Answered step by step

Verified Expert Solution

Question

1 Approved Answer

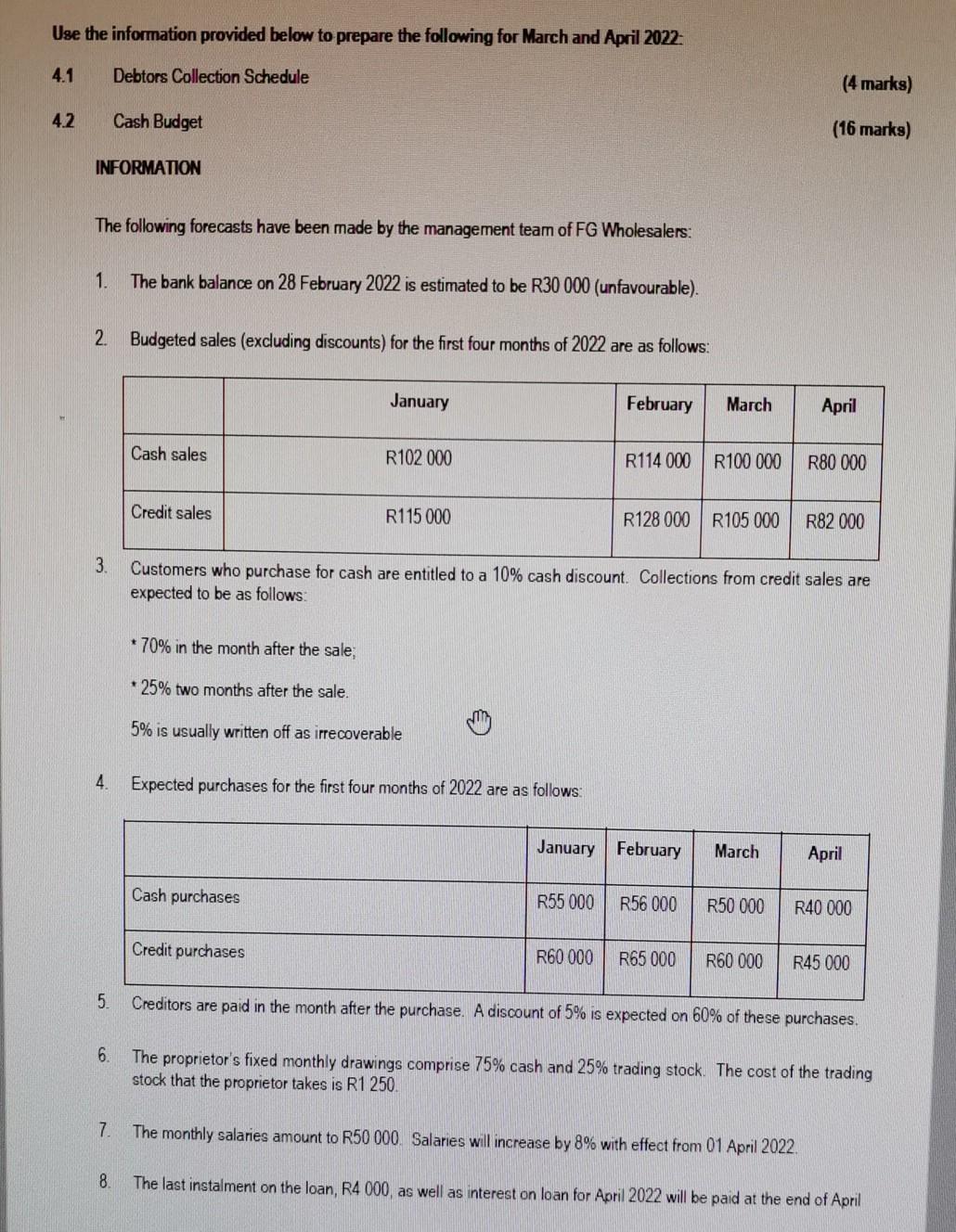

Please urgently answer all questions SECTION A [100 MARKS] Answer ALL the questions in this section. Use the information provided below to calculate the following

