Please write if 1st statement is true or false

and same with 2nd statement. thank you

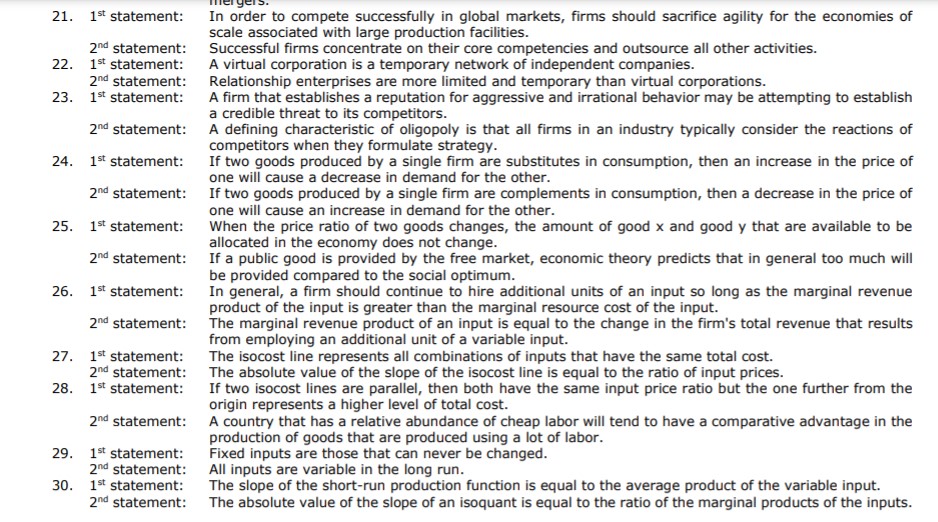

21. 22. 23. 24. 25. 26. 27. 23. 29. 30. 1it statement: 2"ll statement: 15t statement: 2\"\" statement: 1'It statement: 2"ll statement: 1"t statement: 2'\"1 statement: 1" statement: 2"ll statement: 19't statement: 2'\"1 statement: 19't statement' 2"\" statement: 1" statement: 2"ll statement: 1" statement: 2'\"1 statement: 1" statement: 2""l statement: "law:- In order to compete successfully In global markets, fins shoidd sacrice agility for the economies of scale associated with large production fadities. Successful firms concentrate on their core competendes and outsource all other activl'tl. A virtual corporation is a temporary network of independent companies. Relationship enterprises are more limited and temporary than virtual corporations. A firm that establishes a reputation for aggressive and hationaI behavior may be attempting to establish a credible threat to its competitors. A dening characteristic of oligopoly is that all fins in an industry typically consider the reactions of competitors when they formulate strategy. If two goods produced by a single iin'n are substitutes In consumption. than an increase in the price of one will cause a decrease in demand for the other. If two goods produced by a single rm are complements in consumption. then a decrease in the price of one will cause an increase In demand for the other. When the price ratio of two goods changes. the amount of good it and good 1; that are available to be allocated In the economy does not change. If a public good is provided by the free market, economic theory predicts that In general too much will be provided compared to the social optimum. In general, a firm should condone to hire additional units of an input so long as the marginal revenue product of the Input is greater than the marginal resource cost of the input. The marginal revenue product of an input is equal to the change in the rm's total revenue diet results from employing an additional unit of a variable input. The isocost line represents all combinations of Inputs that have the same total cost. The absolute value of the slope of the isocost line Is equal to the ratio of Input prices. If trivo isocost lines are parallel, then both have the same input price ratio but the one further from the origin represents a higher level of total cost. A couritw that has a relative abundance of cheap labor will tend to have a comparative advantage in the production of goods that are produced using a lot of labor. Fixed inputs are those that can never be changed. All inputs are variable in the long run. The slope of the short-run production function Is equal to the average product of the variable Input. The absolute value of the slope of an isoquant is equal to the ratio of the marginal products of the inputs