Answered step by step

Verified Expert Solution

Question

1 Approved Answer

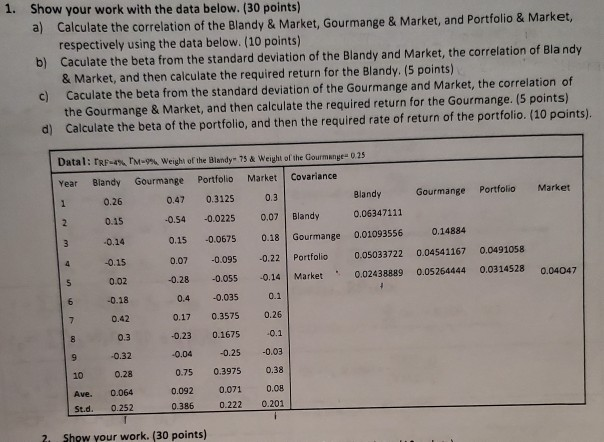

please show work 1. Show your work with the data below. (30 points) a) Calculate the correlation of the Blandy & Market, Gourmange & Market,

please show work

1. Show your work with the data below. (30 points) a) Calculate the correlation of the Blandy & Market, Gourmange & Market, and Portfolio & Market, respectively using the data below. (10 points) b) Caculate the beta from the standard deviation of the Blandy and Market, the correlation of Bla ndy & Market, and then calculate the required return for the Blandy. (5 points) Caculate the beta from the standard deviation of the Gourmange and Market, the correlation of the Gourmange & Market, and then calculate the required return for the Gourmange. (5 points) d) Calculate the beta of the portfolio, and then the required rate of return of the portfolio. (10 points). Datal: rRF-4 % TM - 9% Weight of the Blandy 75 & Weight of the Gourmange 0.25 Market Covariance Blandy Gourmange Portfolio Year Portfolio Gourmange Market Blandy 0.26 0.47 0.3125 0.3 0.06347111 0.15 -0.54 -0.0225 0.07 Blandy 2 0.14884 Gourmange 0.01093556 0.14 0.18 3 0.15 -0.0675 0.0491058 0.04541167 0.05033722 -0.15 Portfolio 0.07 -0.095 -0.22 0.0314528 0.02438889 0.05264444 0.02 -0.28 -0.055 -0.14 Market 0.04047 -0.18 0.4 -0.035 0.1 0.26 0.42 0.17 0.3575 7 -0.23 0.1675 -0.1 0.3 8 -0.04 -0.25 -0.03 -0.32 9 0.38 0.75 0.3975 10 0.28 0.064 0.092 0.071 0.08 Ave. 0.252 0.386 0.222 0.201 St.d. work. (30 points) owStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started