Please urgently answer all questions

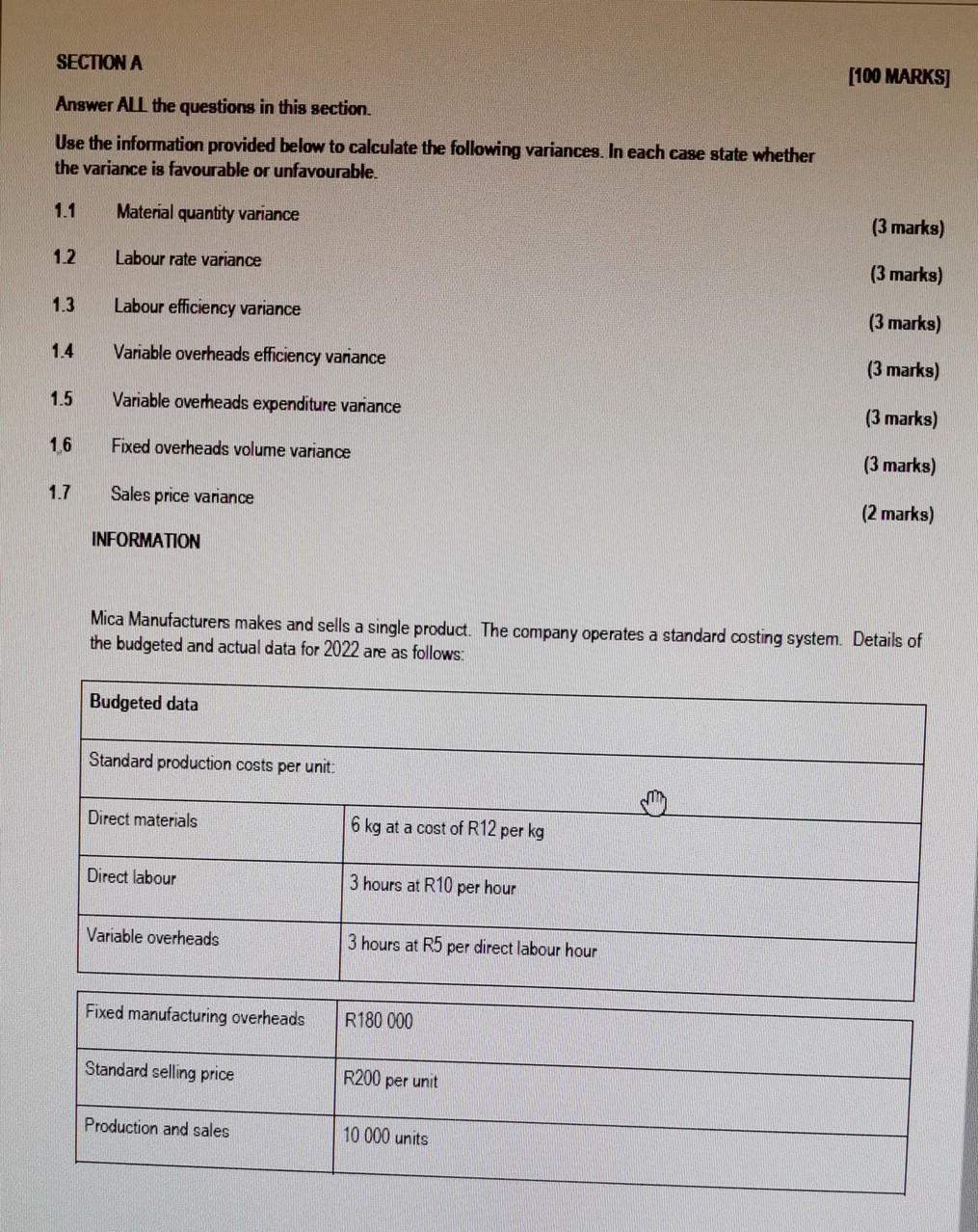

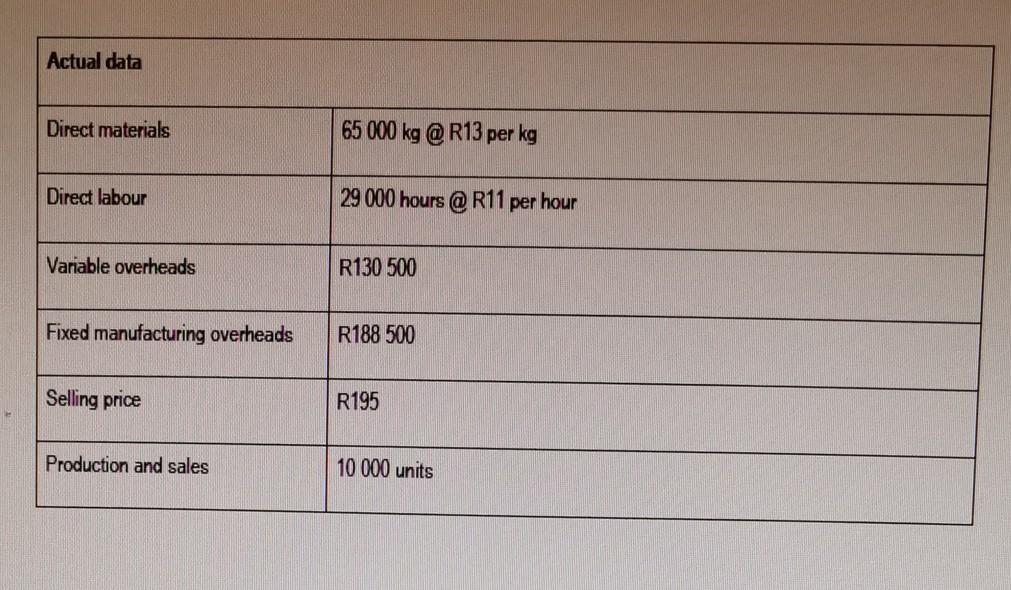

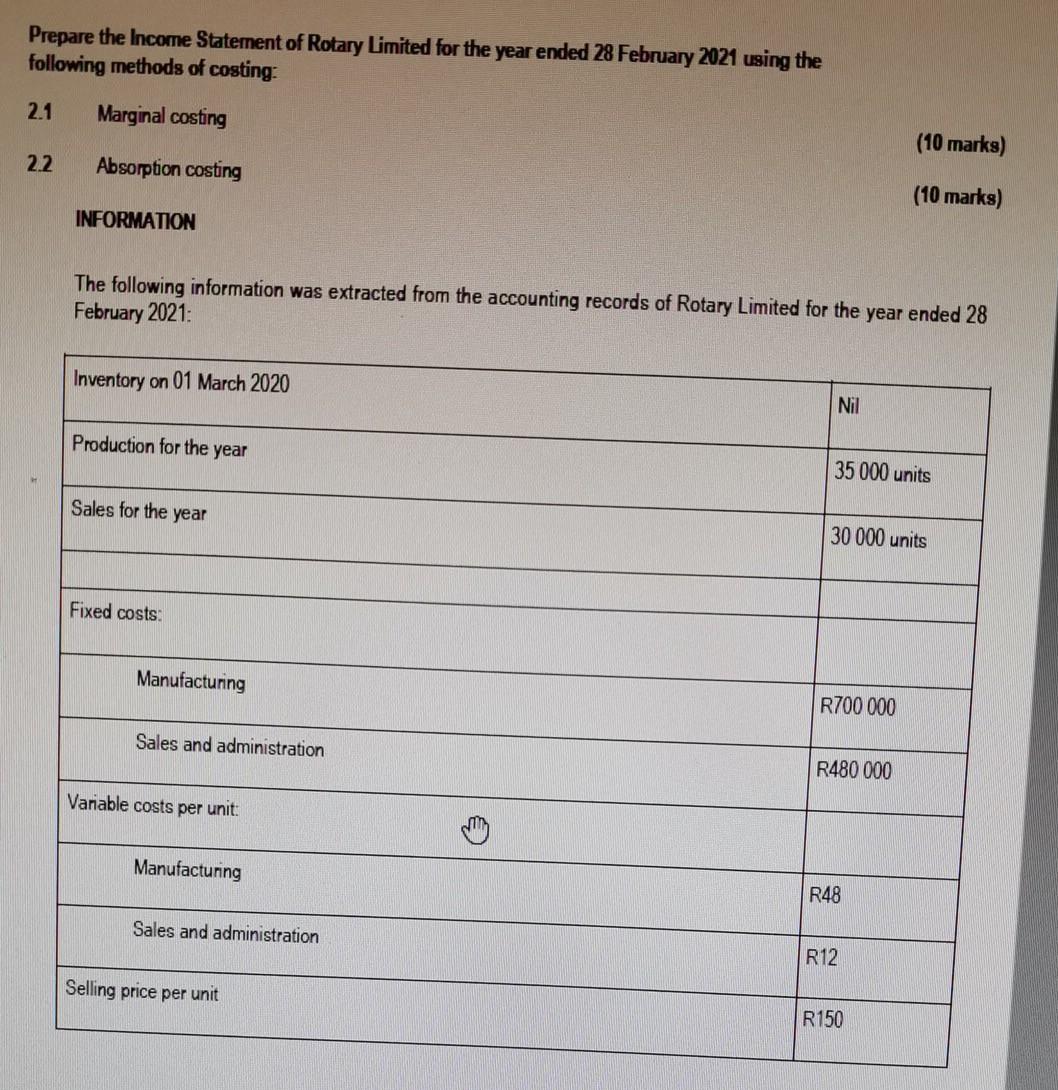

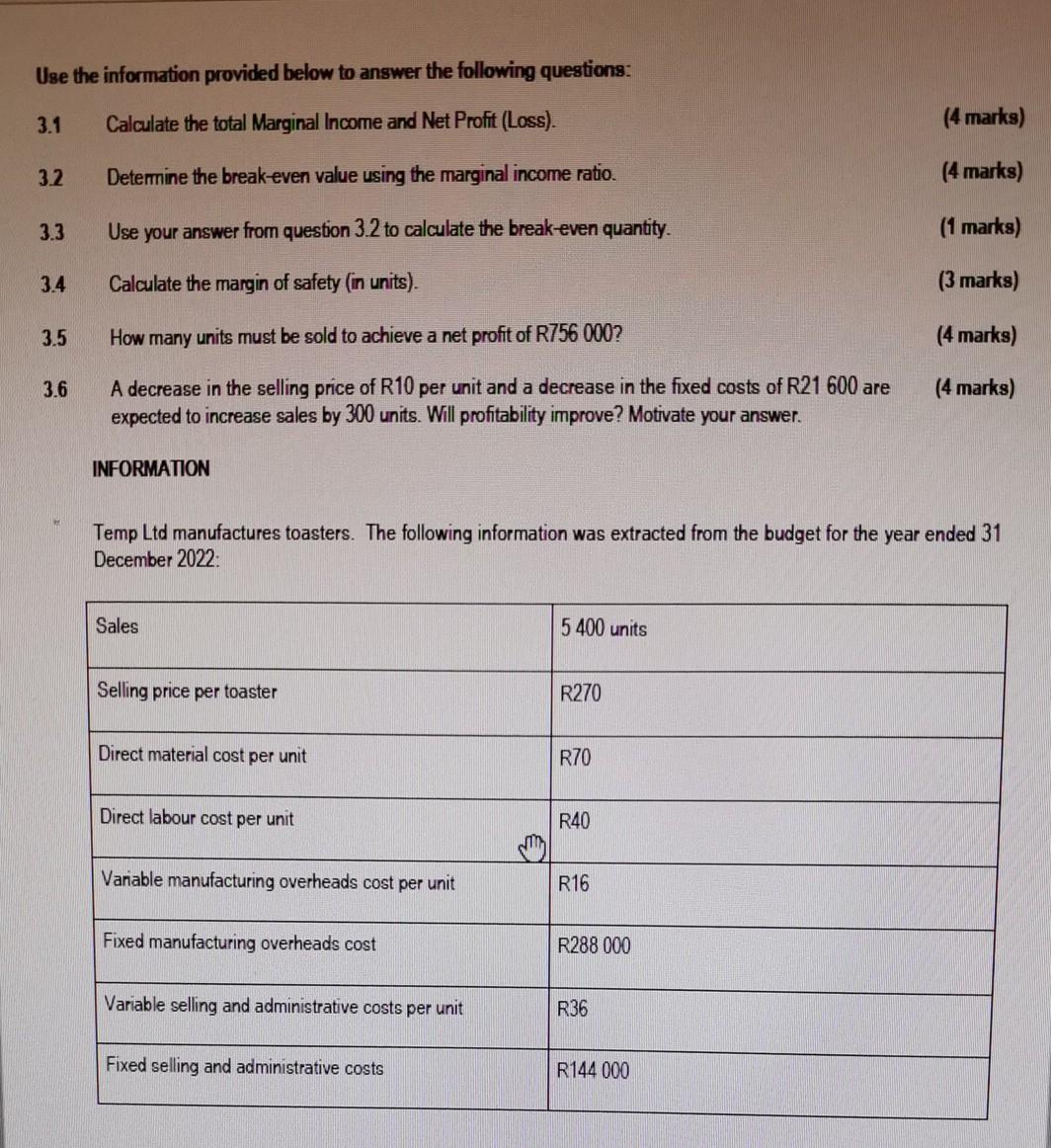

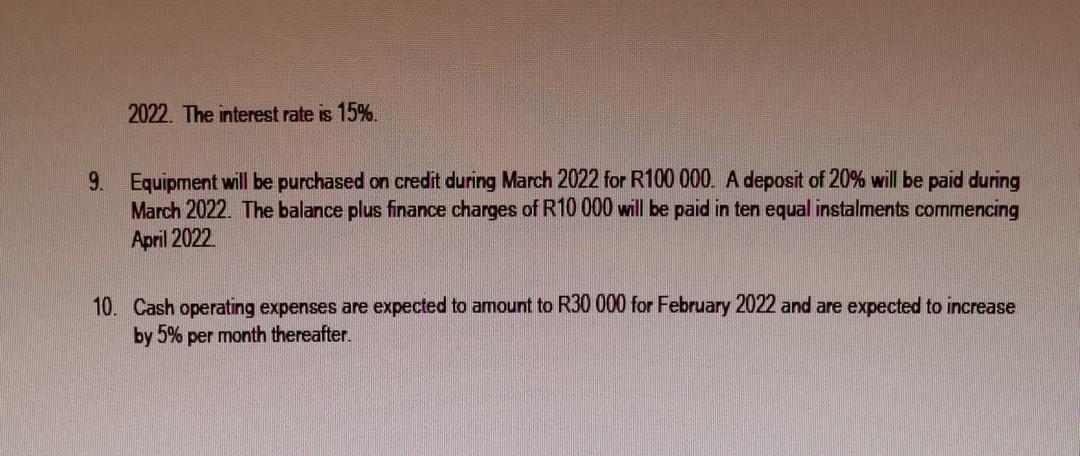

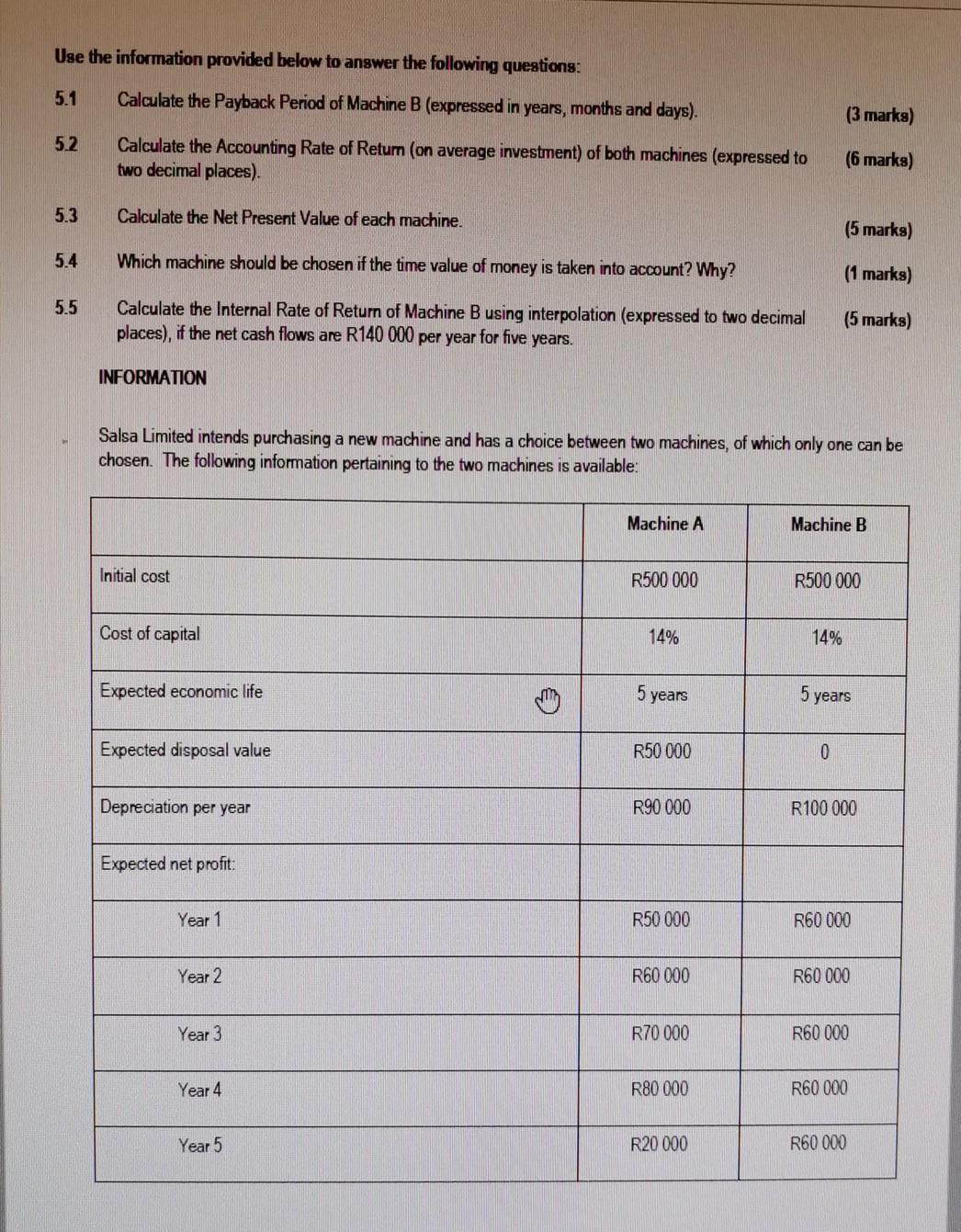

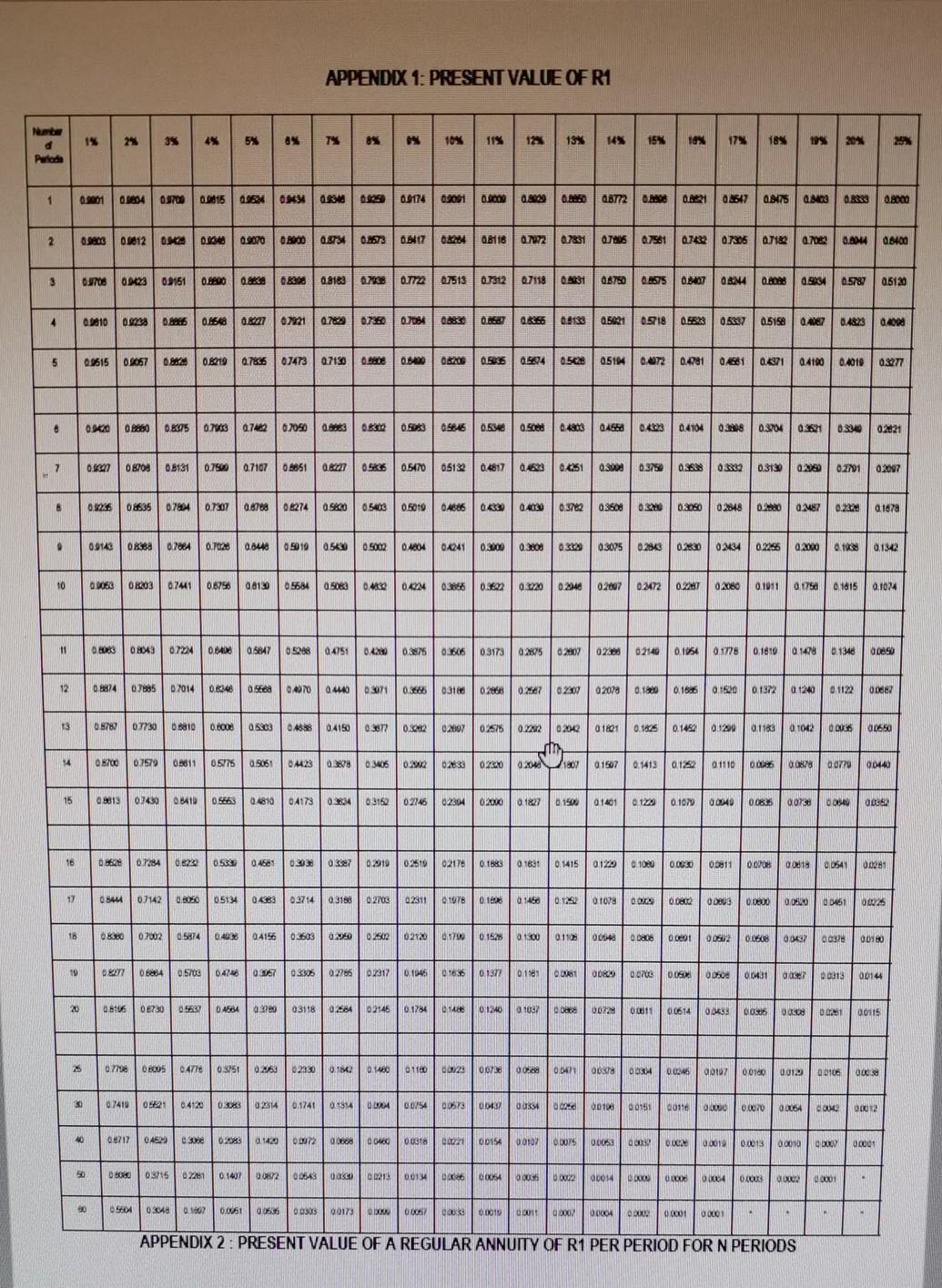

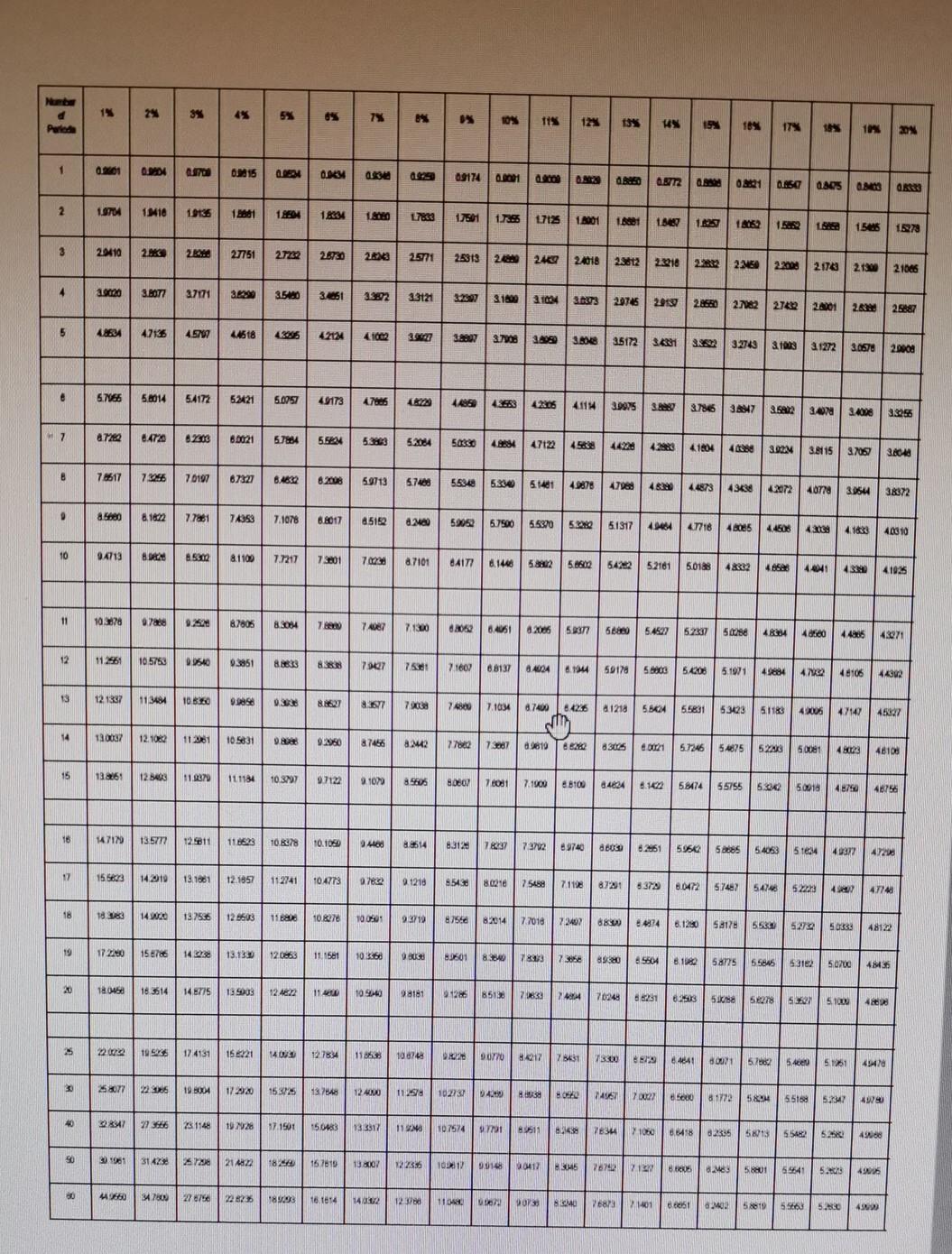

SECTION A [100 MARKS] Answer ALL the questions in this section. Use the information provided below to calculate the following variances. In each case state whether the variance is favourable or unfavourable. 1.1 Material quantity variance (3 marks) 1.2 Labour rate variance (3 marks) 1.3 Labour efficiency variance (3 marks) 1.4 Variable overheads efficiency variance (3 marks) 1.5 Variable overheads expenditure variance (3 marks) 16 Fixed overheads volume variance (3 marks) 1.7 Sales price variance (2 marks) INFORMATION Mica Manufacturers makes and sells a single product. The company operates a standard costing system. Details of the budgeted and actual data for 2022 are as follows: Budgeted data Standard production costs per unit: Direct materials 6 kg at a cost of R12 per kg Direct labour 3 hours at R10 per hour Variable overheads 3 hours at R5 per direct labour hour Fixed manufacturing overheads R180 000 Standard selling price R200 per unit Production and sales 10 000 units Actual data Direct materials 65 000 kg @ R13 per kg Direct labour 29 000 hours @ R11 per hour Variable overheads R130 500 Fixed manufacturing overheads R188 500 Selling price R195 Production and sales 10 000 units Prepare the Income Statement of Rotary Limited for the year ended 28 February 2021 using the following methods of costing: 2.1 Marginal costing (10 marks) 2.2 Absorption costing (10 