Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please solve. urgent XYZ Ltd. is currently trading at Rs. 190 with call options expiring December. The annualized volatility of the stock is 20% and

please solve. urgent

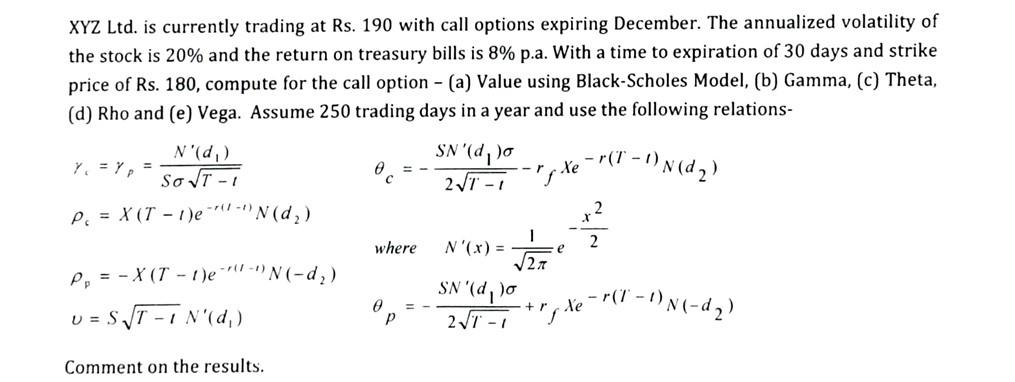

XYZ Ltd. is currently trading at Rs. 190 with call options expiring December. The annualized volatility of the stock is 20% and the return on treasury bills is 8% p.a. With a time to expiration of 30 days and strike price of Rs. 180, compute for the call option - (a) Value using Black-Scholes Model, (b) Gamma, (c) Theta, (d) Rho and (e) Vega. Assume 250 trading days in a year and use the following relations- N'(d,) So T-1 - SN'(d)o 27-1 de (T 1) N (d ) P = X(T-1)e-N(d) where N'(x) = P = -X (T-1)e-(-)N(-d) SN'(d)o U = S T-1 N'(d) P 27-1 Comment on the results. I 27 2 Xer(1. S 1-D) N (-4) XYZ Ltd. is currently trading at Rs. 190 with call options expiring December. The annualized volatility of the stock is 20% and the return on treasury bills is 8% p.a. With a time to expiration of 30 days and strike price of Rs. 180, compute for the call option - (a) Value using Black-Scholes Model, (b) Gamma, (c) Theta, (d) Rho and (e) Vega. Assume 250 trading days in a year and use the following relations- N'(d,) So T-1 - SN'(d)o 27-1 de (T 1) N (d ) P = X(T-1)e-N(d) where N'(x) = P = -X (T-1)e-(-)N(-d) SN'(d)o U = S T-1 N'(d) P 27-1 Comment on the results. I 27 2 Xer(1. S 1-D) N (-4)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading QuickStart Guide The Simplified Beginners Guide To Options Trading

Authors: Clydebank Finance

2nd Edition

1945051051, 978-1945051050