Answered step by step

Verified Expert Solution

Question

1 Approved Answer

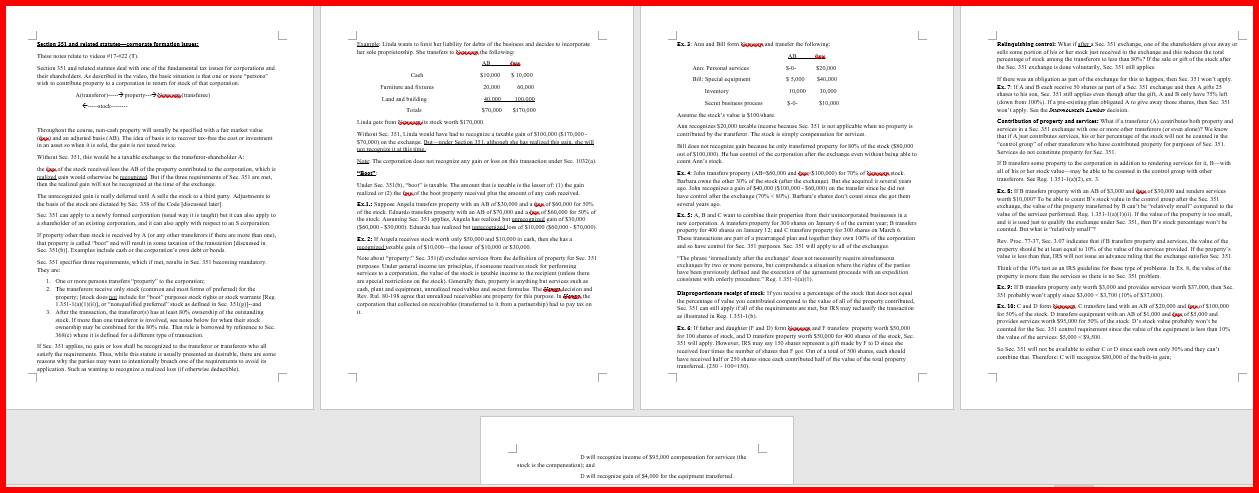

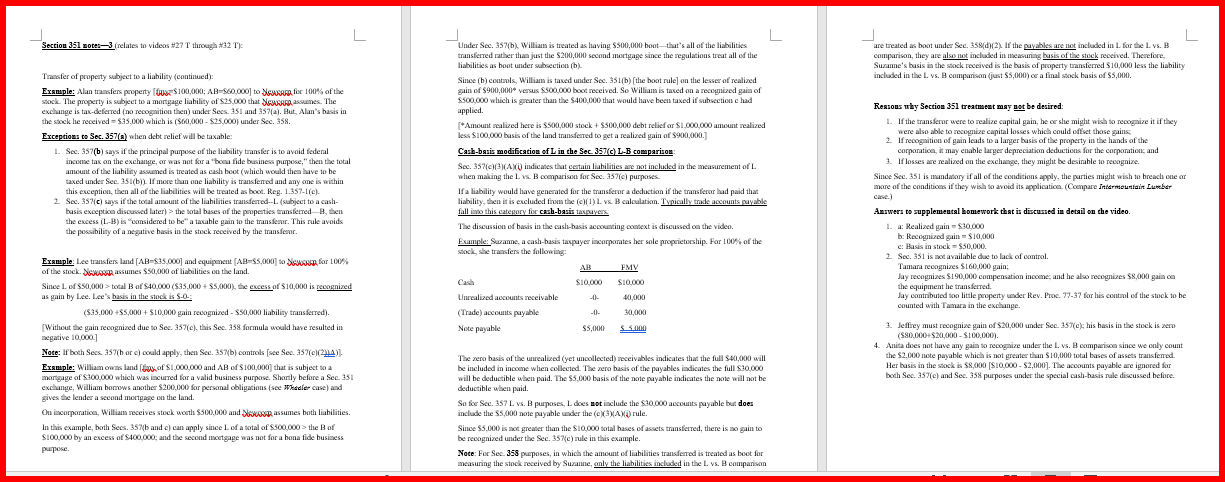

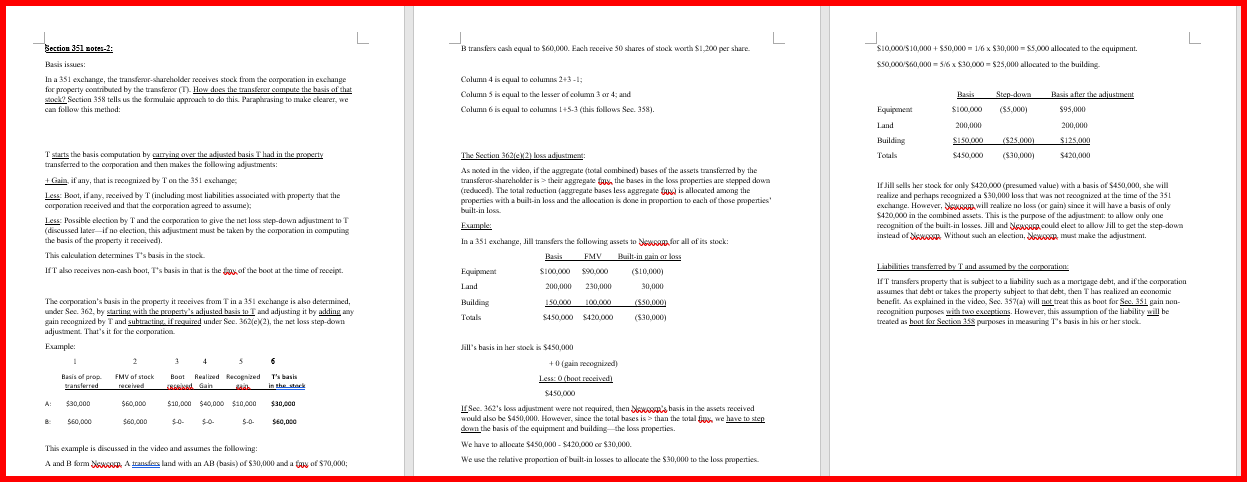

Please use tax section 351 note, according to instruction above, write 5 pages project. Thanks! Secrion 351 noter-2: B transfers cash equal to $60,000. Fach

Please use tax section 351 note, according to instruction above, write 5 pages project. Thanks!

