Answered step by step

Verified Expert Solution

Question

1 Approved Answer

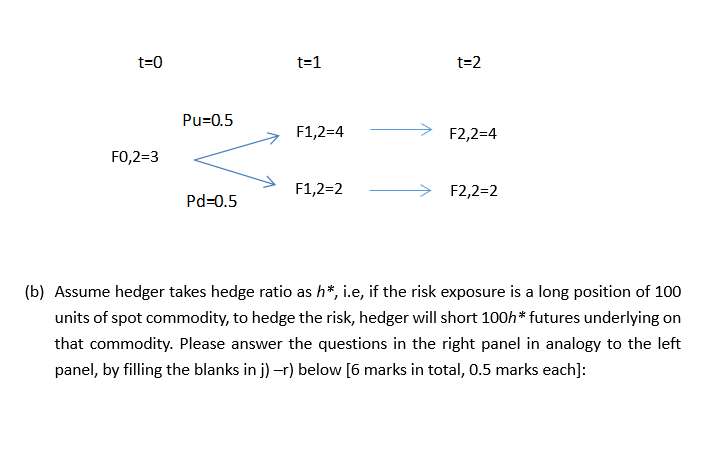

Please solve the right panel as shown above t=0 t=1 t=2 Pu=0.5 50.5 F1,2=4 - > F2,2=4 F0,2=3 Pd=0.5 > F1,2=2 - > F2,2=2 (b)

Please solve the right panel as shown above

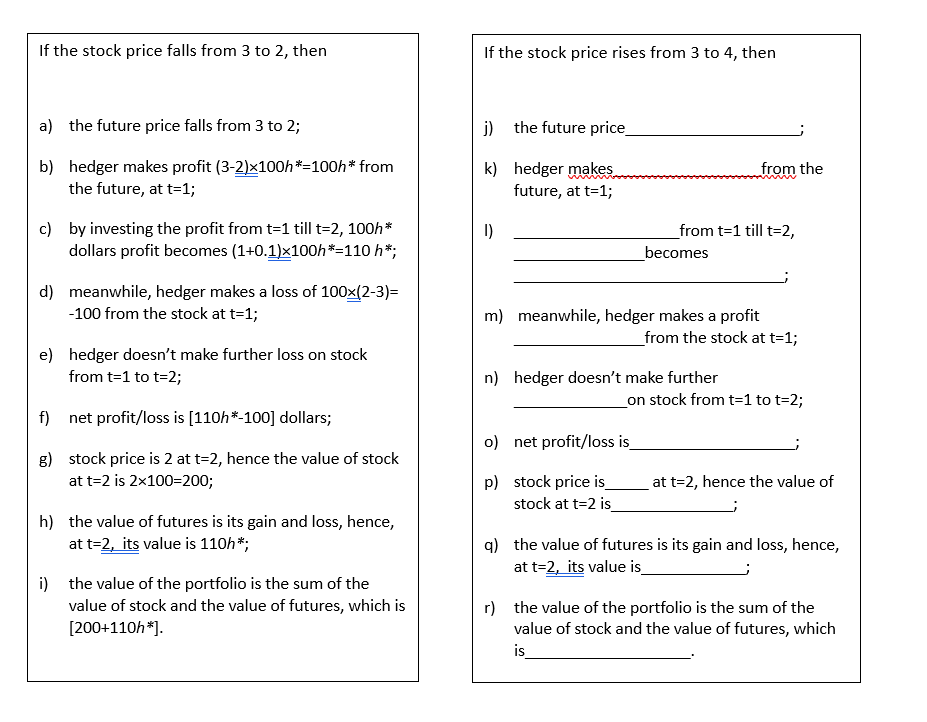

t=0 t=1 t=2 Pu=0.5 50.5 F1,2=4 - > F2,2=4 F0,2=3 Pd=0.5 > F1,2=2 - > F2,2=2 (b) Assume hedger takes hedge ratio as h*, i.e, if the risk exposure is a long position of 100 units of spot commodity, to hedge the risk, hedger will short 100h* futures underlying on that commodity. Please answer the questions in the right panel in analogy to the left panel, by filling the blanks in j) -r) below [6 marks in total, 0.5 marks each]: If the stock price falls from 3 to 2, then If the stock price rises from 3 to 4, then a) the future price falls from 3 to 2; j) the future price b) hedger makes profit (3-2)x100h*=100h* from the future, at t=1; k) hedger makes. future, at t=1; from the c) by investing the profit from t=1 tillt=2, 100h* dollars profit becomes (1+0.1)x100h*=110 h*; from t=1 till t=2, _becomes d) meanwhile, hedger makes a loss of 100x(2-3)= -100 from the stock at t=1; m) meanwhile, hedger makes a profit from the stock at t=1; e) hedger doesn't make further loss on stock from t=1 to t=2; n) hedger doesn't make further __on stock from t=1 to t=2; f) net profit/loss is [110h*-100] dollars; o) net profit/loss is g) stock price is 2 at t=2, hence the value of stock at t=2 is 2x100=200; at t=2, hence the value of p) stock price is stock at t=2 is h) the value of futures is its gain and loss, hence, at t=2, its value is 110h*; q) the value of futures is its gain and loss, hence, at t=2, its value is the value of the portfolio is the sum of the value of stock and the value of futures, which is [200+110h*]. r) the value of the portfolio is the sum of the value of stock and the value of futures, which t=0 t=1 t=2 Pu=0.5 50.5 F1,2=4 - > F2,2=4 F0,2=3 Pd=0.5 > F1,2=2 - > F2,2=2 (b) Assume hedger takes hedge ratio as h*, i.e, if the risk exposure is a long position of 100 units of spot commodity, to hedge the risk, hedger will short 100h* futures underlying on that commodity. Please answer the questions in the right panel in analogy to the left panel, by filling the blanks in j) -r) below [6 marks in total, 0.5 marks each]: If the stock price falls from 3 to 2, then If the stock price rises from 3 to 4, then a) the future price falls from 3 to 2; j) the future price b) hedger makes profit (3-2)x100h*=100h* from the future, at t=1; k) hedger makes. future, at t=1; from the c) by investing the profit from t=1 tillt=2, 100h* dollars profit becomes (1+0.1)x100h*=110 h*; from t=1 till t=2, _becomes d) meanwhile, hedger makes a loss of 100x(2-3)= -100 from the stock at t=1; m) meanwhile, hedger makes a profit from the stock at t=1; e) hedger doesn't make further loss on stock from t=1 to t=2; n) hedger doesn't make further __on stock from t=1 to t=2; f) net profit/loss is [110h*-100] dollars; o) net profit/loss is g) stock price is 2 at t=2, hence the value of stock at t=2 is 2x100=200; at t=2, hence the value of p) stock price is stock at t=2 is h) the value of futures is its gain and loss, hence, at t=2, its value is 110h*; q) the value of futures is its gain and loss, hence, at t=2, its value is the value of the portfolio is the sum of the value of stock and the value of futures, which is [200+110h*]. r) the value of the portfolio is the sum of the value of stock and the value of futures, whichStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

CIA Part 1 Essentials Of Internal Auditing Certified Internal Auditor 2019

Authors: Muhammad Zain

1st Edition

1091949182, 978-1091949188