Please write a conclusion with the business case given below.

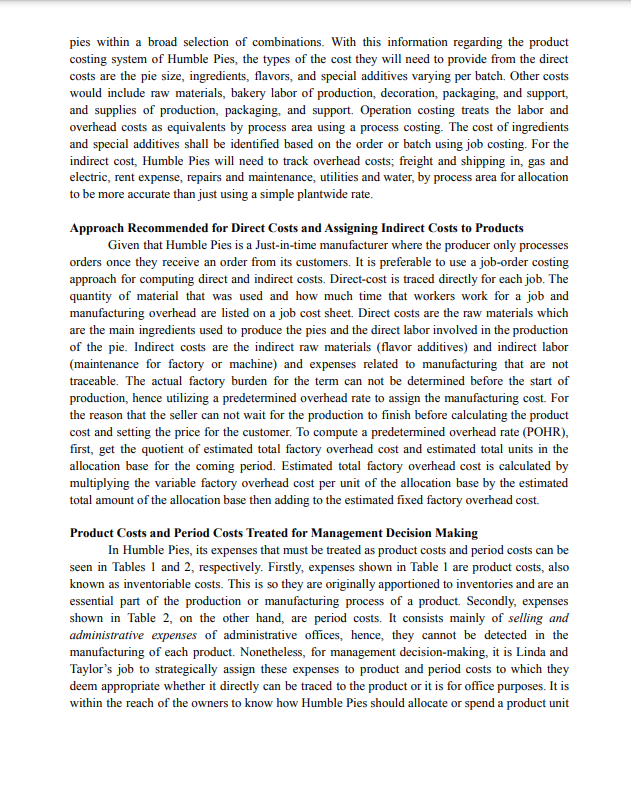

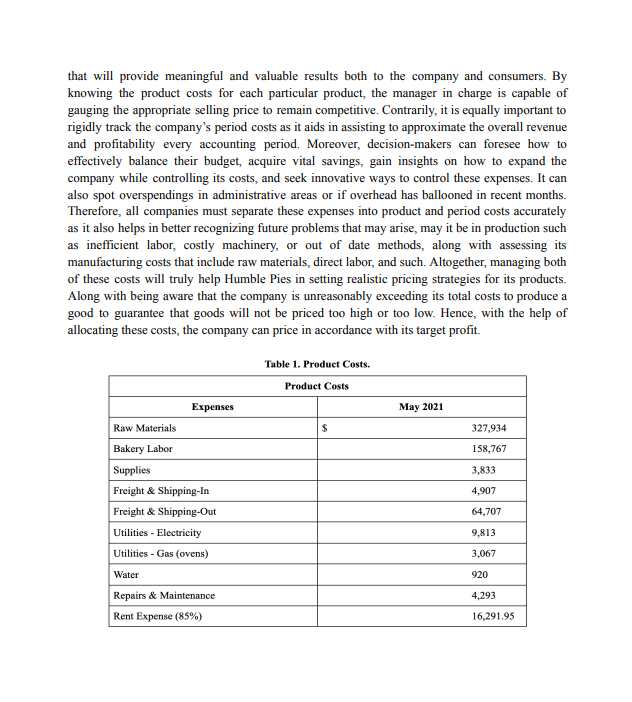

Introduction Humble Pies, from the name itself, started from a humble beginning without great expectations their company would turn out to be flourishing in the food industry. It started in the year 2015 when the owners, Linda Jackson, and Taylor Johnson, reunited after living their own separate lives for years. Henceforth, they found out how their passion and dedication in crafting multiple delectable desserts never faded away. Therefore, they decided to partner up and build Humble Pies that consists of mainly selling high-quality delightful pies that vary according to the size, filling, packaging, flavors, and other factors. Moreover, Humbles Pies was surprisingly thriving in the industry over the months, and demand was growing. Moreso, Linda, and Taylor decided to hire more workers by employing a controller that can guide them through the process of maintaining the long-term profitability of Humble Pies. Years later, they pursue expanding their operations by producing ready-made pies to be distributed to suppliers. Afterward, suppliers' jobs will sell these goods to different platforms such as foodservice applications, supermarkets, bakery shops, and groceries to reach a wider and untapped market. With the effective and innovative strategy of dispersing their products to suppliers and markets, they were able to reach a spectacular total amount of revenue of $6.1 million in the year 2020. High customer satisfaction with heartening feedback is brought by the owner's constant innovation of curating unique desserts through the use of healthy alternative ingredients and their area of expertise. Along the way, they began to incrementally increase their productions and staff to ensure the smooth running of Humble Pies. As their business grows tremendously, the managers systematically handle their workers through the labor reports. However, this caused some inconsistencies internally in the company as they are unsure of how to distribute equal overhead or indirect costs to every quantity produced. Therefore, the owners of Humble Pies are looking for a strategic yet convenient and inexpensive way to develop a course of action on how to track the labor hours of each worker in each unit produced to ensure that every cost is accounted for. Information Needed Humble Pies, Inc. needs information such as the different cost systems in order to operate different types of pies since the business does not only produce a single type of pie thus needing accurate decision making that relates to the pricing, special orders, and product offerings of the company. Types of Cost Information Humble Pies' Product Costing System should Provide Based on Humble Pies' needs, the types of cost information Humble Pies production costing system should provide are the following. The company competes through a differentiation strategy based on a variety of flavors and packaging. Due to its differentiation strategy, Humble Pies will need a cost system that can handle various pies for decisions associated with pricing, product offerings, and special orders. Since these pies go through nearly the same production process, the cost system does not need to track the specific labor and overhead per individual pie or order. Henceforth, a strategic plan for an innovative cost system would be to deliver accurate and reliable product costs per particular order request and varyingpies within a broad selection of combinations. With this information regarding the product costing system of Humble Pies, the types of the cost they will need to provide from the direct costs are the pie size, ingredients, flavors, and special additives varying per batch. Other costs would include raw materials, bakery labor of production, decoration, packaging, and support, and supplies of production, packaging, and support. Operation costing treats the labor and overhead costs as equivalents by process area using a process costing. The cost of ingredients and special additives shall be identified based on the order or batch using job costing. For the indirect cost, Humble Pies will need to track overhead costs; freight and shipping in, gas and electric, rent expense, repairs and maintenance, utilities and water, by process area for allocation to be more accurate than just using a simple plantwide rate. Approach Recommended for Direct Costs and Assigning Indirect Costs to Products Given that Humble