Please type the answer by computer so I can see it clearly, thank you!!!

T-Toys Ltd has engaged Mr Cheung as a marketing manager since 2016. T-Toys Ltd is a Hong Kong-based firm that specializes in toy trading. Mr. Cheung was compelled to go regularly to China because T-Toys Ltd's primary clients are based there. For the fiscal year ending March 31, 2021, he presents the following data:

information maybe needed:

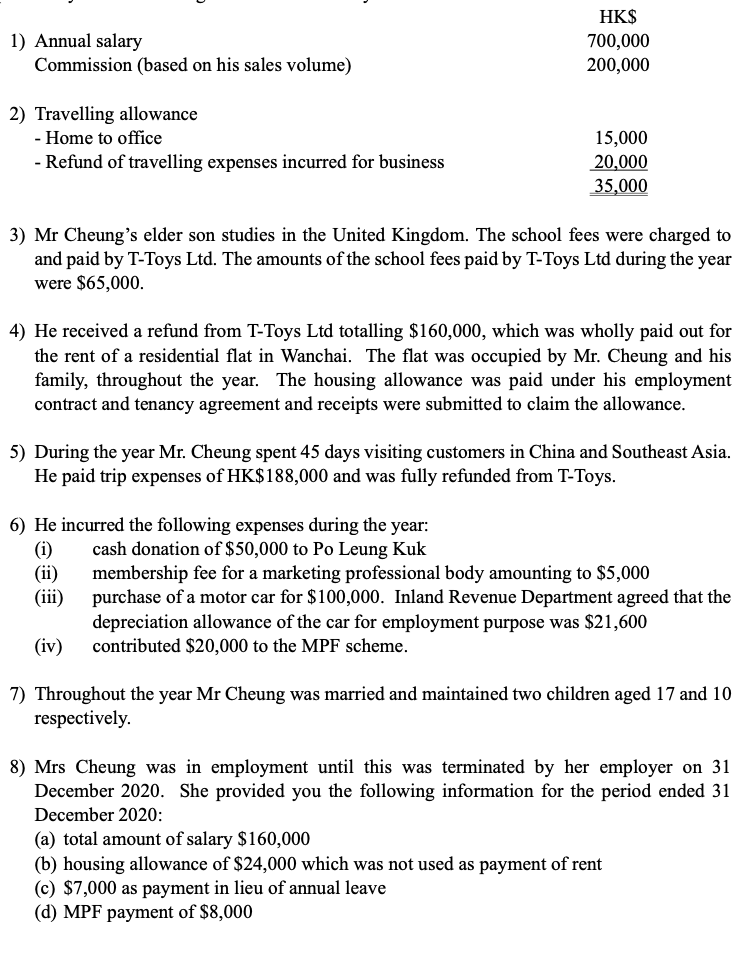

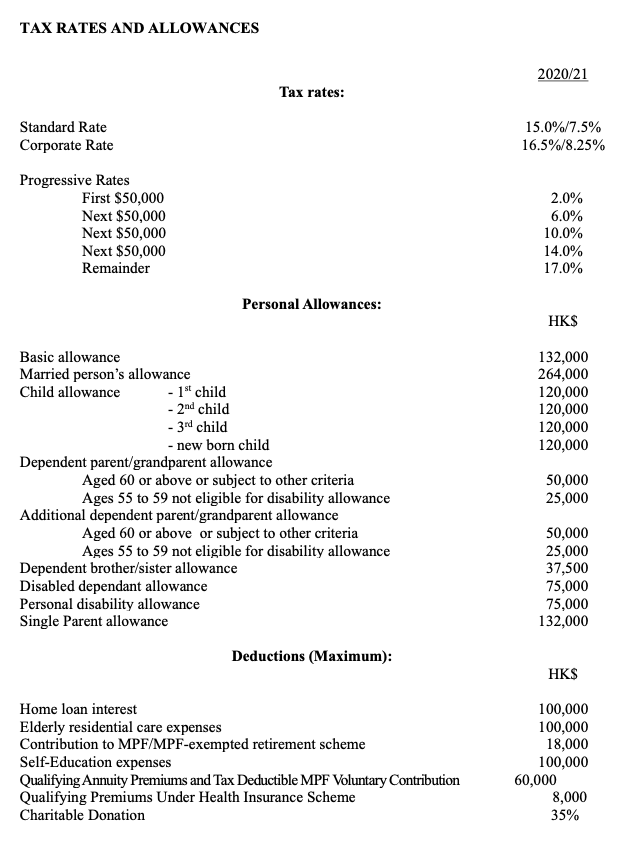

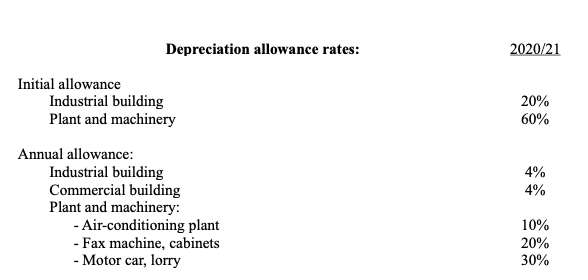

1) Annual salary HK$ 700,000 200,000 Commission (based on his sales volume) 2) Travelling allowance - Home to office 15,000 - Refund of travelling expenses incurred for business 20,000 35,000 3) Mr Cheung's elder son studies in the United Kingdom. The school fees were charged to and paid by T-Toys Ltd. The amounts of the school fees paid by T-Toys Ltd during the year were $65,000. 4) He received a refund from T-Toys Ltd totalling $160,000, which was wholly paid out for the rent of a residential flat in Wanchai. The flat was occupied by Mr. Cheung and his family, throughout the year. The housing allowance was paid under his employment contract and tenancy agreement and receipts were submitted to claim the allowance. 5) During the year Mr. Cheung spent 45 days visiting customers in China and Southeast Asia. He paid trip expenses of HK$188,000 and was fully refunded from T-Toys. 6) He incurred the following expenses during the year: (i) cash donation of $50,000 to Po Leung Kuk (ii) membership fee for a marketing professional body amounting to $5,000 (iii) purchase of a motor car for $100,000. Inland Revenue Department agreed that the depreciation allowance of the car for employment purpose was $21,600 contributed $20,000 to the MPF scheme. (iv) 7) Throughout the year Mr Cheung was married and maintained two children aged 17 and 10 respectively. 8) Mrs Cheung was in employment until this was terminated by her employer on 31 December 2020. She provided you the following information for the period ended 31 December 2020: (a) total amount of salary $160,000 (b) housing allowance of $24,000 which was not used as payment of rent (c) $7,000 as payment in lieu of annual leave (d) MPF payment of $8,000 Required (a) Compute the salaries tax liabilities of Mr. Cheung for the year of assessment 2020/21. Mr. Cheung is nominated to claim all the personal allowances. Ignore provisional tax and tax rebate. (15 marks) (b) Compute the salaries tax liabilities of Mrs. Cheung for the