Answered step by step

Verified Expert Solution

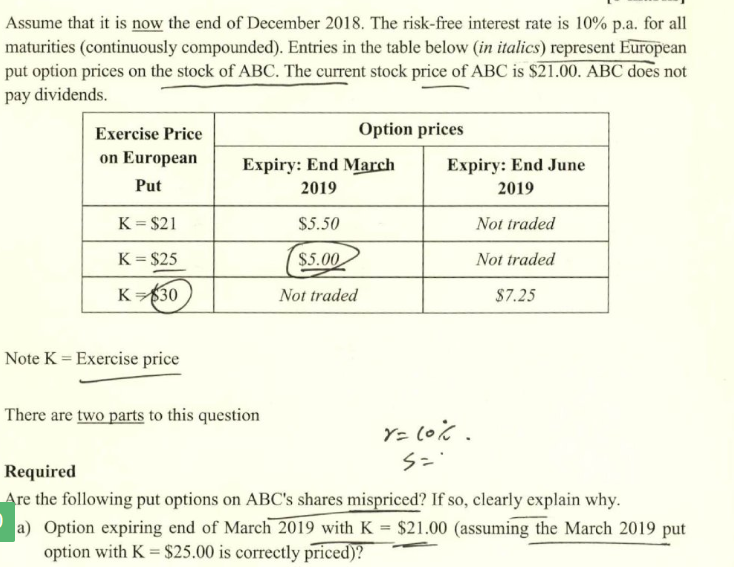

Question

1 Approved Answer

plz answer 2 sub-question as a whole. Assume that it is now the end of December 2018. The risk-free interest rate is 10% p.a. for

plz answer 2 sub-question as a whole.

Assume that it is now the end of December 2018. The risk-free interest rate is 10% p.a. for all maturities (continuously compounded). Entries in the table below (in italics) represent European put option prices on the stock of ABC. The current stock price of ABC is $21.00. ABC does not pay dividends. Option prices Exercise Price on European Put Expiry: End March 2019 Expiry: End June 2019 K = $21 Not traded $5.50 ( $5.00 Not traded K= $25 K=$30 Not traded $7.25 Note K = Exercise price There are two parts to this question YaLoL. so Required Are the following put options on ABC's shares mispriced? If so, clearly explain why. a) Option expiring end of March 2019 with K = $21.00 (assuming the March 2019 put option with K = $25.00 is correctly priced)? 5) Option expiring end of June 2019 with K = $30.00? If this option is mis-priced also clearly state how you would exploit any arbitrage opportunity and any expected arbitrage profit. If required assume long or short sales of shares are allowed and that you can borrow or lend at the risk free rate. Ignore all transaction costs other than the costs of borrowing or lending. Assume that it is now the end of December 2018. The risk-free interest rate is 10% p.a. for all maturities (continuously compounded). Entries in the table below (in italics) represent European put option prices on the stock of ABC. The current stock price of ABC is $21.00. ABC does not pay dividends. Option prices Exercise Price on European Put Expiry: End March 2019 Expiry: End June 2019 K = $21 Not traded $5.50 ( $5.00 Not traded K= $25 K=$30 Not traded $7.25 Note K = Exercise price There are two parts to this question YaLoL. so Required Are the following put options on ABC's shares mispriced? If so, clearly explain why. a) Option expiring end of March 2019 with K = $21.00 (assuming the March 2019 put option with K = $25.00 is correctly priced)? 5) Option expiring end of June 2019 with K = $30.00? If this option is mis-priced also clearly state how you would exploit any arbitrage opportunity and any expected arbitrage profit. If required assume long or short sales of shares are allowed and that you can borrow or lend at the risk free rate. Ignore all transaction costs other than the costs of borrowing or lendingStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started