Pies is a Just-in-time manufacturer where the producer only processes orders once they receive an order from its customers. It is preferable to use a job-order costing approach for computing direct and indirect costs. Direct-cost is traced directly for each job. The quantity of material that was used and how much time that workers work for a job and manufacturing overhead are listed on a job cost sheet. Direct costs are the raw materials which are the main ingredients used to produce the pies and the direct labor involved in the production of the pie. Indirect costs are the indirect raw materials (flavor additives) and indirect labor (maintenance for factory or machine) and expenses related to manufacturing that are not traceable. The actual factory burden for the term can not be determined before the start of production, hence utilizing a predetermined overhead rate to assign the manufacturing cost. For the reason that the seller can not wait for the production to finish before calculating the product cost and setting the price for the customer. To compute a predetermined overhead rate (POHR), first, get the quotient of estimated total factory overhead cost and estimated total units in the allocation base for the coming period. Estimated total factory overhead cost is calculated by multiplying the variable factory overhead cost per unit of the allocation base by the estimated total amount of the allocation base then adding to the estimated fixed factory overhead cost. Product Costs and Period Costs Treated for Management Decision Making In Humble Pies, its expenses that must be treated as product costs and period costs can be seen in Tables 1 and 2, respectively. Firstly, expenses shown in Table 1 are product costs, also known as inventoriable costs. This is so they are originally apportioned to inventories and are an essential part of the production or manufacturing process of a product. Secondly, expenses shown in Table 2, on the other hand, are period costs. It consists mainly of selling and administrative expenses of administrative offices, hence, they cannot be detected in the manufacturing of each product. Nonetheless, for management decision-making, it is Linda and Taylor's job to strategically assign these expenses to product and period costs to which they deem appropriate whether it directly can be traced to the product or it is for office purposes. It is within the reach of the owners to know how Humble Pies should allocate or spend a product unitthat will provide meaningful and valuable results both to the company and consumers. By knowing the product costs for each particular product, the manager in charge is capable of gauging the appropriate selling price to remain competitive. Contrarily, it is equally important to rigidly track the company's period costs as it aids in assisting to approximate the overall revenue and profitability every accounting period. Moreover, decision-makers can foresee how to effectively balance their budget, acquire vital savings, gain insights on how to expand the company while controlling its costs, and seek innovative ways to control these expenses. It can also spot overspendings in administrative areas or if overhead has ballooned in recent months. Therefore, all companies must separate these expenses into product and period costs accurately as it also helps in better recognizing future problems that may arise, may it be in production such as inefficient labor, costly machinery, or out of date methods, along with assessing its manufacturing costs that include raw materials, direct labor, and such. Altogether, managing both of these costs will truly help Humble Pies in setting realistic pricing strategies for its products. Along with being aware that the company is unreasonably exceeding its total costs to produce a good to guarantee that goods will not be priced too high or too low. Hence, with the help of allocating these costs, the company can price in accordance with its target profit. Table 1. Product Costs. Product Costs Expenses May 2021 Raw Materials $ 327,934 Bakery Labor 158,767 Supplies 3,833 Freight & Shipping-In 4,907 Freight & Shipping-Out 64.707 Utilities - Electricity 9.813 Utilities - Gas (ovens) 3,067 Water 920 Repairs & Maintenance 4.293 Rent Expense (85%) 16,291.95Table 2. Period Costs. Period Costs Expenses May 2021 Administration Salaries $ 41,367 Rent Expense (15%) 2,875.05 Telephone & Internet 2,300 Co-owner's Salary 25,300 Broker's Commissions 30.667 Product Cost Tracking Once an order or project has been