Answered step by step

Verified Expert Solution

Question

1 Approved Answer

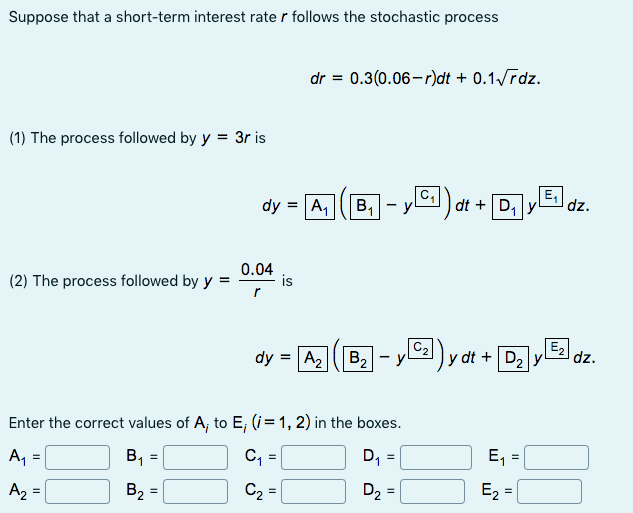

Please solve the following questions.Suppose that a short - term interest rate r follows the stochastic process d r = 0 . 3 ( 0

Please solve the following questions.Suppose that a shortterm interest rate follows the stochastic process

The process followed by is

The process followed by is

Enter the correct values of to in the boxes.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Psychology Of Money Timeless Lessons On Wealth Greed And Happiness

Authors: Morgan Housel

1st Edition

978-0857199096