Question

Please solve this problem urgently if you know perfect thanks Information is clear what more u want dear Which bit not clear tell me I

Please solve this problem urgently if you know perfect thanks

Information is clear what more u want dear

Which bit not clear tell me I will tell you the picture numbers

Please solve this now it's clear upload just now waiting for answer plz do bits I will appreciate thanks

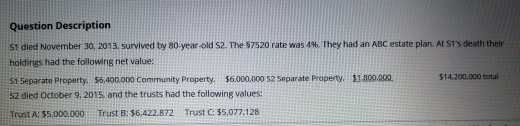

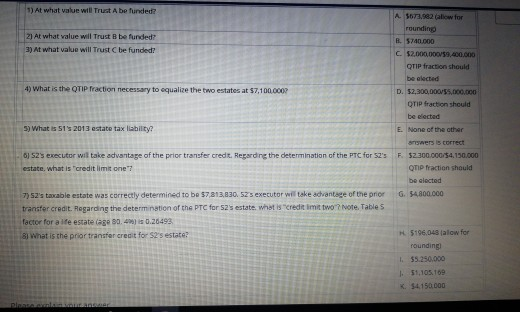

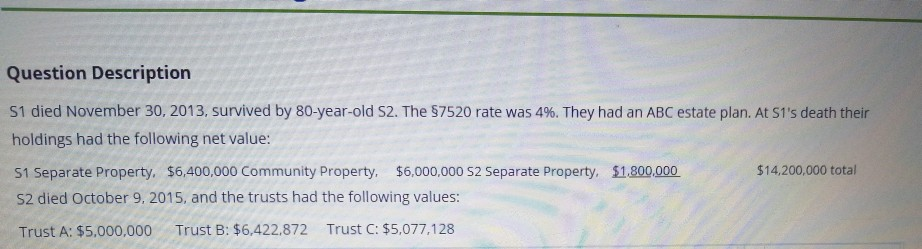

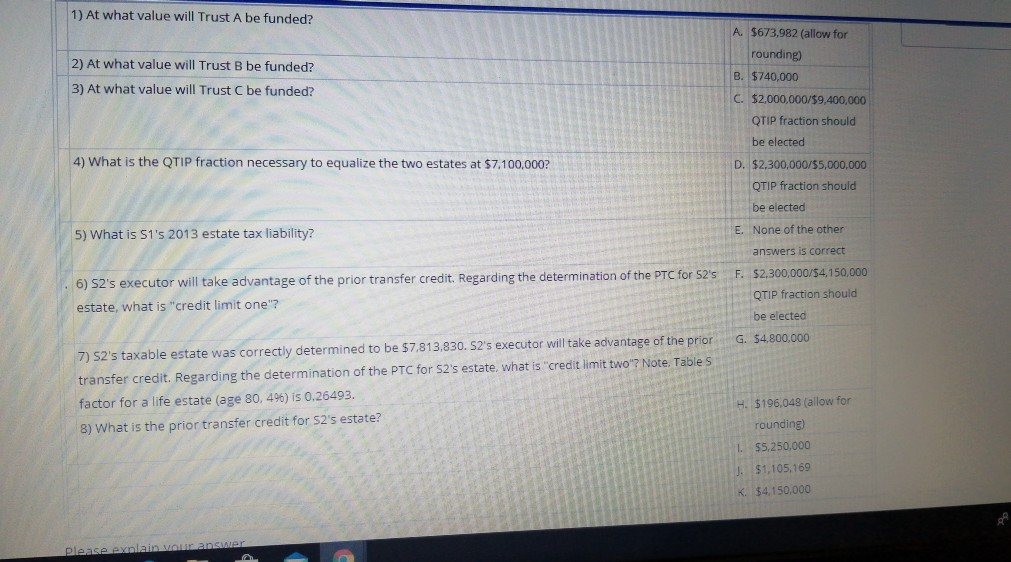

Question Description S1 died November 30, 2013. survived by 80-year-old S2. The S7520 rate was 4. They had an ABC estate plan. At 51's death their holdings had the following net value: 51 Separate Property. 56,400.000 Community Property. $6.000.000 S2 Separate Property. 1.300.000 $14,200,000 total S2 died October 9, 2015. and the trusts had the following values: Trust A! $5.000.000 Trust B: $6,422.872 Trust C: $5,077,128 3) At what value will Trust A befunded? 2) At what value will Trust be funded? 3) At what value will Trust be funded? 4) What is the OTIP Traction necessary to equalize the two estates at 57,100.000 A $673,982 (allow for rounding B. 5740.000 C$2,000.00.400.000 QTIP fraction should be elected D. $2,300,000/35.000.000 Tip fraction should be elected E. None of the other answers is correct F $2.300.000/54,150.000 OTIP fraction should be elected 5) What is 51' 2013 estate tax liability 6J 525 executor will take advantage of the prior transfer credt. Regarding the determination of the PTC for Sz's estate. what is credit limit one? G. 54,800.000 7) S2's taxable estate was correctly determined to be $7,813,830.525 executor we take advantage of the prior transfer credit. Regarding the determination of the PTC for S2's estate. What is "creditimit two Note Tables factor for a life estate age 30.41 s 0.26493 8 What is the prior transfer credit for S2's estate H5196,043 alow for rounding I55.250.000 1 31.105.109 K. $4150.000 Question Description S1 died November 30, 2013, survived by 80-year-old S2. The $7520 rate was 4%. They had an ABC estate plan. At Si's death their holdings had the following net value: 51 Separate Property. $6,400,000 Community Property. $6,000,000 S2 Separate Property. $1.800.000 $14,200,000 total S2 died October 9, 2015, and the trusts had the following values: Trust A: $5,000,000 Trust B: $6,422,872 Trust C: $5,077,128 1) At what value will Trust A be funded? 2) At what value will Trust B be funded? 3) At what value will Trust C be funded? A. $673,982 (allow for rounding) B. $740.000 C. $2,000,000/$9,400,000 QTIP fraction should be elected 4) What is the QTIP fraction necessary to equalize the two estates at $7,100,000? D. $2,300,000/$5.000.000 QTIP fraction should be elected E. None of the other 5) What is S1's 2013 estate tax liability? 6) S2's executor will take advantage of the prior transfer credit. Regarding the determination of the PTC for 52's estate, what is "credit limit one"? answers is correct F. $2,300,000/54,150,000 QTIP fraction should be elected G. $4.800,000 7) 52's taxable estate was correctly determined to be $7.813,830. S2's executor will take advantage of the prior transfer credit. Regarding the determination of the PTC for S2's estate, what is "credit limit two"? Note. Tables factor for a life estate (age 80, 496) is 0.26493. 