Answered step by step

Verified Expert Solution

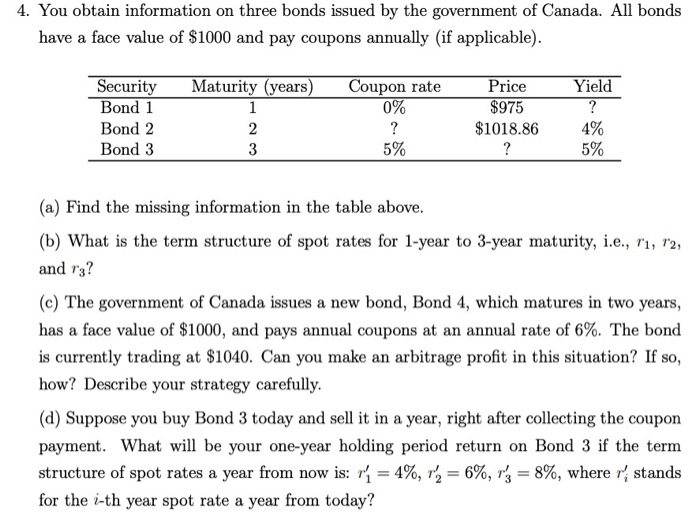

Question

1 Approved Answer

Please show work, and do not copy from previous answers from other experts (which are partially wrong) since I posted this question 2 times already.

Please show work, and do not copy from previous answers from other experts (which are partially wrong) since I posted this question 2 times already. Thanks!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dynamic Asset Allocation With Forwards And Futures

Authors: Abraham Lioui , Patrice Poncet

1st Edition

0387241078,038724106X