Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please write the steps. The term structure of effective annual yield rates for zero coupon bonds is given as follows: 1- and 2-year maturity, 10%;

please write the steps.

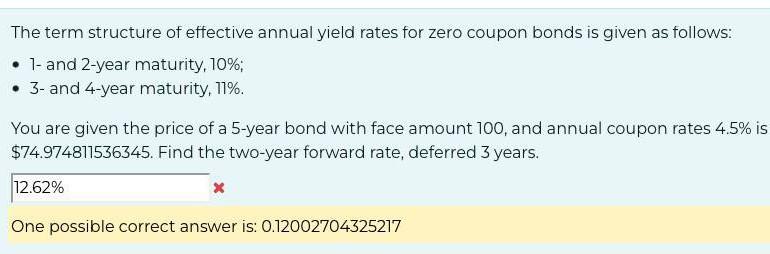

The term structure of effective annual yield rates for zero coupon bonds is given as follows: 1- and 2-year maturity, 10%; 3- and 4-year maturity, 11%. You are given the price of a 5-year bond with face amount 100, and annual coupon rates 4.5% is $74.974811536345. Find the two-year forward rate, deferred 3 years. 12.62% X One possible correct answer is: 0.12002704325217Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment The Study Of An Economic Aggregate

Authors: Philip J. Lund

1st Edition

0444851380,1483256901