Answered step by step

Verified Expert Solution

Question

1 Approved Answer

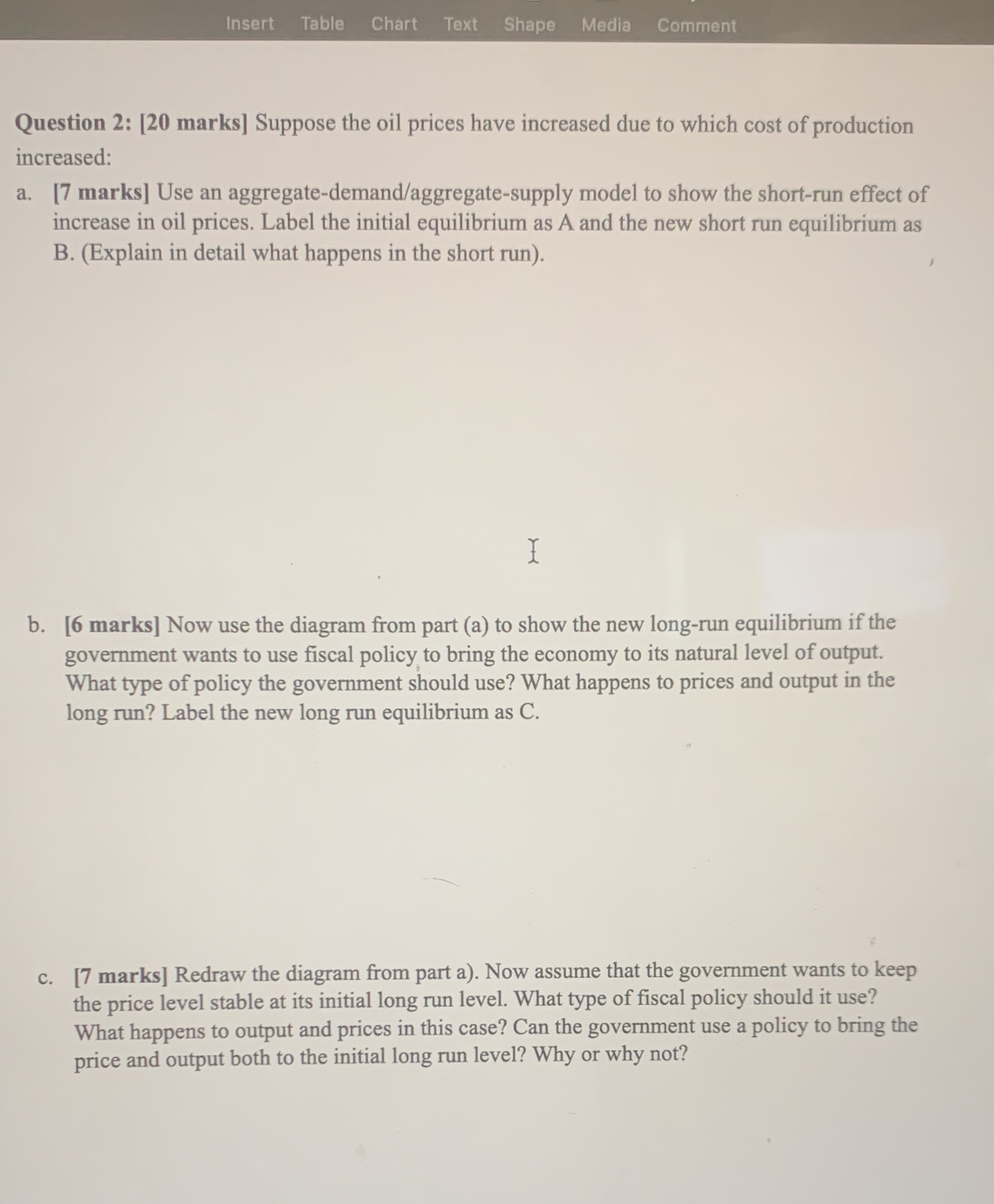

Plss fast Insert Table Chart Text Shape Media Comment Question 2: [20 marks] Suppose the oil prices have increased due to which cost of production

Plss fast

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Vanishing American Corporation Navigating The Hazards Of A New Economy

Authors: Jerry Davis, Gerald F Davis

1st Edition

1626562792, 9781626562790