marks) INFORMATION The following information was extracted from the accounting records of Rotary Limited for the year ended 28 February 2021 Inventory on 01 March 2020 Nil Production for the year 35 000 units Sales for the year 30 000 units Fixed costs: Manufacturing R700 000 Sales and administration R480 000 Variable costs per unit: Manufacturing R48 Sales and administration R12 Selling price per unit R150 Use the information provided below to answer the following questions: 3.1 Calculate the total Marginal Income and Net Profit (Loss). (4 marks) 32 Determine the break-even value using the marginal income ratio. (4 marks) 3.3 Use your answer from question 3.2 to calculate the break-even quantity. (1 marks) 3.4 Calculate the margin of safety (in units). (3 marks) 3.5 How many units must be sold to achieve a net profit of R756 000? (4 marks) 3.6 (4 marks) A decrease in the selling price of R10 per unit and a decrease in the fixed costs of R21 600 are expected to increase sales by 300 units. Will profitability improve? Motivate your answer. INFORMATION Temp Ltd manufactures toasters. The following information was extracted from the budget for the year ended 31 December 2022 Sales 5 400 units Selling price per toaster R270 Direct material cost per unit R70 Direct labour cost per unit R40 Variable manufacturing overheads cost per unit R16 Fixed manufacturing overheads cost R288 000 Variable selling and administrative costs per unit R36 Fixed selling and administrative costs R144 000 Use the information provided below to prepare the following for March and April 2022 4.1 Debtors Collection Schedule (4 marks) 42 Cash Budget (16 marks) INFORMATION The following forecasts have been made by the management team of FG Wholesalers: 1. The bank balance