Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please solve this in handwritten or word form not in excel thanks Case 1 Financial Ratio Analysis Triple A Office Mart Susan Burke, president of

please solve this in handwritten or word form not in excel thanks

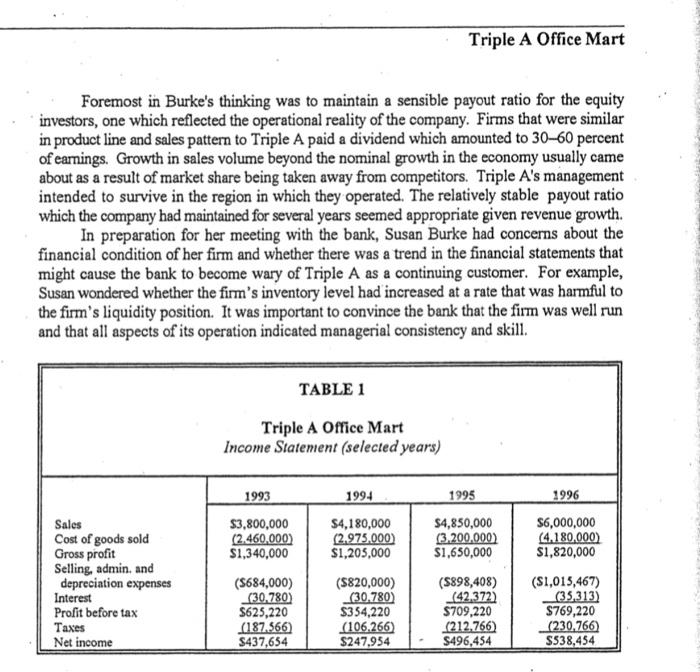

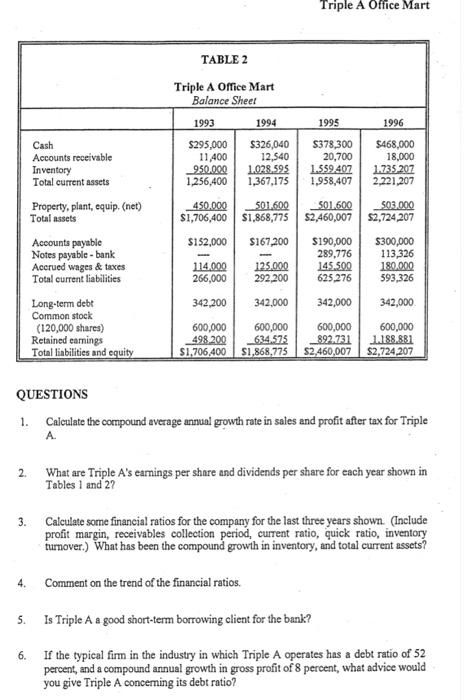

Case 1 Financial Ratio Analysis Triple A Office Mart Susan Burke, president of Triple A Office Mart, studied her notes for the afternoon meeting with the bank's commercial loan committee. The profitable company, organized in 1978, sold a complete line of office equipment, furniture, and supplies. Two stores operated in two adjoining states in the southwestern United States. Budgetary control of the two stores was centralized in the store and office complex which operated in the larger of the two cities. In preparation for the meeting, Burke wondered about the type of information the bank might have with which to make a decision on her loan. She was also concerned about how the bank would view a profitable company that needed to borrow funds. The stores had operated profitably since their inception. Triple A was organized by Burke and a college roommate, Virginia Best, one year after their graduation. Best left the company after only three years to participate in an overseas venture. Her interest was sold to Burke at that time. With the advent of the personal computer, a major component of company sales, and a general trend in the economy toward specialty stores, Triple A had experienced excellent growth in revenue and earnings. Table 1 illustrates a portion of the firm's sales and earnings history. Table 2 provides balance sheets for selected years. The firm had issued no common stock or long-term debt in the recent past. In fact, the second store was opened in 1992 without any additional long-term financing. In the case of the new store, however, there was an increase in inventory and bank borrowing. The company's financial staff wondered if this were a normal state of affairs for an expansion situation. Triple A had traditionally handled its credits well, and the stockholders were generally satisfied with the firm's return on equity. (Stock was offered to the public for the first time in 1980). The primary benefit to the company was the strong local economy. Although it was primarily a service economy, it supported Triple A almost perfectly. A nearby college of business administration, which published an economic report and forecast concerning the local economy, stated that since 1990 the growth of the local GNP had been in the range of 8-10 percent. Susan Burke had, as a long-range plan, every intention of participating in the region's growth and of contributing to it through the efficient operation of her firm. In recent months during early 1996, there had been cause for concern on the part of company management. Prices from suppliers had risen and the firm's financial managers wondered about the effect of this upon profitability and the general operation of the business. The suppliers to the firm were varied, since the firm carried a wide range of office equipment and supplies. As a result, it was not possible to develop a strong and mutually supportive relationship with any one supplier. In general, the company had to deal with the vagaries of the economy. Triple A Office Mart Foremost in Burke's thinking was to maintain a sensible payout ratio for the equity investors, one which reflected the operational reality of the company. Firms that were similar in product line and sales pattern to Triple A paid a dividend which amounted to 30-60 percent of earnings. Growth in sales volume beyond the nominal growth in the economy usually came about as a result of market share being taken away from competitors. Triple A's management intended to survive in the region in which they operated. The relatively stable payout ratio which the company had maintained for several years seemed appropriate given revenue growth. In preparation for her meeting with the bank, Susan Burke had concerns about the financial condition of her firm and whether there was a trend in the financial statements that might cause the bank to become wary of Triple A as a continuing customer. For example, Susan wondered whether the firm's inventory level had increased at a rate that was harmful to the firm's liquidity position. It was important to