please show working out , if needed

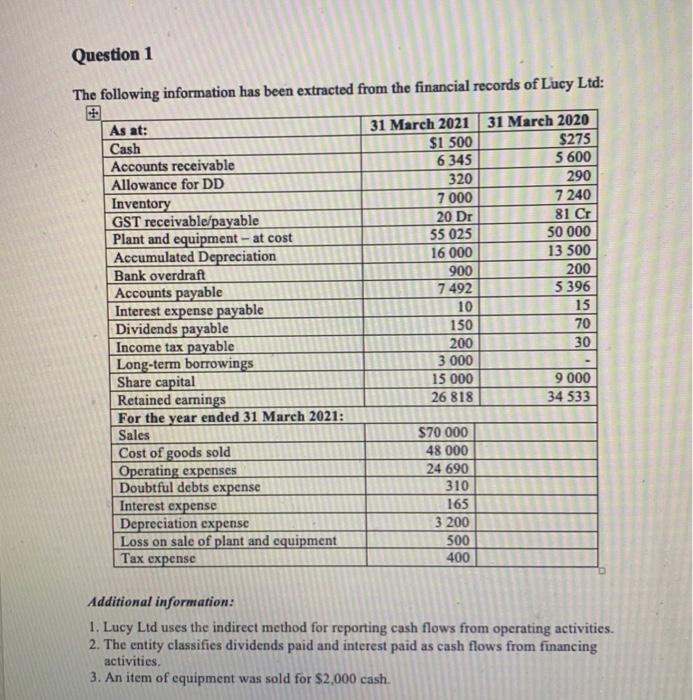

Question 1 The following information has been extracted from the financial records of Lucy Ltd: As at: Cash Accounts receivable Allowance for DD Inventory GST receivable/payable Plant and equipment - at cost Accumulated Depreciation Bank overdraft Accounts payable Interest expense payable Dividends payable Income tax payable Long-term borrowings Share capital Retained earnings For the year ended 31 March 2021: Sales Cost of goods sold Operating expenses Doubtful debts expense Interest expense Depreciation expense Loss on sale of plant and equipment Tax expense 31 March 2021 31 March 2020 $1 500 $275 6 345 5 600 320 290 7 000 7 240 20 Dr 81 Cr 55 025 50 000 16 000 13 500 900 200 7492 5 396 10 15 150 70 200 30 3 000 15 000 9 000 26 818 34 533 $70 000 48 000 24 690 310 165 3 200 500 400 Additional information: 1. Lucy Ltd uses the indirect method for reporting cash flows from operating activities. 2. The entity classifies dividends paid and interest paid as cash flows from financing activities. 3. An item of equipment was sold for $2,000 cash. Question 1 (L) Statement of Cash Flows for Lucy Lid for the year ended 31 March 2021 Cash Bows from operating activities: Non-cash items: Deferrals Accruals: Items included in the determination of PBT classified as investing financing activities Items included in the determination of PBT classified separately as operating activities! S Cash generated from operations Net cashed from operating activities Cash flows from investing activities Nel cas de investing actitles Question 1 (ii) Statement of Cash Flows for Lucy Ltd for the year ended 31 March 2021 continued: Cash flows from financing activities: Net cash from used in financing activities Net increase/(decrease) in cash and cash equivalents Cash and cash equivalents at the beginning of period Cash and cash equivalents at the end of period Question 1 (ll) Statement of Cash Flows for Lucy Ltd for the year ended 31 March 2021 Cash flows from operating activities S Cash generated from operations $ Net cash (used in from operating activities Cash flows from investing activities: Nel cash from used in) Investing activities Cash flows from financing activities: + Nel cash from cused in financing activities Net Increase/(decrease) in cash and cash equivalents Cash and cash equivalents at the beginning of period Cash and eash equivalents at the end of period Question 1 (10) Reconciliation of profit after tax to net cash flow (wed in froen operating activities Profit/(loss) after tax Non-cash items: Deferrals/Accruals: Reverse Items of income/expense classified as CFIA/CFFA: Net cash flows (used in from operating activities Question 1 (lv) Review the SCF's and state three significant concerns. Briefly explain your concerns: 1. Why is this a concern? 2. Why is this a concern! 3. Why is this a concer? I Question 3 In Question 1, Lucy Ltd classified interest expense paid, and dividends paid as cash flows from financing activities. What if Lucy Ltd had used the alternative classification for these two items? Complete the table in the answer booklet to illustrate the effect of using a different classification, for these two items, on the Statement of Cash Flows and note. Ensure you provide detail of the parts of the CFOA (and Reconciliation) affected. For example: 'After the cash generated from operations' line. Question 3 Insert your answers from Question 1: Your alternative classification answer: (i) The indirect method was used: (6) The Indirect method was used: $ CFOA $ CFOA CFIA CFIA CFFA CFFA (ii) The direct method was used: (iii) The direct method was used: CFOA CFOA CFIA CFIA CFFA CFFA