PLEASE SHOW WORK

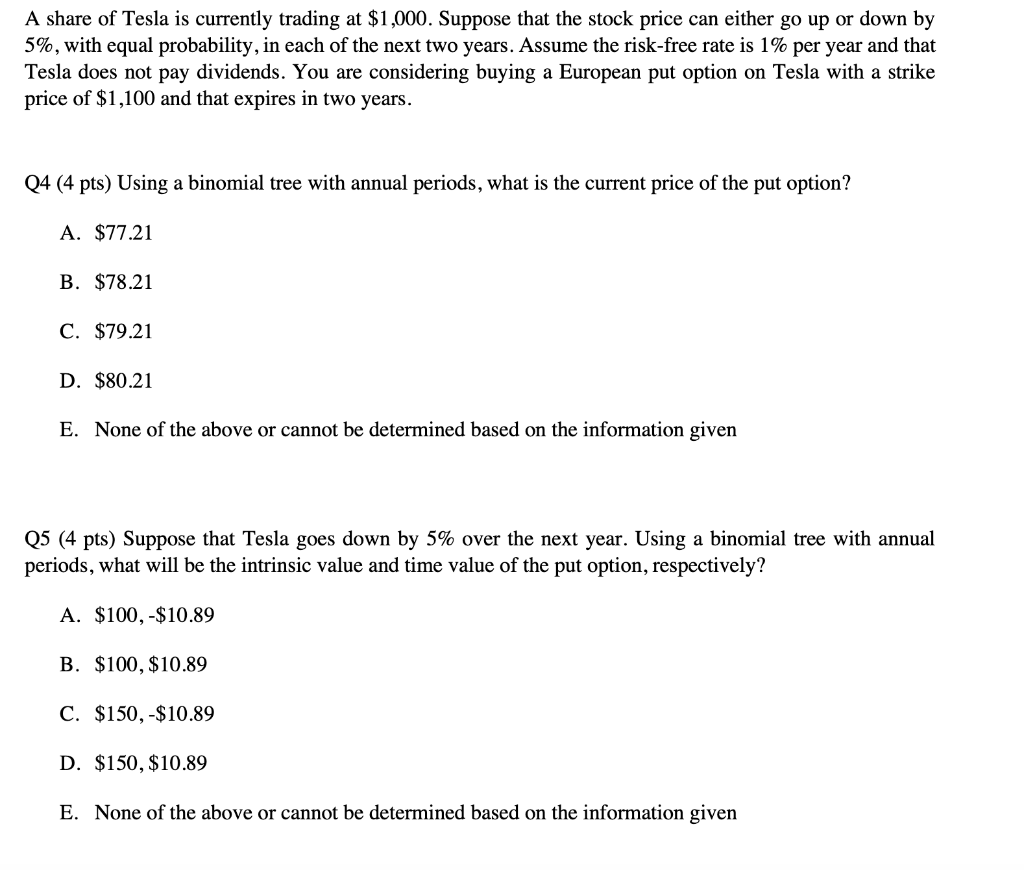

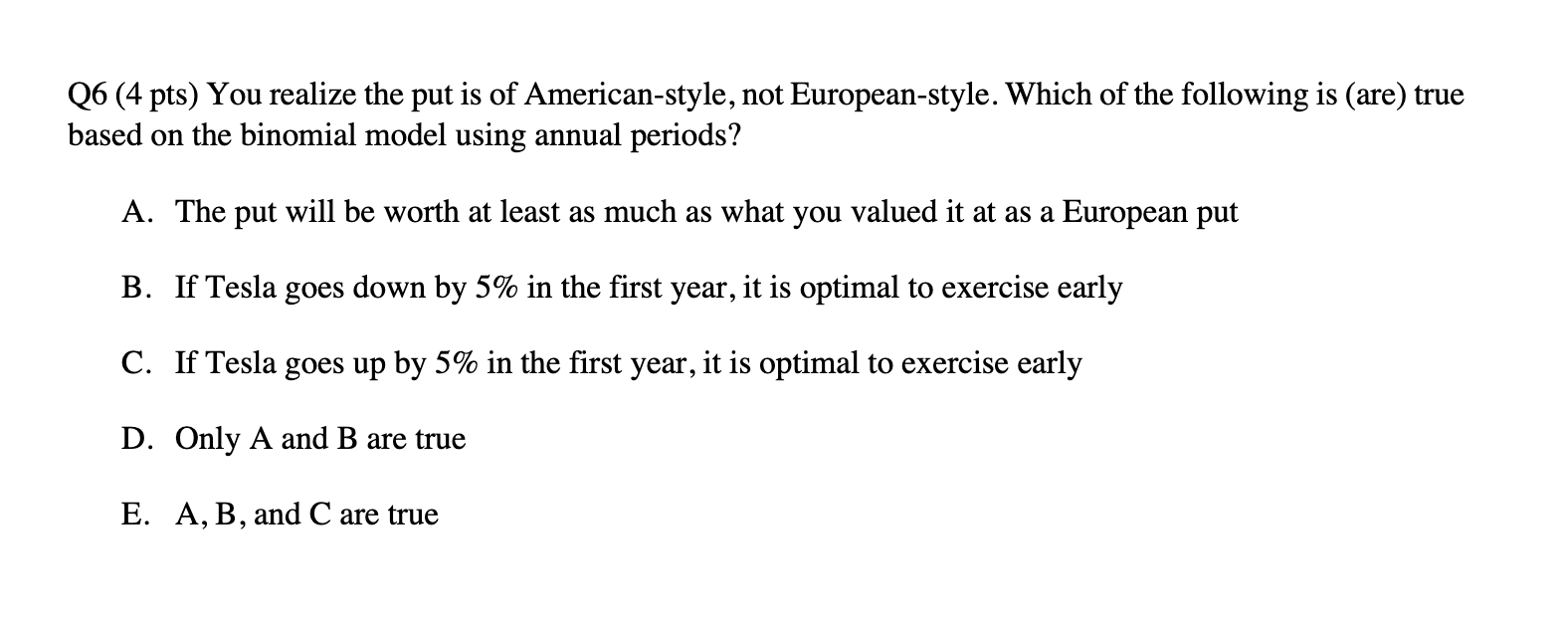

A share of Tesla is currently trading at $1,000. Suppose that the stock price can either go up or down by 5%, with equal probability, in each of the next two years. Assume the risk-free rate is 1% per year and that Tesla does not pay dividends. You are considering buying a European put option on Tesla with a strike price of $1,100 and that expires in two years. Q4 (4 pts) Using a binomial tree with annual periods, what is the current price of the put option? A. $77.21 B. $78.21 C. $79.21 D. $80.21 E. None of the above or cannot be determined based on the information given Q5 (4 pts) Suppose that Tesla goes down by 5% over the next year. Using a binomial tree with annual periods, what will be the intrinsic value and time value of the put option, respectively? A. $100,$10.89 B. $100,$10.89 C. $150,$10.89 D. $150,$10.89 E. None of the above or cannot be determined based on the information given Q6 (4 pts) You realize the put is of American-style, not European-style. Which of the following is (are) true based on the binomial model using annual periods? A. The put will be worth at least as much as what you valued it at as a European put B. If Tesla goes down by 5% in the first year, it is optimal to exercise early C. If Tesla goes up by 5% in the first year, it is optimal to exercise early D. Only A and B are true E. A,B, and C are true A share of Tesla is currently trading at $1,000. Suppose that the stock price can either go up or down by 5%, with equal probability, in each of the next two years. Assume the risk-free rate is 1% per year and that Tesla does not pay dividends. You are considering buying a European put option on Tesla with a strike price of $1,100 and that expires in two years. Q4 (4 pts) Using a binomial tree with annual periods, what is the current price of the put option? A. $77.21 B. $78.21 C. $79.21 D. $80.21 E. None of the above or cannot be determined based on the information given Q5 (4 pts) Suppose that Tesla goes down by 5% over the next year. Using a binomial tree with annual periods, what will be the intrinsic value and time value of the put option, respectively? A. $100,$10.89 B. $100,$10.89 C. $150,$10.89 D. $150,$10.89 E. None of the above or cannot be determined based on the information given Q6 (4 pts) You realize the put is of American-style, not European-style. Which of the following is (are) true based on the binomial model using annual periods? A. The put will be worth at least as much as what you valued it at as a European put B. If Tesla goes down by 5% in the first year, it is optimal to exercise early C. If Tesla goes up by 5% in the first year, it is optimal to exercise early D. Only A and B are true E. A,B, and C are true