on 28 February 2022 is estimated to be R30 000 (unfavourable) 2. Budgeted sales (excluding discounts) for the first four months of 2022 are as follows: January February March April Cash sales R102 000 R114 000 R100 000 R80 000 Credit sales R115 000 R128 000 R105 000 R82 000 3. Customers who purchase for cash are entitled to a 10% cash discount Collections from credit sales are expected to be as follows. * 70% in the month after the sale; * 25% two months after the sale. 5% is usually written off as irrecoverable 4. Expected purchases for the first four months of 2022 are as follows: January February March April Cash purchases R55 000 R56 000 R50 000 R40 000 Credit purchases R60 000 R65 000 R60 000 R45 000 5. Creditors are paid in the month after the purchase. A discount of 5% is expected on 60% of these purchases. 6. The proprietor's fixed monthly drawings comprise 75% cash and 25% trading stock. The cost of the trading stock that the proprietor takes is R1 250 7 The monthly salaries amount to R50 000. Salaries will increase by 8% with effect from 01 April 2022 8. The last instalment on the loan, R4 000, as well as interest on loan for April 2022 will be paid at the end of April 2022. The interest rate is 15%. 9. Equipment will be purchased on credit during March 2022 for R100 000. A deposit of 20% will be paid during March 2022. The balance plus finance charges of R10 000 will be paid in ten equal instalments commencing April 2022 10. Cash operating expenses are expected to amount to R30 000 for February 2022 and are expected to increase by 5% per month thereafter. Use the information provided below to answer the following questions: 5.1 Calculate the Payback Period of Machine B (expressed in years, months and days). (3 marks) 5.2 