Answered step by step

Verified Expert Solution

Question

1 Approved Answer

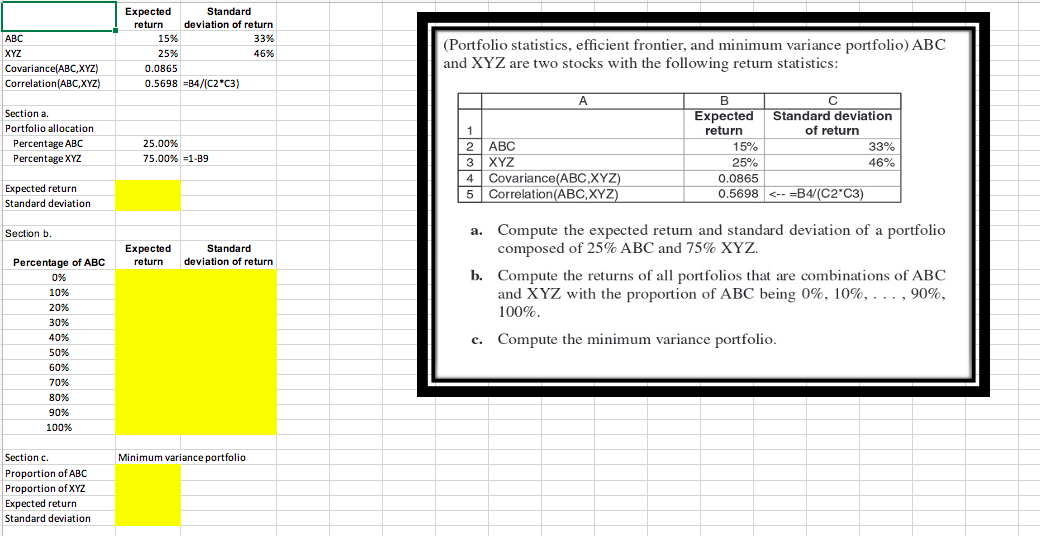

(Portfolio statistics, efficient frontier, and minimum variance portfolio) ABC and XYZ are two stocks with the following return statistics: a. Compute the expected return and

(Portfolio statistics, efficient frontier, and minimum variance portfolio) ABC and XYZ are two stocks with the following return statistics: a. Compute the expected return and standard deviation of a portfolio composed of 25%ABC and 75%XYZ. b. Compute the returns of all portfolios that are combinations of ABC and XYZ with the proportion of ABC being 0%,10%,,90%, 100%. c. Compute the minimum variance portfolio

(Portfolio statistics, efficient frontier, and minimum variance portfolio) ABC and XYZ are two stocks with the following return statistics: a. Compute the expected return and standard deviation of a portfolio composed of 25%ABC and 75%XYZ. b. Compute the returns of all portfolios that are combinations of ABC and XYZ with the proportion of ABC being 0%,10%,,90%, 100%. c. Compute the minimum variance portfolio Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management For Nurse Managers

Authors: J. Michael Leger

5th Edition

1284230937, 9781284230932