Answered step by step

Verified Expert Solution

Question

1 Approved Answer

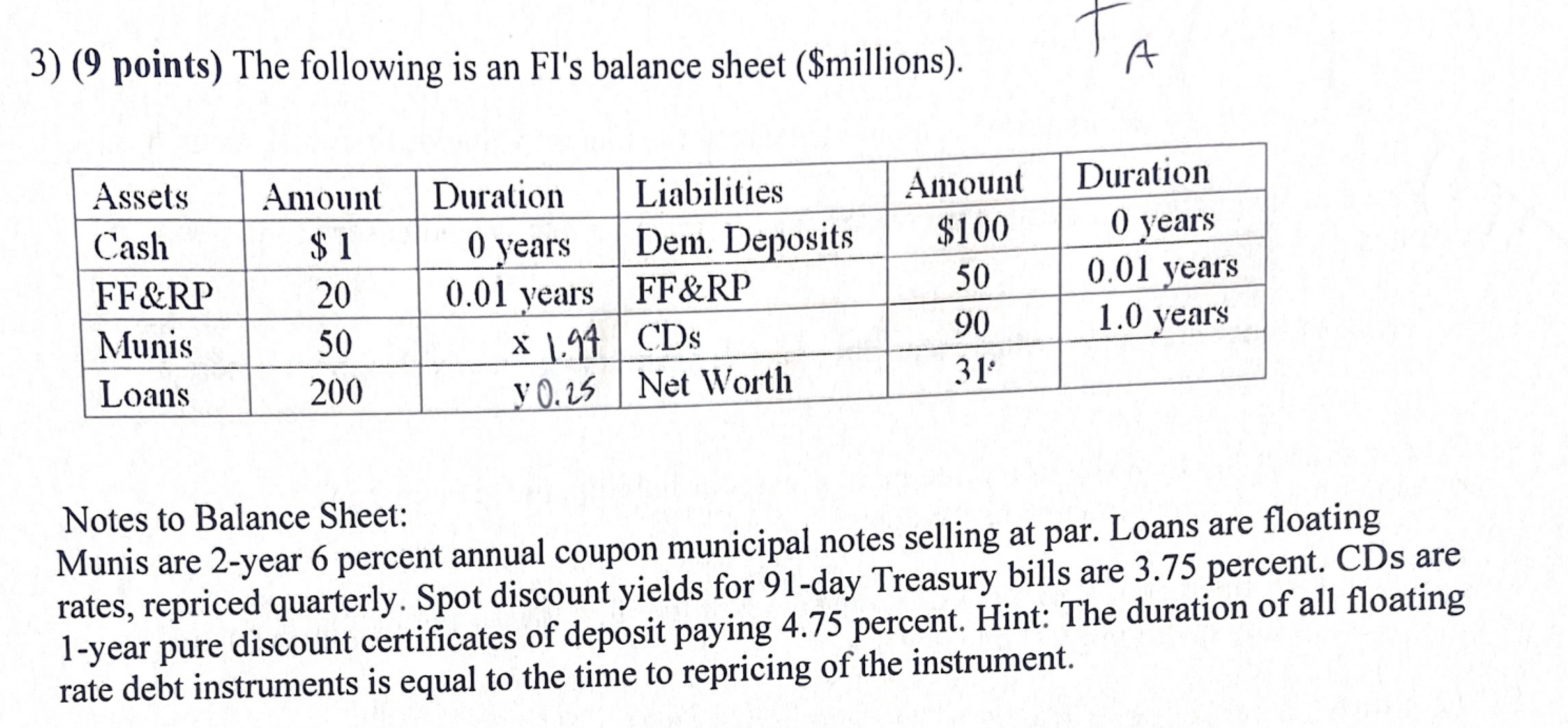

points ) The following is an Fl ' s balance sheet ( $millions ) . A table [ [ Assets , Amount,Duration,Liabilities,Amount,Duration ] ,

points The following is an Fls balance sheet $millions

A

tableAssetsAmount,Duration,Liabilities,Amount,DurationCash$ years,Dem. Deposits,$ yearsFF&RP years,FF&RP yearsMunisCDs yearsLoansNet Worth,

Notes to Balance Sheet:

Munis are year percent annual coupon municipal notes selling at par. Loans are floating rates, repriced quarterly. Spot discount yields for day Treasury bills are percent. CDs are year pure discount certificates of deposit paying percent. Hint: The duration of all floating rate debt instruments is equal to the time to repricing of the instrument.

a What is the duration of the munnicipal notes value of x

b What is this banks interest rate exposure, if any?

c What will be the impact, on the market value of the banks equity if all interest rates increase by baisis points?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Issues In Finance

Authors: Simon Grima, Frank Bezzina, Inna Romanova

1st Edition

1786359073, 978-1786359070