Calculate the Accounting Rate of Return (on average investment) of both machines (expressed to two decimal places). (6 marks) 5.3 Calculate the Net Present Value of each machine. (5 marks) 5.4 Which machine should be chosen if the time value of money is taken into account? Why? (1 marks) 5.5 Calculate the Internal Rate of Return of Machine B using interpolation (expressed to two decimal places), if the net cash flows are R140 000 per year for five years. (5 marks) INFORMATION Salsa Limited intends purchasing a new machine and has a choice between two machines, of which only one can be chosen. The following information pertaining to the two machines is available: Machine A Machine B Initial cost R500 000 R500 000 Cost of capital 14% 14% Expected economic life mong 5 years 5 years Expected disposal value R50 000 0 Depreciation per year R90 000 R100 000 Expected net profit Year 1 R50 000 R60 000 Year 2 R60 000 R60 000 Year 3 R70 000 R60 000 Year 4 R80 000 R60 000 Year 5 R20 000 R60 000 APPENDIX 1: PRESENT VALUE OF R1 15 2% 35 * 7% 10% 11% 12 155 145 15% 18 17N 18% 1955 P 25 Paroda 1 1 2001 0164 0979 08015 098 00 or 09174 09001 0.000 0.20 0.20 08772 028 0221 08547 08 0903 08 0.800 2 0.9 0.5812 DSC 09070 0.20 0.87 0.857 09417 0424 08198 0.7272 0784 0745 0.791 07422 072 07122 0.7042 0.80 08400 3 Guns 09423 09161 00 00336 08183 ONS OT722 07513 07312 07118 0.831 08750 0.2575 0347 024 0.20 09:34 0.578 05120 4 0.9910 BETTO 0. 01648 OKT KIRCO 0.768 07260 0.7084 09890 016 0255 03133 05021 0.37180.5E13 05337 05158 0.4057 0.48.24 ROOVD 5 51550 29050 0.8210 0.766 07473 0.7150 0.080 OBO 02.00 cam 053609874 0.5228 05190.0072 0.4981 0/61 0371 04100 0.010 0277 . 