Answered step by step

Verified Expert Solution

Question

1 Approved Answer

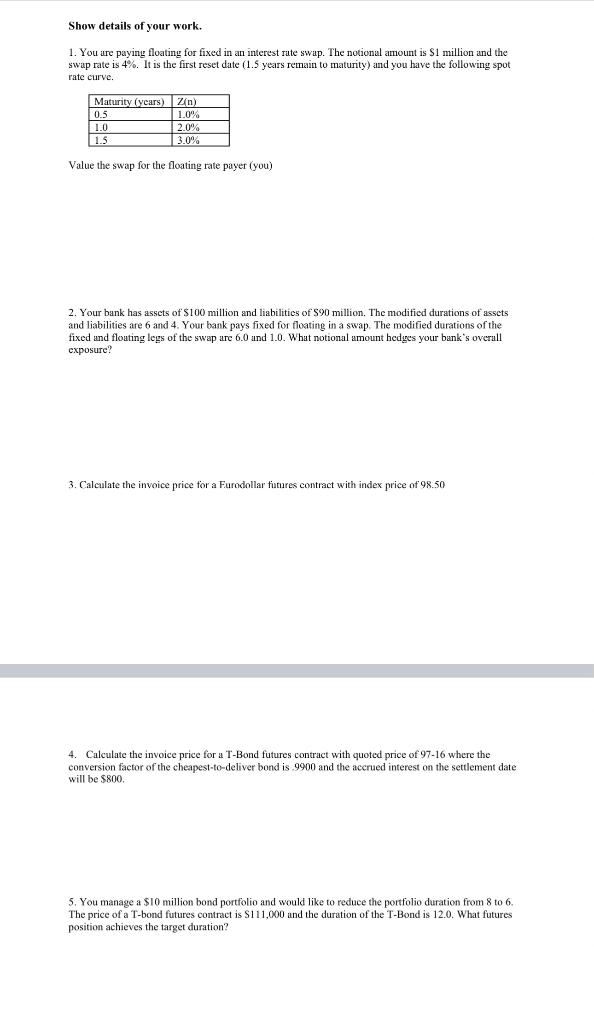

Please show work and answer correctly THANK YOU!!! Show details of your work. 1. You are paying floating for fixed in an interest rate swap.

Please show work and answer correctly THANK YOU!!!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Regulation A+ How The JOBS Act Creates Opportunities For Entrepreneurs And Investors

Authors: Paul Getty , Dinesh Gupta , Robert R. Kaplan

1st Edition

1430257318,1430257326