Secrion 351 noter-2: B transfers cash equal to $60,000. Fach receive 30 shares of stock woeth $1,200 per share \$10,0001\$10,000 +$50,000=1/6$30,000=$5,000 allocased to the equipment. Basis issues: $50,0005600,000=516$30,000=$25,000 allocated to the building. In a 351 exchange, the transferor-shureholder receives stock frou the compocation in exchange Column 4 is equal to columus 2+31; for property contributed by the transferoe (1). How does the transferor compute the basis of that siock? Section 358 tells us the formulaic approach to do this. Paraphrasing to make clearer, we Column 5 is equal to the lesser of colurnn 3 or 4 ; and sack? Section 358 tells Column 6 is equal to columus 1+53 (this follows Sec. 358). T starts the basis computation by camving over the adjusted basis T had in the property trinsferred to the comporation and then makes the following adjustmens: The Section 362(1) (e) 2 loss adjustment: + Gain, if any, that is recognized by T ou the 351 evehange As sosed in the video, if the aggregate (tocal combized) bases of the assets transferred by the If Jill sells her stock for ouly $420,000 (presumed value) with a basis of $450,000, she will Less: Boot, if ayy, received by T (including usost liabilities asseciated with property that the transferar-shareholder is > their aggregase frow the bases in the lose peoperties are sicepped do (redaced). The sotal reduction (aggresate bases less aggregate forv) is allocated among the realize and perhaps recognized a 530,000 loss that was not recognized at the time of the 35 corponation received and that the corporation agreed to assume), properties w exchange. However, Noword will realize no loss (or gain) since it will have a basis of onl $420,000 in the combined assets. This is the purpose of the adjustment: to allow only oue Less: Possible election by T and the corponation to give the net loss step-down adjustment to T (discussed laser- if no clection, this adjustment must be taken by the comporation in eomputing recognition of the built-in losses. Jill and Nerprep could elect to allow Jill to get the step-dowa the basis of the property it reoeived). In a 351 exchange, Jill transfers the following assets io Neworqu for all of is stock: instead of Neroen Without sach a election, Noroen most make the adjustment. This calculation determines T+s basis in the stock. If T also receives non-cash boot, T+s busis in that is the ferh of the boot at the time of receipt. Liabilities tranefenod by T and assumed by the carsocation: If T transfers porperty that is subject to a liahility such as a mortgage debt, and if the compocation assumses that debt or takes the property subject to that debt, then T has realized an eomomic. The coporation's basis in the peoperty it receives from T in a 351 exchange is also desermined. benefit. As explained in the video, Sec. 357(a) will not treat this as boot for Sec. 351 gain nom- gain recognized by T and subtrating, if reouined under Sec. 362(e) (2), the net loss step-down recognition purposes with two exceptions. However, this assumption of the liability will be treased as boot for Section 358 perposes in useacaring T's basis in his or her stock adjustaneat. That's it for the corporation. Framinia Jill's basis in her siock is $450,000 If Sec. 362 's loss adjustmeat were not required. then, Wrwoome's basis in the assets received This example is discussed in the video and assumes the following: We have to allocate $450,000 - $420,000 or $30.000. A and B form Jorresen A transfex land with an AB (basis) of $30,000 and a foly of $70,000; We we the relative proportion of built-in lesses to allocase the 530,000 to the loss peoperties. This assignment should help you practice putting tax ideas and specific content into a clear, professional written format. Styles for such "memoranda" can vary according to the context and purpose of the project. You are to write a research paper that develops and explains in a clear, coherent manner, any tax topic that is covered in this course. I don't want a mere rewrite of my notes. I Would like you to narrow a topic from the broader topics we study and develop it in your own words. Just imagine if you were working in an accounting firm, and your supervisor or manager/partner asked you to write a memo on an appropriate tax topic to refresh his or her understanding of the issues involved. The paper should contain specific references to appropriate Code and Reg sections, any rulings or cases that are relevant, and any other citations. You may use any source to accomplish this including other materials on the QC Library's database, other textbooks or articles, etc. You must, however, give proper credit in footnotes for any source you quote or paraphrase. The citation should be clear. If it is a case, give the main name and citation found in Checkpoint. If possible, the paper should include a reference to some relatively recent development such as a new ruling or case on your topic. You can use the Citator to check for sources that refer to a source you already have. You can also search Checkpoint databases including a key word search. Length: The paper should be at least five (5) double-spaced typed pages, but not longer than 10 pages. Don't say more than you need to say. Use common sense and keep it straightforward. Also, use standard fonts and margins. Due Date: The paper is due by our last Zoom meeting in May. Secrion 351 noter-2: B transfers cash equal to $60,000. Fach receive 30 shares of stock woeth $1,200 per