0262002250 0505 07 0.7462 070503 0.0.08305646 0.5348 0.9088048773 0466 0.4323 0.4104 0288 03704 0:38 0.3340 02821 7 LOTO 0 870806131 0.79607107 05851 0.05% 0.5170 05132 0.4817 04623 042510 0.375 0.0332 031290380 0.21 02097 8 ONZE 08635 074 07307 0.8780 0627405620 05468 0.501004886 0233 0.4030 0.37 036000.00 02846 0.28 0.2287 0.2220 0.1678 6 0.0146 0888 07040.7028 0.6445 09010 05430 0.002 0.4604 04041 0.3000 ROWED 03075 02843 CERTO 0234 0.2255 0.2000 0108 CRID to 09090 OK203 0.741 06754 0.813005684 050630433 0404 0386 0.5 0.0 0.2948 0.2007 02072 CACCO 0.2800.1011 0.1788 0.1815 0.1024 11 0 0 0849 07224 0.840 056470528 0.4751 0.400 0.38 0.606 0.3173 0.287502007 028 02140 0.1054 0.1775 0.1810 0 1478 PRED Oce 12 08874 0.75 07014 0.04070 0.4440 0.3071 0.3 0316028 0227 026 02078 0.100.15001520 0.1372 0 1240 01122 ODBA 13 6.5780 07730 05810 0.0008 05803 04338 04150032 0.32 0.2807 0.125 0.1452 0.1220 01163 a 1042 OD 05920 02575 0.712 0.24201601 st 0x200 1207 0.1507 14 06/00 0.7579 0.0011 05775 0.8061 014423 0388 03106 0:22 0.2833 0.1413 0.1252 0.1110 0.00 0878 0.070 00440 15 0.8819 07430 06410 056630.4810 04173032403152 0.2345 02394 0.2000 1827 0.1990 LOVID 01229 0.107 00040 0.0835 007 DOSAU 00362 16 07284 00 05 04681 0.3938 0.37 0.2910 02510 02178 ORS 018 0 1415 0129 120 1020 0.000 0.0811 0.008 BLOO 0549 00281 17 0546 07142 00005134 0.4883 0.27140318802703 02311 RIAN 0.1 ON ISIO 0.1078 DO 0.0002 0800 0.00 0.00 ODASI OLAS 18 060 0.7002 058740.40 04156 03603 0.250 0250202120 617001501300 0.110 00048 BORDO O. DEDI DU 0.0608 00 ROOD 0010 10 URO OBA 05700 0411 1950 0.330502786 0731701045 01636 0.1977 0.1181 OBUS 6200 0.070 K500 POSCO 00431 DO 00013 00144 20 0.6106 08730 0.5632 DASA 0.3780 03118 0258402145 0.1784 RYD 01240 01037 OO 0024 00011 0.0614 OM DOLES OLUN 00115 25 OBODS 0.4770 0975 ON 02330 12 DIA 0110 0925 073 0 0.0 0021 /900 OBRA 