Answered step by step

Verified Expert Solution

Question

1 Approved Answer

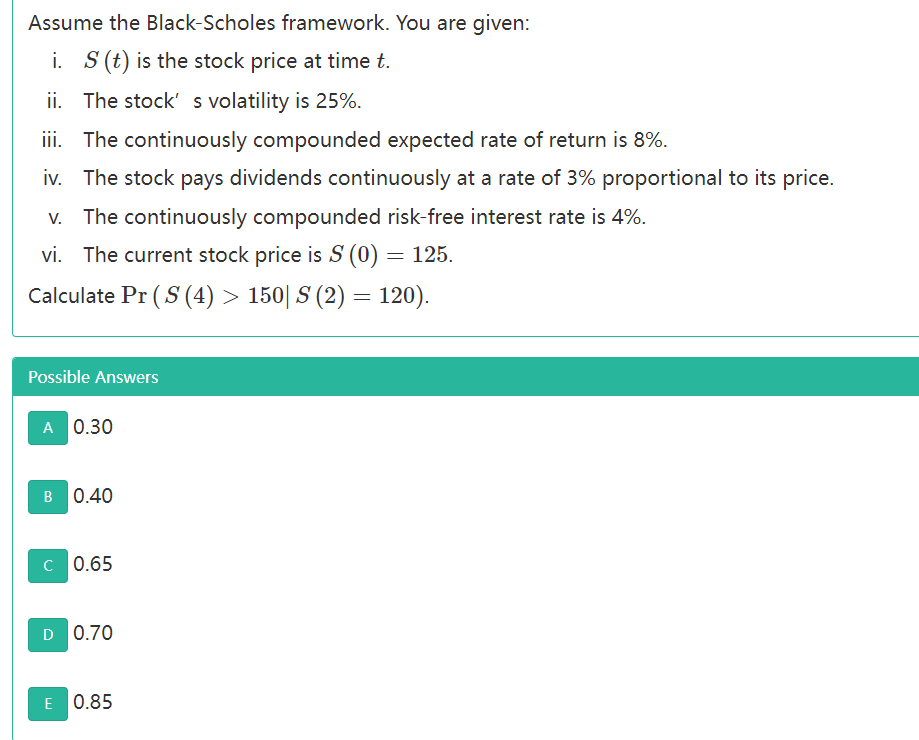

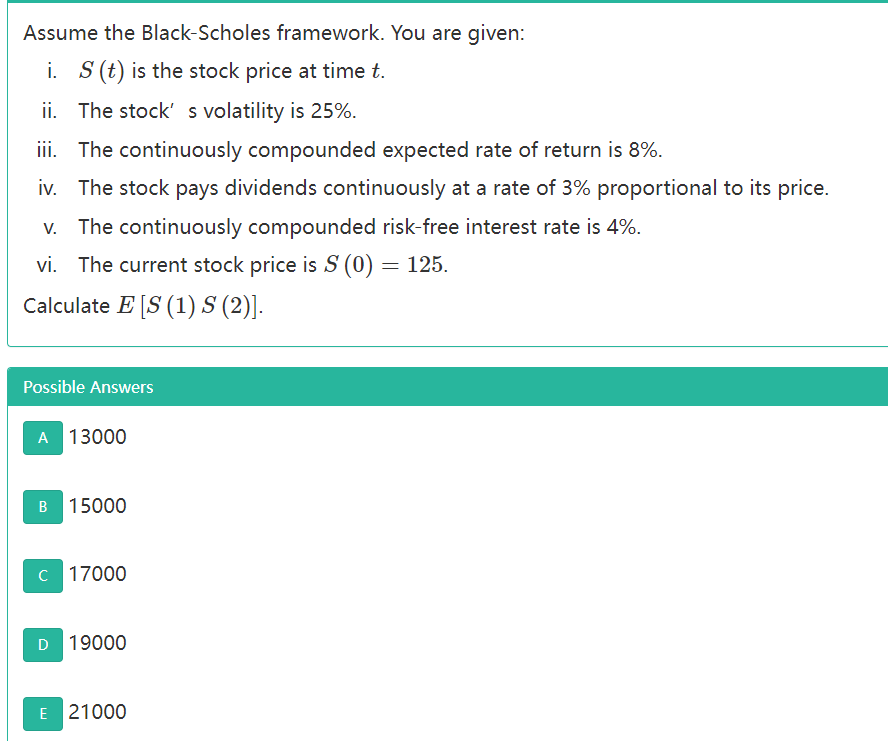

Please show your work Assume the Black-Scholes framework. You are given: i. S(t) is the stock price at time t. ii. The stock' s volatility

Please show your work

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Managerial Accounting Concepts

Authors: Thomas Edmonds, Christopher Edmonds, Bor Yi Tsay, Philip Old

7th edition

978-0077632427, 77632427, 78025656, 978-0078025655