8) What is the prior transfer credit for S2's estate? H. $196,048 (allow for rounding) 1 $5,250,000 $1,105,169 K $4,150,000 please eyala Manancier Question Description S1 died November 30, 2013. survived by 80-year-old S2. The S7520 rate was 4. They had an ABC estate plan. At 51's death their holdings had the following net value: 51 Separate Property. 56,400.000 Community Property. $6.000.000 S2 Separate Property. 1.300.000 $14,200,000 total S2 died October 9, 2015. and the trusts had the following values: Trust A! $5.000.000 Trust B: $6,422.872 Trust C: $5,077,128 3) At what value will Trust A befunded? 2) At what value will Trust be funded? 3) At what value will Trust be funded? 4) What is the OTIP Traction necessary to equalize the two estates at 57,100.000 A $673,982 (allow for rounding B. 5740.000 C$2,000.00.400.000 QTIP fraction should be elected D. $2,300,000/35.000.000 Tip fraction should be elected E. None of the other answers is correct F $2.300.000/54,150.000 OTIP fraction should be elected 5) What is 51' 2013 estate tax liability 6J 525 executor will take advantage of the prior transfer credt. Regarding the determination of the PTC for Sz's estate. what is credit limit one? G. 54,800.000 7) S2's taxable estate was correctly determined to be $7,813,830.525 executor we take advantage of the prior transfer credit. Regarding the determination of the PTC for S2's estate. What is "creditimit two Note Tables factor for a life estate age 30.41 s 0.26493 8 What is the prior transfer credit for S2's estate H5196,043 alow for rounding I55.250.000 1 31.105.109 K. $4150.000 Question Description S1 died November 30, 2013, survived by 80-year-old S2. The $7520 rate was 4%. They had an ABC estate plan. At Si's death their holdings had the following net value: 51 Separate Property. $6,400,000 Community Property. $6,000,000 S2 Separate Property. $1.800.000 $14,200,000 total S2 died October 9, 2015, and the trusts had the following values: Trust A: $5,000,000 Trust B: $6,422,872 Trust C: $5,077,128 1) At what value will Trust A be funded? 2) At what value will Trust B be funded? 3) At what value will Trust C be funded? A. $673,982 (allow for rounding) B. $740.000 C. $2,000,000/$9,400,000 QTIP fraction should be elected 4) What is the QTIP fraction necessary to equalize the two estates at $7,100,000? D. $2,300,000/$5.000.000 QTIP fraction should be elected E. None of the other 5) What is S1's 2013 estate tax liability? 6) S2's executor will take advantage of the prior transfer credit. Regarding the determination of the PTC for 52's estate, what is "credit limit one"? answers is correct F. $2,300,000/54,150,000 QTIP fraction should be elected G. $4.800,000 7) 52's taxable estate was correctly determined to be $7.813,830. S2's executor will take advantage of the prior transfer credit. Regarding the determination of the PTC for S2's estate, what is "credit limit two"? Note. Tables factor for a life estate (age 80, 496) is 0.26493. 8) What is the prior transfer credit for S2's estate? H. $196,048 (allow for rounding) 1 $5,250,000 $1,105,169 K $4,150,000 please eyala ManancierStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Concepts And Applications

Authors: K. Fred Skousen, James D. Stice, Earl Kay. Stice, W. Steve Albrecht

7th Edition

0538876255, 978-0538876254