00346 00107 00100 GIOD 00106 200 8 30 07410 08221 0.4120 OSORS 02814 0.1741 1914 DURA 00754 00573 OD 003 PROD 00103 19.00 00116 OR 0.0070 0.0064 NO 00012 40 08217 0450 0.30 02045 142000072 GBB O OWO 008 0001 00154 0.0102 OB075 0003 ED D.GE 00012 0.0013 0.0010 0.000 OL 05 0 0 03015 02281 0.1497 008200543 00213 001 D0000540200 000 00014 DON ko 00004 000 DIA 0.0001 . OF ORA RYOSO 0.1007 0.0051 005360030500173 600/ 00050 0 0000 00004 INICIO 100 0001 APPENDIX 2 : PRESENT VALUE OF A REGULAR ANNUITY OF R1 PER PERIOD FOR N PERIODS Numbe d Perlede 24 3% 5% 65 7% * 105 115 12% 13% H 19% 16% 17% % 10% 20 1 0401 0. 0915 2004 01234 0834 0979 09174 0.0001 246002 A02210850 000 ONS OR 2 1.9704 11110 19135 12881 1250 1634 180 L783 17561 17125 14001 11 184871835 18152 1521 155 1978 3 20410 2. 27751 27222 28730 26X3 2571 25313 2000 240 24018 2382 23218228222260 2200 2.172 2120 21066 4 2.9020 3.8077 27171 3.60 3560 32851 3382 33121 3/2007 318231034 373 207462913 2.850 2182278224201 283 25887 12% 5 46 47136 45701 4618 4085 42124 41002 3.1997 37000 3.4050 38 15172 34331 352 32743 1013 21272 3.0578 20008 5.766 SOL SAT 52421 50014 54172 52421 5.0757 49173 4706 4485 43852805 4.1143.9975 38 3.786 38947 SA 3.0 2.4028 3.82% 7 87262 8.4720 62305 8.0021 57884 5.56 5363 5208A 50330 48684 47122 456384422 423 41604 488 3008 3.8115 3708 3.600 8 7.617 76066 70197 87327 8.4632 59713 67488 55348 5334514614.9878 479884828 4.48734343 1272407783954 38372 de &1802 7781 74353 7.1078 6.8017 85152 81 552 6.7900553705 51317424 47718 46085 4.4608 Aey 41633 40010 10 10 94713 B. 8530 81100 7.7217 7.3801 70231 87101 BAT76.1468 5.88.2 5.802 542252161 50188 48332 4863 4.0041 41025 11 1078 0.78 9.2528 87805 8.3054 7 74087 71500 XO 0.4051 8.2006 5377 668 5.4522 5.2337 5.se 48834 40 4485 1207 12 112951 165753 0.0540 0.3851 8.88 BER 70427 75: 71607 88137 8.4024 6.124450178 500 5.4208519149884 47 40106 443W 13 12 1337 113484 TE 0.00 OR 8862 700 7. 