year of assessment 2020/21. Ignore provisional tax and tax rebate. (6 marks) TAX RATES AND ALLOWANCES Standard Rate Corporate Rate Progressive Rates Tax rates: First $50,000 Next $50,000 Next $50,000 Next $50,000 Remainder Personal Allowances: Basic allowance Married person's allowance Child allowance - 1st child - 2nd child - 3rd child - new born child Dependent parent/grandparent allowance Aged 60 or above or subject to other criteria Ages 55 to 59 not eligible for disability allowance Additional dependent parent/grandparent allowance Aged 60 or above or subject to other criteria Ages 55 to 59 not eligible for disability allowance Dependent brother/sister allowance Disabled dependant allowance Personal disability allowance Single Parent allowance Deductions (Maximum): Home loan interest Elderly residential care expenses Contribution to MPF/MPF-exempted retirement scheme Self-Education expenses Qualifying Annuity Premiums and Tax Deductible MPF Voluntary Contribution Qualifying Premiums Under Health Insurance Scheme Charitable Donation 2020/21 15.0%/7.5% 16.5%/8.25% 2.0% 6.0% 10.0% 14.0% 17.0% HK$ 132,000 264,000 120,000 120,000 120,000 120,000 50,000 25,000 50,000 25,000 37,500 75,000 75,000 132,000 HK$ 100,000 100,000 18,000 100,000 8,000 35% 60,000 Initial allowance Annual allowance: Depreciation allowance rates: Industrial building Plant and machinery Industrial building Commercial building Plant and machinery: - Air-conditioning plant - Fax machine, cabinets - Motor car, lorry 2020/21 20% 60% 4% 4% 10% 20% 30% 1) Annual salary HK$ 700,000 200,000 Commission (based on his sales volume) 2) Travelling allowance - Home to office 15,000 - Refund of travelling expenses incurred for business 20,000 35,000 3) Mr Cheung's elder son studies in the United Kingdom. The school fees were charged to and paid by T-Toys Ltd. The amounts of the school fees paid by T-Toys Ltd during the year were $65,000. 4) He received a refund from T-Toys Ltd totalling $160,000, which was wholly paid out for the rent of a residential flat in Wanchai. The flat was occupied by Mr. Cheung and his family, throughout the year. The housing allowance was paid under his employment contract and tenancy agreement and receipts were submitted to claim the allowance. 