convince the bank that the firm was well run and that all aspects of its operation indicated managerial consistency and skill. TABLE 1 Triple A Office Mart Income Statement (selected years) 1993 1994 1996 $3,800,000 $4,180,000 $6,000,000 (2.460,000) (2.975,000) (4.180,000) Sales Cost of goods sold Gross profit Selling, admin, and $1,340,000 $1,205,000 $1,820,000 depreciation expenses ($684,000) ($820,000) ($1,015,467) Interest (30,780) (30,780) (35,313) Profit before tax $625,220 $354,220 $769,220 Taxes (187.566) (106.266) (230.766) Net income $437,654 $247,954 $538,454 1995 $4,850,000 (3,200,000) $1,650,000 ($898,408) (42,372) $709,220 (212,766) $496,454 Triple A Office Mart TABLE 2 Triple A Office Mart Balance Sheet 1993 1994 1995 1996 $378,300 $468,000 Cash Accounts receivable $295,000 $326,040 11,400 12,540 20,700 18,000 Inventory 950.000 1.028.595 1.559.407 1.735.207 Total current assets 1,256,400 1,367,175 1,958,407 2,221,207 501,600 503.000 Property, plant, equip. (net) Total assets 450.000 501,600 $1,706,400 $1,868,775 $2,460,007 $2,724,207 $152,000 $167,200 $190,000 $300,000 www - 289,776 113,326 Accounts payable Notes payable-bank Accrued wages & taxes Total current liabilities 114.000 125.000 145.500 180.000 266,000 292,200 625,276 593,326 342,200 342,000 342,000 342,000 Long-term debt Common stock (120,000 shares) 600,000 600,000 600,000 600,000 498.200 634.575 892.731 1.188.881 Retained earnings Total liabilities and equity $1,706,400 $1,868,775 $2,460,007 $2,724,207 QUESTIONS 1. Calculate the compound average annual growth rate in sales and profit after tax for Triple A. 2. What are Triple A's earnings per share and dividends per share for each year shown in Tables 1 and 27 3. Calculate some financial ratios for the company for the last three years shown. (Include profit margin, receivables collection period, current ratio, quick ratio, inventory turnover.) What has been the compound growth in inventory, and total current assets? 4. Comment on the trend of the financial ratios. 5. Is Triple A a good short-term borrowing client for the bank? 6. If the typical firm in the industry in which Triple A operates has a debt ratio of 52 percent, and a compound annual growth in gross profit of 8 percent, what advice would you give Triple A concerning its debt ratio? N Case 1 Financial Ratio Analysis Triple A Office Mart Susan Burke, president of Triple A Office Mart, studied her notes for the afternoon meeting with the bank's commercial loan committee. The profitable company, organized in 1978, sold a complete line of office equipment, furniture, and supplies. Two stores operated in two adjoining states in the southwestern United States. Budgetary control of the two stores was centralized in the store and office complex which operated in the larger of the two cities. In preparation for the meeting, Burke wondered about the type of information the bank might have with which to make a decision on her loan. She was also concerned about how the bank would view a profitable company that needed to borrow funds. The stores had operated profitably since their inception. Triple A was organized by Burke and a college roommate, Virginia Best, one year after their graduation. Best left the company after only three years to participate in an overseas venture. Her interest was sold to Burke at that time. With the advent of the personal computer, a major component of company sales, and a general trend in the economy toward specialty stores, Triple A had experienced excellent growth in revenue and earnings. Table 1 illustrates a portion of the firm's sales and earnings history. Table 2 provides balance sheets for selected years. The firm had issued no common stock or long-term debt in the recent past. In fact, the second store was opened in 1992 without any additional long-term financing. In the case of the new store, however, there was an increase in inventory and bank borrowing. The company's financial staff wondered if this were a normal state of affairs for an expansion situation. Triple A had traditionally handled its credits well, and the stockholders were generally satisfied with the firm's return on equity. (Stock was offered to the public for the first time in 1980). The primary benefit to the company was the strong local economy. Although it was primarily a service economy, it supported Triple A almost perfectly. A nearby college of business administration, which