Answered step by step

Verified Expert Solution

Question

1 Approved Answer

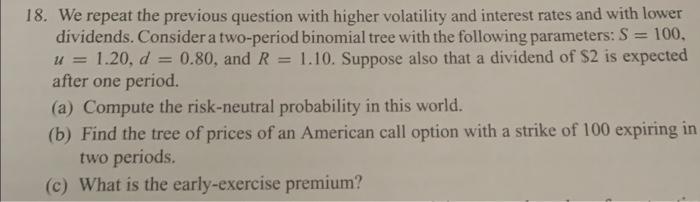

PLEASE USE EXCEL TO ANSWER 18. We repeat the previous question with higher volatility and interest rates and with lower dividends. Consider a two-period binomial

PLEASE USE EXCEL TO ANSWER

18. We repeat the previous question with higher volatility and interest rates and with lower dividends. Consider a two-period binomial tree with the following parameters: S = 100. u = 1.20, 0.80, and R. 1.10. Suppose also that a dividend of $2 is expected after one period. (a) Compute the risk-neutral probability in this world. (b) Find the tree of prices of an American call option with a strike of 100 expiring in two periods. (c) What is the early-exercise premium Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Budget Building Book For Nonprofits

Authors: Murray Dropkin, Jim Halpin, Bill La Touche

2nd Edition

0787996033, 978-0787996031