share \$10,0001\$10,000 +$50,000=1/6$30,000=$5,000 allocased to the equipment. Basis issues: $50,0005600,000=516$30,000=$25,000 allocated to the building. In a 351 exchange, the transferor-shureholder receives stock frou the compocation in exchange Column 4 is equal to columus 2+31; for property contributed by the transferoe (1). How does the transferor compute the basis of that siock? Section 358 tells us the formulaic approach to do this. Paraphrasing to make clearer, we Column 5 is equal to the lesser of colurnn 3 or 4 ; and sack? Section 358 tells Column 6 is equal to columus 1+53 (this follows Sec. 358). T starts the basis computation by camving over the adjusted basis T had in the property trinsferred to the comporation and then makes the following adjustmens: The Section 362(1) (e) 2 loss adjustment: + Gain, if any, that is recognized by T ou the 351 evehange As sosed in the video, if the aggregate (tocal combized) bases of the assets transferred by the If Jill sells her stock for ouly $420,000 (presumed value) with a basis of $450,000, she will Less: Boot, if ayy, received by T (including usost liabilities asseciated with property that the transferar-shareholder is > their aggregase frow the bases in the lose peoperties are sicepped do (redaced). The sotal reduction (aggresate bases less aggregate forv) is allocated among the realize and perhaps recognized a 530,000 loss that was not recognized at the time of the 35 corponation received and that the corporation agreed to assume), properties w exchange. However, Noword will realize no loss (or gain) since it will have a basis of onl $420,000 in the combined assets. This is the purpose of the adjustment: to allow only oue Less: Possible election by T and the corponation to give the net loss step-down adjustment to T (discussed laser- if no clection, this adjustment must be taken by the comporation in eomputing recognition of the built-in losses. Jill and Nerprep could elect to allow Jill to get the step-dowa the basis of the property it reoeived). In a 351 exchange, Jill transfers the following assets io Neworqu for all of is stock: instead of Neroen Without sach a election, Noroen most make the adjustment. This calculation determines T+s basis in the stock. If T also receives non-cash boot, T+s busis in that is the ferh of the boot at the time of receipt. Liabilities tranefenod by T and assumed by the carsocation: If T transfers porperty that is subject to a liahility such as a mortgage debt, and if the compocation assumses that debt or takes the property subject to that debt, then T has realized an eomomic. The coporation's basis in the peoperty it receives from T in a 351 exchange is also desermined. benefit. As explained in the video, Sec. 357(a) will not treat this as boot for Sec. 351 gain nom- gain recognized by T and subtrating, if reouined under Sec. 362(e) (2), the net loss step-down recognition purposes with two exceptions. However, this assumption of the liability will be treased as boot for Section 358 perposes in useacaring T's basis in his or her stock adjustaneat. That's it for the corporation. Framinia Jill's basis in her siock is $450,000 If Sec. 362 's loss adjustmeat were not required. then, Wrwoome's basis in the assets received This example is discussed in the video and assumes the following: We have to allocate $450,000 - $420,000 or $30.000. A and B form Jorresen A transfex land with an AB (basis) of $30,000 and a foly of $70,000; We we the relative proportion of built-in lesses to allocase the 530,000 to the loss peoperties. This assignment should help you practice putting tax ideas and specific content into a clear, professional written format. Styles for such "memoranda" can vary according to the context and purpose of the project. You are to write a research paper that develops and explains in a clear, coherent manner, any tax topic that is covered in this course. I don't want a mere rewrite of my notes. I Would like you to narrow a topic from the broader topics we study and develop it in your own words. Just imagine if you were working in an accounting firm, and your supervisor or manager/partner asked you to write a memo on an appropriate tax topic to refresh his or her understanding of the issues involved. The paper should contain specific references to appropriate Code and Reg sections, any rulings or cases that are relevant, and any other citations. You may use any source to accomplish this including other materials on the QC Library's database, other textbooks or articles, etc. You must, however, give proper credit in footnotes for any source you quote or paraphrase. The citation should be clear. If it is a case, give the main name and citation found in Checkpoint. If possible, the paper should include a reference to some relatively recent development such as a new ruling or case on your topic. You can use the Citator to check for sources that refer to a source you already have. You can also search Checkpoint databases including a key word search. Length: The paper should be at least five (5) double-spaced typed pages, but not longer than 10 pages. Don't say more than you need to say. Use common sense and keep it straightforward. Also, use standard fonts and margins. Due Date: The paper is due by our last Zoom meeting in May

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Auditing An Introduction to International Standards on Auditing

Authors: Rick Hayes, Philip Wallage, Hans Gortemaker

3rd edition

273768174, 978-0273768173