and Reconciliation: and Reconciliation: Question 1 The following information has been extracted from the financial records of Lucy Ltd: As at: Cash Accounts receivable Allowance for DD Inventory GST receivable/payable Plant and equipment - at cost Accumulated Depreciation Bank overdraft Accounts payable Interest expense payable Dividends payable Income tax payable Long-term borrowings Share capital Retained earnings For the year ended 31 March 2021: Sales Cost of goods sold Operating expenses Doubtful debts expense Interest expense Depreciation expense Loss on sale of plant and equipment Tax expense 31 March 2021 31 March 2020 $1 500 $275 6 345 5 600 320 290 7 000 7 240 20 Dr 81 Cr 55 025 50 000 16 000 13 500 900 200 7492 5 396 10 15 150 70 200 30 3 000 15 000 9 000 26 818 34 533 $70 000 48 000 24 690 310 165 3 200 500 400 Additional information: 1. Lucy Ltd uses the indirect method for reporting cash flows from operating activities. 2. The entity classifies dividends paid and interest paid as cash flows from financing activities. 3. An item of equipment was sold for $2,000 cash. Question 1 (L) Statement of Cash Flows for Lucy Lid for the year ended 31 March 2021 Cash Bows from operating activities: Non-cash items: Deferrals Accruals: Items included in the determination of PBT classified as investing financing activities Items included in the determination of PBT classified separately as operating activities! S Cash generated from operations Net cashed from operating activities Cash flows from investing activities Nel cas de investing actitles Question 1 (ii) Statement of Cash Flows for Lucy Ltd for the year ended 31 March 2021 continued: Cash flows from financing activities: Net cash from used in financing activities Net increase/(decrease) in cash and cash equivalents Cash and cash equivalents at the beginning of period Cash and cash equivalents at the end of period Question 1 (ll) Statement of Cash Flows for Lucy Ltd for the year ended 31 March 2021 Cash flows from operating activities S Cash generated from operations $ Net cash (used in from operating activities Cash flows from investing activities: Nel cash from used in) Investing activities Cash flows from financing activities: + Nel cash from cused in financing activities Net Increase/(decrease) in cash and cash equivalents Cash and cash equivalents at the beginning of period Cash and eash equivalents at the end of period Question 1 (10) Reconciliation of profit after tax to net cash flow (wed in froen operating activities Profit/(loss) after tax Non-cash items: Deferrals/Accruals: Reverse Items of income/expense classified as CFIA/CFFA: Net cash flows (used in from operating activities Question 1 (lv) Review the SCF's and state three significant concerns. Briefly explain your concerns: 1. Why is this a concern? 2. Why is this a concern! 3. Why is this a concer? I Question 3 In Question 1, Lucy Ltd classified interest expense paid, and dividends paid as cash flows from financing activities. What if Lucy Ltd had used the alternative classification for these two items? Complete the table in the answer booklet to illustrate the effect of using a different classification, for these two items, on the Statement of Cash Flows and note. Ensure you provide detail of the parts of the CFOA (and Reconciliation) affected. For example: 'After the cash generated from operations' line. Question 3 Insert your answers from Question 1: Your alternative classification answer: (i) The indirect method was used: (6) The Indirect method was used: $ CFOA $ CFOA CFIA CFIA CFFA CFFA (ii) The direct method was used: (iii) The direct method was used: CFOA CFOA CFIA CFIA CFFA CFFA and Reconciliation: and Reconciliation