Answered step by step

Verified Expert Solution

Question

1 Approved Answer

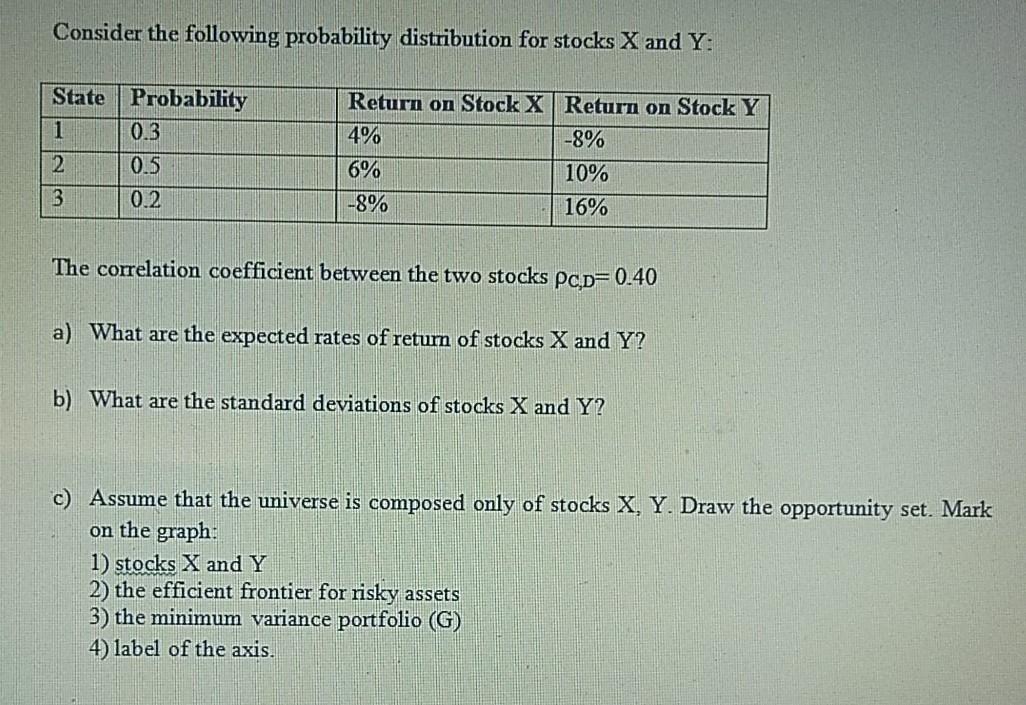

Please solve c branch only in the easiest way possible Consider the following probability distribution for stocks X and Y: Return on Stock X Return

Please solve c branch only in the easiest way possible

Consider the following probability distribution for stocks X and Y: Return on Stock X Return on Stock Y State Probability 1 0.3 2 0.5 4% -8% 6% 10% 3 0.2 -8% 16% The correlation coefficient between the two stocks pc,D=0.40 a) What are the expected rates of retum of stocks X and Y? b) What are the standard deviations of stocks X and Y? c) Assume that the universe is composed only of stocks X, Y. Draw the opportunity set. Mark on the graph: 1) stocks X and Y 2) the efficient frontier for risky assets 3) the minimum variance portfolio (G) 4) label of the axisStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Report Of Johnstown Flood Finance Committee

Authors: Johnstown (Pa.) Flood Finance Committee, YA Pamphlet Collection

1st Edition

1246561557, 9781246561555