5) During the year Mr. Cheung spent 45 days visiting customers in China and Southeast Asia. He paid trip expenses of HK$188,000 and was fully refunded from T-Toys. 6) He incurred the following expenses during the year: (i) cash donation of $50,000 to Po Leung Kuk (ii) membership fee for a marketing professional body amounting to $5,000 (iii) purchase of a motor car for $100,000. Inland Revenue Department agreed that the depreciation allowance of the car for employment purpose was $21,600 contributed $20,000 to the MPF scheme. (iv) 7) Throughout the year Mr Cheung was married and maintained two children aged 17 and 10 respectively. 8) Mrs Cheung was in employment until this was terminated by her employer on 31 December 2020. She provided you the following information for the period ended 31 December 2020: (a) total amount of salary $160,000 (b) housing allowance of $24,000 which was not used as payment of rent (c) $7,000 as payment in lieu of annual leave (d) MPF payment of $8,000 Required (a) Compute the salaries tax liabilities of Mr. Cheung for the year of assessment 2020/21. Mr. Cheung is nominated to claim all the personal allowances. Ignore provisional tax and tax rebate. (15 marks) (b) Compute the salaries tax liabilities of Mrs. Cheung for the year of assessment 2020/21. Ignore provisional tax and tax rebate. (6 marks) TAX RATES AND ALLOWANCES Standard Rate Corporate Rate Progressive Rates Tax rates: First $50,000 Next $50,000 Next $50,000 Next $50,000 Remainder Personal Allowances: Basic allowance Married person's allowance Child allowance - 1st child - 2nd child - 3rd child - new born child Dependent parent/grandparent allowance Aged 60 or above or subject to other criteria Ages 55 to 59 not eligible for disability allowance Additional dependent parent/grandparent allowance Aged 60 or above or subject to other criteria Ages 55 to 59 not eligible for disability allowance Dependent brother/sister allowance Disabled dependant allowance Personal disability allowance Single Parent allowance Deductions (Maximum): Home loan interest Elderly residential care expenses Contribution to MPF/MPF-exempted retirement scheme Self-Education expenses Qualifying Annuity Premiums and Tax Deductible MPF Voluntary Contribution Qualifying Premiums Under Health Insurance Scheme Charitable Donation 2020/21 15.0%/7.5% 16.5%/8.25% 2.0% 6.0% 10.0% 14.0% 17.0% HK$ 132,000 264,000 120,000 120,000 120,000 120,000 50,000 25,000 50,000 25,000 37,500 75,000 75,000 132,000 HK$ 100,000 100,000 18,000 100,000 8,000 35% 60,000 Initial allowance Annual allowance: Depreciation allowance rates: Industrial building Plant and machinery Industrial building Commercial building Plant and machinery: - Air-conditioning plant - Fax machine, cabinets - Motor car, lorry 2020/21 20% 60% 4% 4% 10% 20% 30%