7.1034 8.7400 8.42 81218554 558315342351183 4206 47140 48227 14 120037 12.10% 11261 105831 98 02950 87466 22 77842 73607 8.98108 83025 80021 5.724654895 52833 50081 480 48100 15 13261 12 463 11.2370 111184 10.397 7122 9.1073 BOS BOCO 76031 7.1900 68100 84A 0.142 58474 55755 530 60218 4878 48750 18 1471 13.5777 EX 2011 OBS 0.16 12011 11 8623 108378 10.1060 Med 88614 83120 7837 73702 8.9740 GBU 62051 5956 52005 54063 5ten 42322 720 17 155623 14919 13.1001 12.1857 112741 10.4773 19782 1210 55430 80210 7545871198 87291 83728.0472 57462 5446 5233 47740 18 18 14 WAO 197556 125633 11880 10.8218 10.00 937 87564 8.2014 77018 7.2002 884874 8.1280 5812 550 527.0 50333 481222 19 1720 158706 1403 13.130 12063 11.1581 10 550 0 0 83301 82 7813 2.05 B20 65604 81982 58775 5562563182 50200 484 2 20 180458 16.3514 14.8775 13003 12.48.22 11 100 08181 1296 851 23 WA 70048 60231 8203 558278 60 5100 480 25 22.000 19 EXE 174131 15321 1403 127834 11888 10.87 20 907708217 7431 70 89 8440 800 5786 5.40 5.7251 45478 58077 22.06 19.00 17:2920 153725 13.748 12 000 1128 102231 DA 83 MA670022 Beco 81772 589 5516 52347 *W 40 2247 223666 23.1148 19 1928 17. 1501 50483 13 3317 11 WMO 10.7574 8.511 BKSH 2634 1080 8.6418 02336 58015 55482 5.25 4318 90 1981 31.43 257238 214322 180 157610 13.02 12236 1012 0417 B35 2821 B. Me 5801 6641 5.6 496 00 4400 34.7800 22 22826 1899 16.1614 140/2 12.30 110. Dee 90733 SMO 68 1401 0.685 8 MB 58810 5563 5. 41Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Valuation For Accountants A Short Course Based On IFRS

Authors: Stephen Lynn

1st Edition

9811503567, 9789811503566