published an economic report and forecast concerning the local economy, stated that since 1990 the growth of the local GNP had been in the range of 8-10 percent. Susan Burke had, as a long-range plan, every intention of participating in the region's growth and of contributing to it through the efficient operation of her firm. In recent months during early 1996, there had been cause for concern on the part of company management. Prices from suppliers had risen and the firm's financial managers wondered about the effect of this upon profitability and the general operation of the business. The suppliers to the firm were varied, since the firm carried a wide range of office equipment and supplies. As a result, it was not possible to develop a strong and mutually supportive relationship with any one supplier. In general, the company had to deal with the vagaries of the economy. Triple A Office Mart Foremost in Burke's thinking was to maintain a sensible payout ratio for the equity investors, one which reflected the operational reality of the company. Firms that were similar in product line and sales pattern to Triple A paid a dividend which amounted to 30-60 percent of earnings. Growth in sales volume beyond the nominal growth in the economy usually came about as a result of market share being taken away from competitors. Triple A's management intended to survive in the region in which they operated. The relatively stable payout ratio which the company had maintained for several years seemed appropriate given revenue growth. In preparation for her meeting with the bank, Susan Burke had concerns about the financial condition of her firm and whether there was a trend in the financial statements that might cause the bank to become wary of Triple A as a continuing customer. For example, Susan wondered whether the firm's inventory level had increased at a rate that was harmful to the firm's liquidity position. It was important to convince the bank that the firm was well run and that all aspects of its operation indicated managerial consistency and skill. TABLE 1 Triple A Office Mart Income Statement (selected years) 1993 1994 1996 $3,800,000 $4,180,000 $6,000,000 (2.460,000) (2.975,000) (4.180,000) Sales Cost of goods sold Gross profit Selling, admin, and $1,340,000 $1,205,000 $1,820,000 depreciation expenses ($684,000) ($820,000) ($1,015,467) Interest (30,780) (30,780) (35,313) Profit before tax $625,220 $354,220 $769,220 Taxes (187.566) (106.266) (230.766) Net income $437,654 $247,954 $538,454 1995 $4,850,000 (3,200,000) $1,650,000 ($898,408) (42,372) $709,220 (212,766) $496,454 Triple A Office Mart TABLE 2 Triple A Office Mart Balance Sheet 1993 1994 1995 1996 $378,300 $468,000 Cash Accounts receivable $295,000 $326,040 11,400 12,540 20,700 18,000 Inventory 950.000 1.028.595 1.559.407 1.735.207 Total current assets 1,256,400 1,367,175 1,958,407 2,221,207 501,600 503.000 Property, plant, equip. (net) Total assets 450.000 501,600 $1,706,400 $1,868,775 $2,460,007 $2,724,207 $152,000 $167,200 $190,000 $300,000 www - 289,776 113,326 Accounts payable Notes payable-bank Accrued wages & taxes Total current liabilities 114.000 125.000 145.500 180.000 266,000 292,200 625,276 593,326 342,200 342,000 342,000 342,000 Long-term debt Common stock (120,000 shares) 600,000 600,000 600,000 600,000 498.200 634.575 892.731 1.188.881 Retained earnings Total liabilities and equity $1,706,400 $1,868,775 $2,460,007 $2,724,207 QUESTIONS 1. Calculate the compound average annual growth rate in sales and profit after tax for Triple A. 2. What are Triple A's earnings per share and dividends per share for each year shown in Tables 1 and 27 3. Calculate some financial ratios for the company for the last three years shown. (Include profit margin, receivables collection period, current ratio, quick ratio, inventory turnover.) What has been the compound growth in inventory, and total current assets? 4. Comment on the trend of the financial ratios. 5. Is Triple A a good short-term borrowing client for the bank? 6. If the typical firm in the industry in which Triple A operates has a debt ratio of 52 percent, and a compound annual growth in gross profit of 8 percent, what advice would you give Triple A concerning its debt ratio? N Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Economics Of Money Banking And Finance

Authors: Howells, Keith Bain

3rd Edition

0273693395, 978-0273693390