Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE USE EXCEL TO ANSWER Here is the information from #26 27. Using the same information as in Question 26, calculate the following quantities: (a)

PLEASE USE EXCEL TO ANSWER

Here is the information from #26

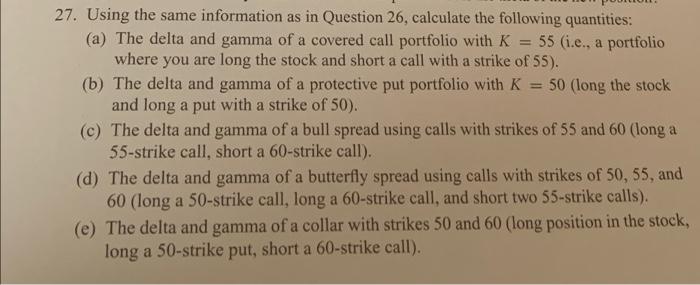

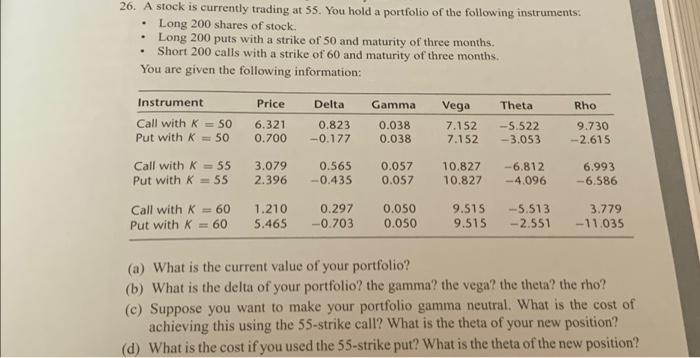

27. Using the same information as in Question 26, calculate the following quantities: (a) The delta and gamma of a covered call portfolio with K 55 (i.e., a portfolio where you are long the stock and short a call with a strike of 55). (b) The delta and gamma of a protective put portfolio with K 50 (long the stock and long a put with a strike of 50). (c) The delta and gamma of a bull spread using calls with strikes of 55 and 60 (long a 55-strike call, short a 60-strike call). (d) The delta and gamma of a butterfly spread using calls with strikes of 50, 55, and 60 (long a 50-strike call, long a 60-strike call, and short two 55-strike calls). (e) The delta and gamma of a collar with strikes 50 and 60 (long position in the stock, long a 50-strike put, short a 60-strike call). a 26. A stock is currently trading at 55. You hold a portfolio of the following instruments: Long 200 shares of stock. Long 200 puts with a strike of 50 and maturity of three months. Short 200 calls with a strike of 60 and maturity of three months. You are given the following information: Instrument Delta Theta Call with K = 50 Put with K = 50 Price 6.321 0.700 0.823 -0.177 Gamma 0.038 0.038 Vega 7.152 7.152 -5.522 -3.053 Rho 9.730 -2.615 Call with K = 55 Put with K = 55 3.079 2.396 0.565 -0.435 0.057 0.057 10.827 10.827 -6.812 -4.096 6.993 -6.586 Call with K = 60 Put with K = 60 1.210 5.465 0.297 -0.703 0.050 0.050 9.515 9.515 -5.513 -2.551 3.779 - 11.035 (a) What is the current value of your portfolio? (b) What is the delta of your portfolio? the gamma? the vega? the theta? the rho? (c) Suppose you want to make your portfolio gamma neutral. What is the cost of achieving this using the 55-strike call? What is the theta of your new position? (d) What is the cost if you used the 55-strike put? What is the theta of the new position? 27. Using the same information as in Question 26, calculate the following quantities: (a) The delta and gamma of a covered call portfolio with K 55 (i.e., a portfolio where you are long the stock and short a call with a strike of 55). (b) The delta and gamma of a protective put portfolio with K 50 (long the stock and long a put with a strike of 50). (c) The delta and gamma of a bull spread using calls with strikes of 55 and 60 (long a 55-strike call, short a 60-strike call). (d) The delta and gamma of a butterfly spread using calls with strikes of 50, 55, and 60 (long a 50-strike call, long a 60-strike call, and short two 55-strike calls). (e) The delta and gamma of a collar with strikes 50 and 60 (long position in the stock, long a 50-strike put, short a 60-strike call). a 26. A stock is currently trading at 55. You hold a portfolio of the following instruments: Long 200 shares of stock. Long 200 puts with a strike of 50 and maturity of three months. Short 200 calls with a strike of 60 and maturity of three months. You are given the following information: Instrument Delta Theta Call with K = 50 Put with K = 50 Price 6.321 0.700 0.823 -0.177 Gamma 0.038 0.038 Vega 7.152 7.152 -5.522 -3.053 Rho 9.730 -2.615 Call with K = 55 Put with K = 55 3.079 2.396 0.565 -0.435 0.057 0.057 10.827 10.827 -6.812 -4.096 6.993 -6.586 Call with K = 60 Put with K = 60 1.210 5.465 0.297 -0.703 0.050 0.050 9.515 9.515 -5.513 -2.551 3.779 - 11.035 (a) What is the current value of your portfolio? (b) What is the delta of your portfolio? the gamma? the vega? the theta? the rho? (c) Suppose you want to make your portfolio gamma neutral. What is the cost of achieving this using the 55-strike call? What is the theta of your new position? (d) What is the cost if you used the 55-strike put? What is the theta of the new position Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: Gary E. Gibbons, Robert D. Hisrich, Carlos Marques DaSilva

1st Edition

1452274177, 978-1452274171