approved, tracking costs for each product is essential to ensure accuracy as it provides an understanding of the overall financial performance of the business. Products can be identified by product type, batch, a specific job, operations, activity, and the like. First, to track the cost of raw materials, it would be tracked by product type. Raw materials are separated into main ingredients and flavor additives; thus are divided into two categories which are direct cost and indirect cost. Main ingredients such as eggs, flour, sugar, nuts, and fruit should be tracked by direct costs of the raw materials because these ingredients can be traced directly to the production of pies. Meanwhile, flavor additives such as salt, dyes, spices, and certain oils are indirect costs of the raw materials because they cannot be easily traced to the production of pies. Second, to track the cost of bakery labor for the production line, it would be tracked by operation. The production line includes mixing, filling, and baking which are sequential steps in producing the pies. The packaging is tracked by batch or product type. Humble Pies has several different varieties of pies produced and each pie will have different sizes thus affecting the packaging. The pies produced should correspond with its packaging, it cannot be uniform for all of its varieties of pies. Then, sanitation and warehouse, which are included as part of the cost of goods sold, should be tracked by support labor since these are the support line that provides the cleanliness, storage, and space for the products that Humble Pies produced which will be shipped and sold. Third, supplies can be tracked by operation because these are the items that are used daily in the operation of Humble Pies. These are further separated into production, packaging and decorating, sanitation, and warehouse. Supplies on the production line such as mixers and ovens are tracked for production supplies. Supplies on the packaging and decorating are tracked by packaging supplies which include items such as pastry bags, icing pens, spatulas, and the like. Moreover, sanitation and warehouse are tracked by supportive supplies. These supplies are used for the cleanliness, storage, and space for the pies that are being produced and ready for shipment. Lastly, overhead costs such as freight shipping-in, electricity and gas utilities, water, repair and maintenance, and rent expenses are tracked by other overhead costs. To further classify them, freight-ins are tracked by rawmaterials since these materials are used for production and are part of the cost of goods sold. Meanwhile, electricity and gas utilities, water, repair and maintenance, and rent expenses are tracked by production costs and administrative costs (for utilities and rent). These costs are not directly traceable to the production of the pies and it does not change whether Humble Pies will generate revenue or not. Assigned Costs to Products The specific cost items that are listed above should be sensible and rational in order to achieve reasonably accurate product costs. Whether to compute it by standard costs, using an allocation base, or tracing it specifically to order, it should always be reasonable because these costs help the business in generating the financial statements. Since actual costs are typically known after the production of goods is finished, using these estimates will provide an approximation of what the job or order is likely to cost. Raw materials, which include both main ingredients and flavor additives, use standard costs to assign costs to its products. Meanwhile, direct cost per unit is used for the bakery labor for production and decoration, and packaging, wherein the price is fixed. On the other hand, bakery labor for sanitation and warehouse assigned its product costs based on the weight or labor hours. Next, supplies used for products such as mixers and ovens are based on production hours. Supplies used in packaging and decorating such as pastry bags, icing tips, and icing pens are based on the packaging hours. Supplies used in sanitation and warehouse are based on weight or labor hours. Moreover, other overhead costs such as freight and shipping-ins assigned product costs based on material costs since this deals with the cost of manufacturing a certain product. Lastly, electricity and gas utilities are used for production equipment, water, repair and maintenance, and rent expenses that are under other overhead costs, assigned product costs based on weight or labor hours