Answered step by step

Verified Expert Solution

Question

1 Approved Answer

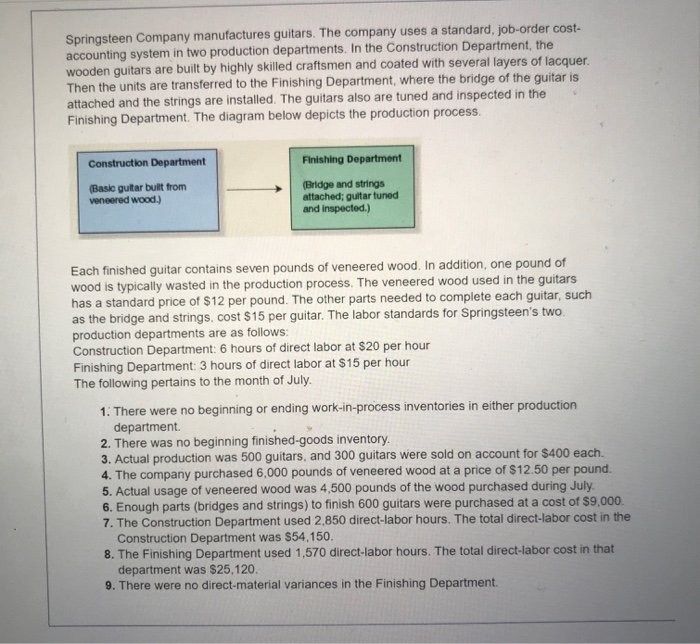

please show your work 2. (a) Construction Department DIRECT-MATERIAL PRICE AND QUANTITY VARIANCES Actual Material Cost Standard Material Cost Actual Standard Actual Actual Standard Standard

please show your work

please show your work Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fraud Auditing Using CAATT A Manual For Auditors And Forensic Accountants To Detect Organizational Fraud

Authors: Shaun Aghili

1st Edition

1032401559, 978-1032401553