049448 0.0633468 -0.028608 0.1384309 0.0423381 0.1052798 -0.012217 -0.016256 -0.039108 -0.021047 -0.025218 0.022486 0.1118314 -0.056576 0.0138756 0.1546205 0.0461619 0.0589503 0.0618894 0.0332312 0.0297234 S&P 500 T-bill recession -0.0631 0.0021 1 -0.0354 0.0013 1 -0.006 0.0017 1 0.04645 0.0017 1 0.01062 0.0017 1 -0.0899 0.0017 1 -0.0099 0.0015 1 0.01212 0.0012 1 -0.0952 0.0015 -0.1856 0.0008 -0.0778 0.0002 0.00779 0.0009 -0.0895 0 -0.1165 0.0001 1 0.08195 0.0001 0.08977 0.0001 0.05172 0 0.0002 0 1 0.07152 0.0001 0.03301 0.0001 0.0351 0 -0.02 0 0.05578 0 0.01761 0 -0.0377 0 0.02811 0 0.05713 0 0.01465 0 -0.0855 0.0001 -0.0554 0.0001 0.06652 0.0001 -0.0486 0.0001 0.08393 0.0001 0.03619 0.0001 -0.0023 0.0001 O O O O O O O O O O O O O O O O O O O O O O O O O O O O O O OOPPPPPPPPPPE 0.0001 0.0001 0.0001 0 0 0 0 0 0 0 0 0 0.0001 201012 201101 201102 201103 201104 201105 201106 201107 201108 201109 201110 201111 201112 201201 201202 201203 201204 201205 201206 201207 201208 201209 201210 201211 201212 201301 201302 201303 201304 201305 201306 201307 201308 201309 201310 201311 201312 0.0360143 0.0541557 0.0506544 -0.045412 0.0401193 0.0168814 -0.013396 0.0371605 0.0046376 0.0312439 -0.006591 -0.009682 -0.035585 0.007159 0.1512481 0.0251226 -0.014575 0.0352481 -0.009163 -0.041887 0.0597047 0.0248273 -0.0574 -0.016083 0.0579429 0.0544758 0.1196574 -0.035495 0.1725329 0.0339212 0.1001022 0.057707 -0.026313 0.0453817 -0.01076 -0.021053 0.0107946 0.0452598 0.044803 0.0464918 0.0854439 -0.077159 0.0070762 0.0140715 -0.113841 -0.013197 -0.017009 0.0197079 -0.090571 -0.038201 -0.155589 0.0269437 -0.031422 0.0389729 0.0086614 0.0434632 0.0002708 0.0528895 0.0155745 -0.056866 -0.119298 0.0029959 0.1321023 0.0061401 0.073862 -0.048566 -0.015143 -0.007889 0.0920156 0.0508945 0.0618862 0.0155472 0.0146842 0.0344671 0.06326 0.02239 0.03146 -0.001 0.0281 -0.0136 -0.0184 -0.0217 -0.0585 -0.0745 0.10231 -0.0051 0.0085 0.04266 0.03979 0.03085 -0.0075 -0.0647 0.03879 0.01252 0.01957 0.02395 -0.02 0.00284 0.00704 0.0492 0.011 0.03536 0.01792 0.02055 -0.0151 0.04828 -0.0318 0.02932 0.04363 0.02766 0.02329 0.0001 0.0001 0.0001 0.0001 0.0001 0 0 0 0 0 0 0 Stock #1 Stock #2 Question 2 Correlation S&P Name of the stock S&P 1 Stock #1 Stock #2 1 1 Estimation of the CAPM Question 3 Name of Stock #1 alpha beta Name of Stock #2 alpha beta Question 4 Answer the question in the following spaces. Question 5 Estimate the CAPM for the recession period: from Jan. 2008 to Jun. 2009 Name|Stock #1 Name|Stock #2 alpha alpha beta beta Estimate the CAPM for the normal period: from Jul. 2009 to Dec. 2013 Name Stock #1 Name Stock #2 alpha alpha beta beta Question 6 Answer the question in the following spaces. 1. Calculate the (monthly) excess return of S&P500 and the excess return of both stocks. The excess return is calculated as the difference between the return of the risky asset and the T-bills. [1pt] 2. Calculate the correlation for the following: [2pt] . between the excess returns of S&P500 and stock 1; between the excess returns of S&P500 and stock 2; between the excess returns of stock 1 and stock 2. 3. Estimate the a and the in the CAPM model for both stocks by running the following regression: Ri Rs = di + Bi * (Rm Rp) + Ei + For this question, please use the full sample period: Jan. 2008 to Dec. 2013. [2pt] 4. Which stock will have a higher beta? Why is the beta of the tech/banking stock higher than the consumer-staples stock? [1pt] Hint: for this question, you may refer to the results of correlation between the S&P and the stocks in #2. 5. Estimate the CAPM for two sub-periods: [3pt] the 1st sub-period is for the recession period (from Jan. 2008 to Jun. 2009) the 2nd sub-period is for the normal period (from Jul. 2009 to Dec. 2013) Report the a and the B for each stock in each sub-period. Note: the last column is a recession indicator constructed by the NBER (National Bureau of Economic Research). 6. Do the B's of these stocks change a lot over the two sub-periods? What does this finding say about the performance of the stocks in the cyclical sector during the recession? [1pt]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Financial Institutions Management

Authors: Marcia Cornett, Anthony Saunders

1st Edition

0256253676, 9780256253672