Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please to be as detailed as possible with the solution. Assume zero transactions costs and the following information: Spot rate of the Japanese yen =

Please to be as detailed as possible with the solution.

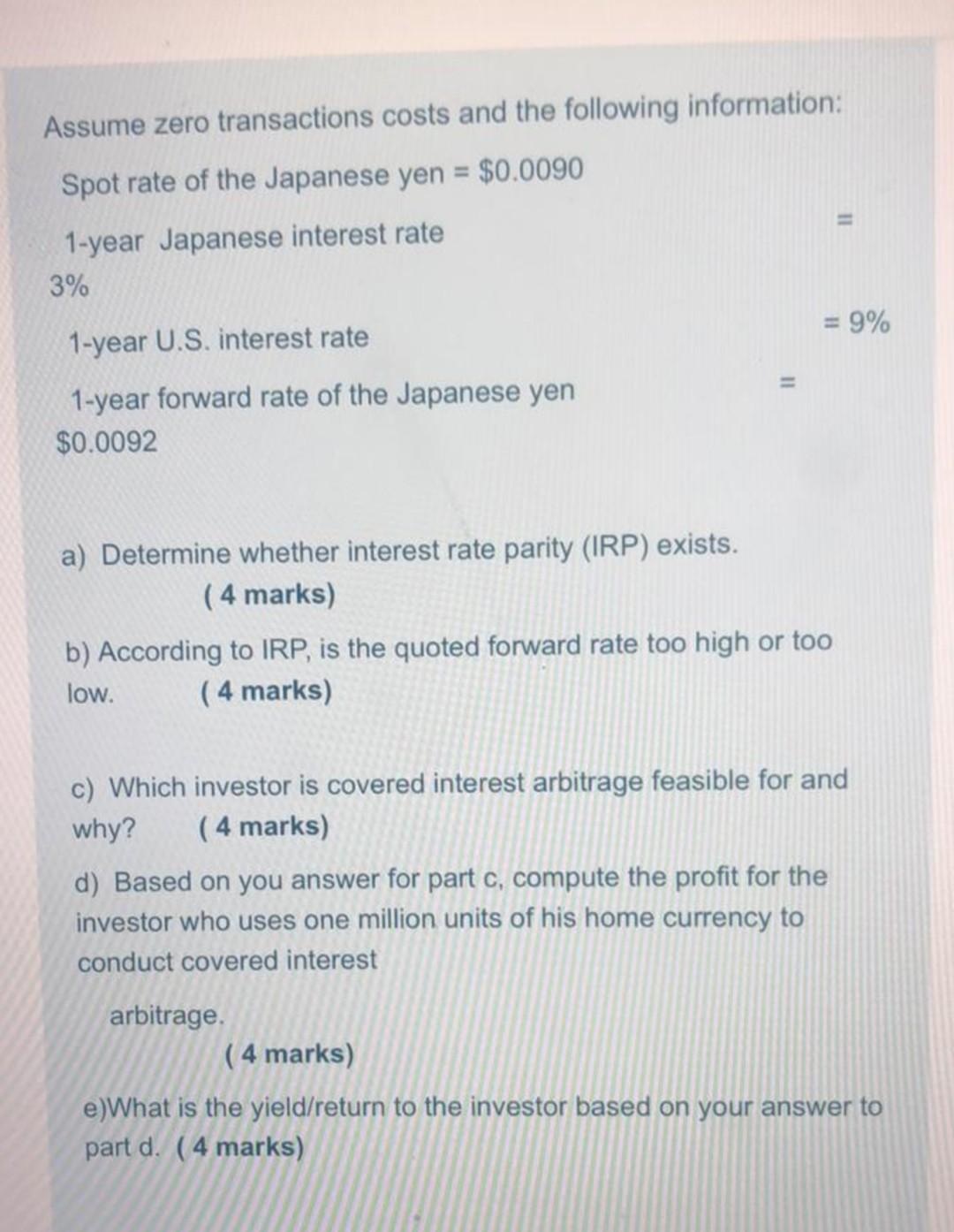

Assume zero transactions costs and the following information: Spot rate of the Japanese yen = $0.0090 1-year Japanese interest rate 3% 11 = 9% 1-year U.S. interest rate 1-year forward rate of the Japanese yen $0.0092 a) Determine whether interest rate parity (IRP) exists. (4 marks) b) According to IRP, is the quoted forward rate too high or too low. (4 marks) c) Which investor is covered interest arbitrage feasible for and why? (4 marks) d) Based on you answer for part c, compute the profit for the investor who uses one million units of his home currency to conduct covered interest arbitrage. (4 marks) e)What is the yield/return to the investor based on your answer to part d. (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Capital Failure Rebuilding Trust In Financial Services

Authors: Nicholas Morris , David Vines

1st Edition

0198712227,019102077X