Answered step by step

Verified Expert Solution

Question

1 Approved Answer

plz answer all for great review. i Answered some but we're not sure about them When there is a change in the estimated useful life

plz answer all for great review. i Answered some but we're not sure about them

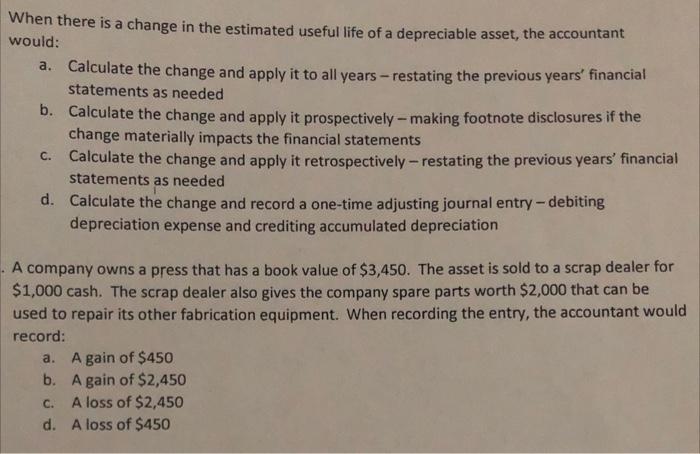

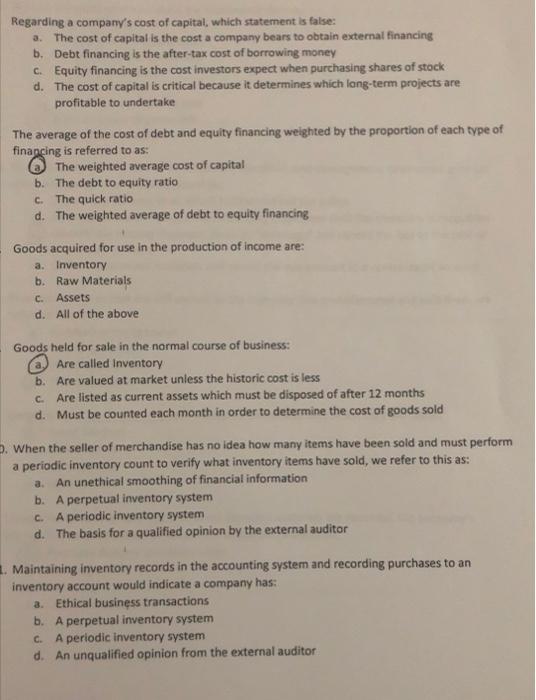

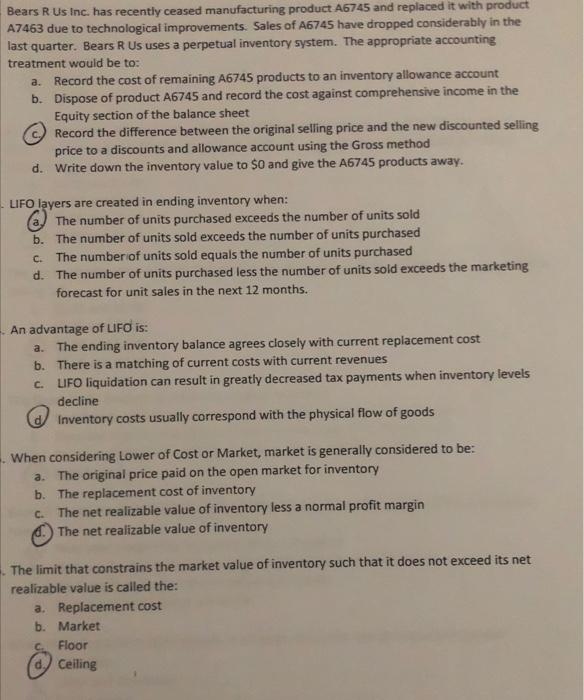

When there is a change in the estimated useful life of a depreciable asset, the accountant would: a. Calculate the change and apply it to all years-restating the previous years' financial statements as needed b. Calculate the change and apply it prospectively-making footnote disclosures if the change materially impacts the financial statements C. Calculate the change and apply it retrospectively-restating the previous years' financial statements as needed d. Calculate the change and record a one-time adjusting journal entry-debiting depreciation expense and crediting accumulated depreciation . A company owns a press that has a book value of $3,450. The asset is sold to a scrap dealer for $1,000 cash. The scrap dealer also gives the company spare parts worth $2,000 that can be used to repair its other fabrication equipment. When recording the entry, the accountant would record: a. A gain of $450 b. A gain of $2,450 C. A loss of $2,450 d. A loss of $450 Regarding a company's cost of capital, which statement is false: a. The cost of capital is the cost a company bears to obtain external financing b. Debt financing is the after-tax cost of borrowing money c. Equity financing is the cost investors expect when purchasing shares of stock d. The cost of capital is critical because it determines which long-term projects are profitable to undertake The average of the cost of debt and equity financing weighted by the proportion of each type of financing is referred to as: The weighted average cost of capital b. The debt to equity ratio c. The quick ratio d. The weighted average of debt to equity financing Goods acquired for use in the production of income are: a. Inventory b. Raw Materials c. Assets d. All of the above Goods held for sale in the normal course of business: Are called Inventory b. Are valued at market unless the historic cost is less c. Are listed as current assets which must be disposed of after 12 months d. Must be counted each month in order to determine the cost of goods sold D. When the seller of merchandise has no idea how many items have been sold and must perform a periodic inventory count to verify what inventory items have sold, we refer to this as: a. An unethical smoothing of financial information b. A perpetual inventory system c. A periodic inventory system d. The basis for a qualified opinion by the external auditor . Maintaining inventory records in the accounting system and recording purchases to an inventory account would indicate a company has: a. Ethical business transactions b. A perpetual inventory system c. A periodic inventory system d. An unqualified opinion from the external auditor Bears R Us Inc. has recently ceased manufacturing product A6745 and replaced it with product A7463 due to technological improvements. Sales of A6745 have dropped considerably in the last quarter. Bears R Us uses a perpetual inventory system. The appropriate accounting treatment would be to: a. Record the cost of remaining A6745 products to an inventory allowance account Dispose of product A6745 and record the cost against comprehensive income in the Equity section of the balance sheet b. Record the difference between the original selling price and the new discounted selling price to a discounts and allowance account using the Gross method d. Write down the inventory value to $0 and give the A6745 products away. LIFO layers are created in ending inventory when: The number of units purchased exceeds the number of units sold b. The number of units sold exceeds the number of units purchased The number of units sold equals the number of units purchased C. d. The number of units purchased less the number of units sold exceeds the marketing forecast for unit sales in the next 12 months. An advantage of LIFO is: a. The ending inventory balance agrees closely with current replacement cost b. There is a matching of current costs with current revenues c. LIFO liquidation can result in greatly decreased tax payments when inventory levels decline Inventory costs usually correspond with the physical flow of goods When considering Lower of Cost or Market, market is generally considered to be: a. The original price paid on the open market for inventory b. The replacement cost of inventory c. The net realizable value of inventory less a normal profit margin The net realizable value of inventory The limit that constrains the market value of inventory such that it does not exceed its net realizable value is called the: a. Replacement cost b. Market C. Floor d. Ceiling Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Susan V. Crosson, Belverd E. Needles

8th Edition

9780618777174, 618777180, 618777172, 978-0618777181