Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please solve question 13.5 (13.1 is needed for this question) also, for 13.5 b, should the manager invest? Should the manager hesge the project's currency

Please solve question 13.5 (13.1 is needed for this question)

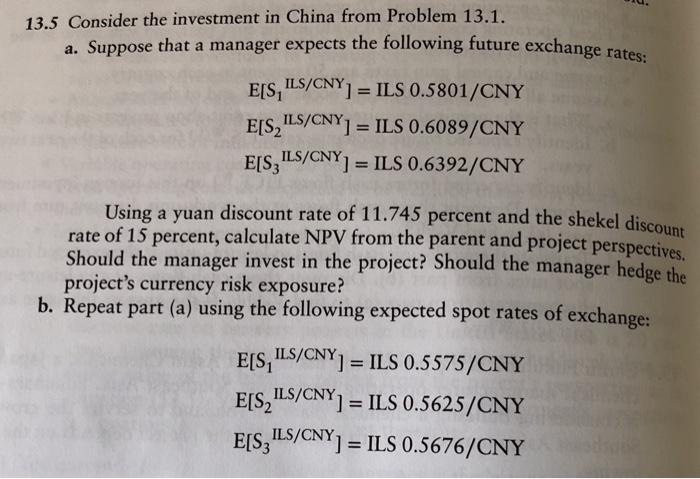

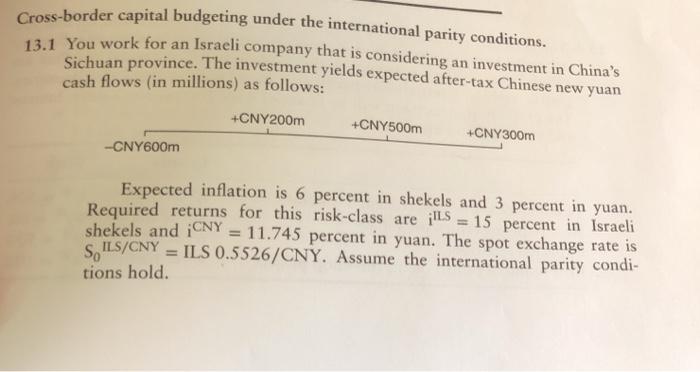

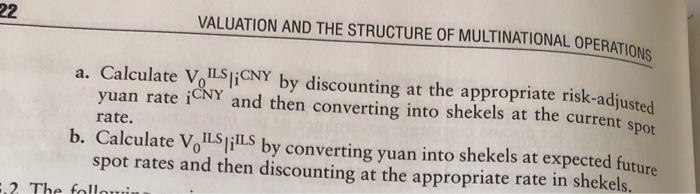

Using a yuan discount rate of 11.745 percent and the shekel discount 13.5 Consider the investment in China from Problem 13.1. a. Suppose that a manager expects the following future exchange rates: E[S, ILS/CNY) = ILS 0.5801/CNY E[S, TLS/CNY) = ILS 0.6089/CNY E[S, ILS/CNY) = ILS 0.6392/CNY rate of 15 percent, calculate NPV from the parent and project perspectives. Should the manager invest in the project? Should the manager hedge the project's currency risk exposure? b. Repeat part (a) using the following expected spot rates of exchange: E[S, ILS/CNY) = ILS 0.5575/CNY E[S, ILS/CNY) = ILS 0.5625/CNY E[S, ILS/CNY) = ILS 0.5676/CNY Cross-border capital budgeting under the international parity conditions. 13.1 You work for an Israeli company that is considering an investment in China's Sichuan province. The investment yields expected after-tax Chinese new yuan cash flows (in millions) as follows: +CNY 200m +CNY500m +CNY300m --CNY600m Expected inflation is 6 percent in shekels and 3 percent in yuan. Required returns for this risk-class are ILS = 15 percent in Israeli shekels and iCNY = 11.745 percent in yuan. The spot exchange rate is ILS 0.5526/CNY. Assume the international parity condi- tions hold. S, ILS/CNY 22 VALUATION AND THE STRUCTURE OF MULTINATIONAL OPERATIONS rate. a. Calculate V, SiCNY by discounting at the appropriate risk-adjusted yuan rate iCNY and then converting into shekels at the current spot b. Calculate V. SillS by converting yuan into shekels at expected future spot rates and then discounting at the appropriate rate in shekels. 4.2 The followin Using a yuan discount rate of 11.745 percent and the shekel discount 13.5 Consider the investment in China from Problem 13.1. a. Suppose that a manager expects the following future exchange rates: E[S, ILS/CNY) = ILS 0.5801/CNY E[S, TLS/CNY) = ILS 0.6089/CNY E[S, ILS/CNY) = ILS 0.6392/CNY rate of 15 percent, calculate NPV from the parent and project perspectives. Should the manager invest in the project? Should the manager hedge the project's currency risk exposure? b. Repeat part (a) using the following expected spot rates of exchange: E[S, ILS/CNY) = ILS 0.5575/CNY E[S, ILS/CNY) = ILS 0.5625/CNY E[S, ILS/CNY) = ILS 0.5676/CNY Cross-border capital budgeting under the international parity conditions. 13.1 You work for an Israeli company that is considering an investment in China's Sichuan province. The investment yields expected after-tax Chinese new yuan cash flows (in millions) as follows: +CNY 200m +CNY500m +CNY300m --CNY600m Expected inflation is 6 percent in shekels and 3 percent in yuan. Required returns for this risk-class are ILS = 15 percent in Israeli shekels and iCNY = 11.745 percent in yuan. The spot exchange rate is ILS 0.5526/CNY. Assume the international parity condi- tions hold. S, ILS/CNY 22 VALUATION AND THE STRUCTURE OF MULTINATIONAL OPERATIONS rate. a. Calculate V, SiCNY by discounting at the appropriate risk-adjusted yuan rate iCNY and then converting into shekels at the current spot b. Calculate V. SillS by converting yuan into shekels at expected future spot rates and then discounting at the appropriate rate in shekels. 4.2 The followin also, for 13.5 b, should the manager invest? Should the manager hesge the project's currency risk exposure?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Financial Models For Management And Planning

Authors: James R Morris, John P Daley

2nd Edition

1498765041, 9781498765046