Answered step by step

Verified Expert Solution

Question

1 Approved Answer

pls respond asap I work for a financial institution. I have the following portfolio of over-the-counter options on gold. Each contract is for 50 ounces

pls respond asap

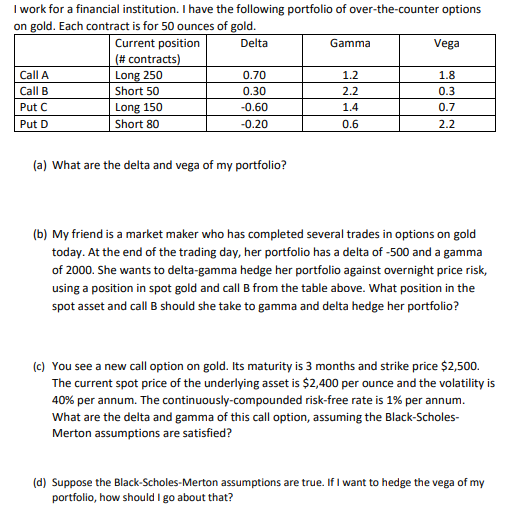

I work for a financial institution. I have the following portfolio of over-the-counter options on gold. Each contract is for 50 ounces of gold. Current position Delta Gamma Vega (#contracts) Call A Long 250 0.70 1.2 1.8 Call B Short 50 0.30 2.2 0.3 Put C Long 150 -0.60 1.4 0.7 Put D Short 80 -0.20 0.6 2.2 (a) What are the delta and vega of my portfolio? (b) My friend is a market maker who has completed several trades in options on gold today. At the end of the trading day, her portfolio has a delta of - 500 and a gamma of 2000. She wants to delta-gamma hedge her portfolio against overnight price risk, using a position in spot gold and call B from the table above. What position in the spot asset and call B should she take to gamma and delta hedge her portfolio? (c) You see a new call option on gold. Its maturity is 3 months and strike price $2,500. The current spot price of the underlying asset is $2,400 per ounce and the volatility is 40% per annum. The continuously-compounded risk-free rate is 1% per annum. What are the delta and gamma of this call option, assuming the Black-Scholes- Merton assumptions are satisfied? (d) Suppose the Black-Scholes-Merton assumptions are true. If I want to hedge the vega of my portfolio, how should I go about that? I work for a financial institution. I have the following portfolio of over-the-counter options on gold. Each contract is for 50 ounces of gold. Current position Delta Gamma Vega (#contracts) Call A Long 250 0.70 1.2 1.8 Call B Short 50 0.30 2.2 0.3 Put C Long 150 -0.60 1.4 0.7 Put D Short 80 -0.20 0.6 2.2 (a) What are the delta and vega of my portfolio? (b) My friend is a market maker who has completed several trades in options on gold today. At the end of the trading day, her portfolio has a delta of - 500 and a gamma of 2000. She wants to delta-gamma hedge her portfolio against overnight price risk, using a position in spot gold and call B from the table above. What position in the spot asset and call B should she take to gamma and delta hedge her portfolio? (c) You see a new call option on gold. Its maturity is 3 months and strike price $2,500. The current spot price of the underlying asset is $2,400 per ounce and the volatility is 40% per annum. The continuously-compounded risk-free rate is 1% per annum. What are the delta and gamma of this call option, assuming the Black-Scholes- Merton assumptions are satisfied? (d) Suppose the Black-Scholes-Merton assumptions are true. If I want to hedge the vega of my portfolio, how should I go about thatStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Future Of Pricing How Airline Ticket Pricing Has Inspired A Revolution

Authors: E. Boyd

1st Edition

0230600190,0230606903