Answered step by step

Verified Expert Solution

Question

1 Approved Answer

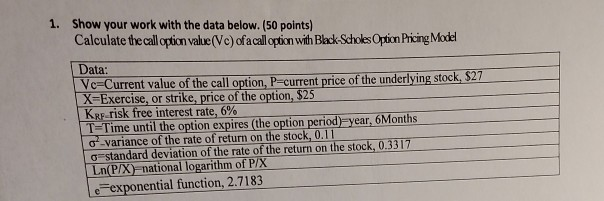

please show work 1. Show your work with the data below. (50 points) Calculate the call option value(Ve) of a call option with Black-Schokes Option

please show work

1. Show your work with the data below. (50 points) Calculate the call option value(Ve) of a call option with Black-Schokes Option Pricing Model Data: Vc Current value of the call option, P-current price of the underlying stock, $27 X-Exercise, or strike, price of the option, $25 KRF risk free interest rate, 6 % T-Time until the option expires (the option period) year, 6Months a-variance of the rate of return on the stock, 0.11 a standard deviation of the rate of the return on the stock, 0.3317 Ln(P/X)=national logarithm of P/X exponential function, 2.7183Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analysis For Financial Management

Authors: Robert Higgins

6th Edition

0071181172, 9780071181174