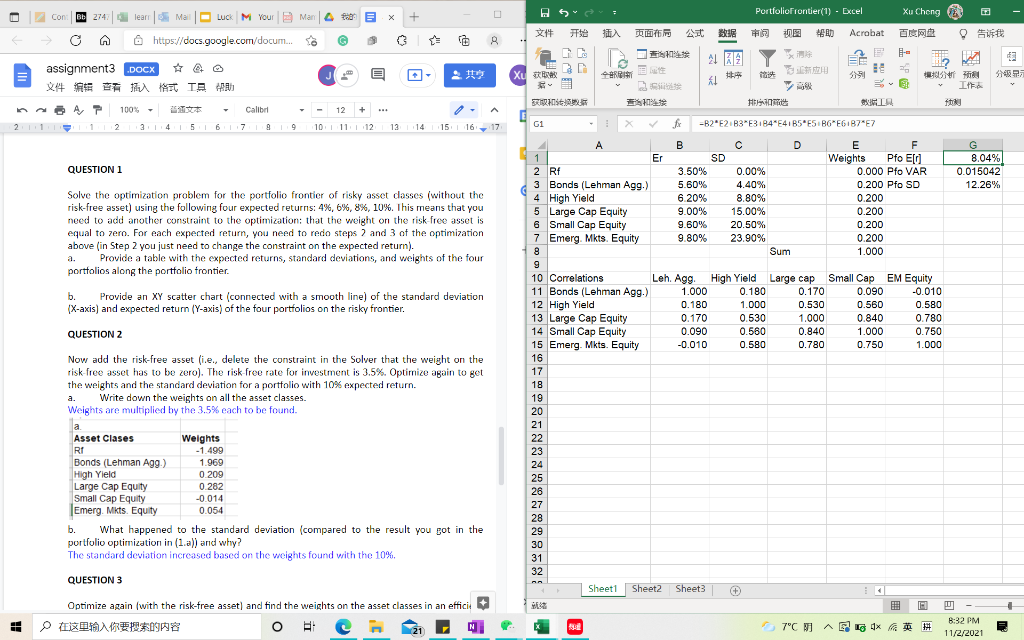

PortfolioFrontier(1) - Excel Con Bb 274 Con learr Mal Luck M Your Man ham X + Xu Cheng Acrobat 9 G @ https://docs.google.com/docum... B NE ALAA E EE 3751 assignment3 .DOCX J. E ARIMI Xu # trist SH A It T 100% - Calibri 12 + na, 2 1 1 : 2 34 | 5 6 7 1919 10 | 11 | 12 13 14 15 16 16-17 G1 -B2E2 B3 B3 184 E41B5E5 BG E61B74E7 QUESTION 1 Solve the optimization problem for the portfolio frontier of risky asset dasses (without the risk-free asset) using the following four expected returns: 4%, 6%, 8%, 10%. This means that you need to add another constraint to the optimization: that the weight on the risk free asset is equal to zero. For each expected return, you need to redo steps 2 and 3 of the optimization above (in Step 2 you just need to change the constraint on the expected return) Provide a table with the expected returns, standard deviations, and weights of the four portfolios along the portfolio frontier b. Provide an XY scatter chart (connected with a smooth line) of the standard deviation (X-axis) and expected return (Y-axis) of the four portfolios on the risky frontier. QUESTION 2 2 Now add the risk-free asset (i.e., delete the constraint in the Solver that the weight on the risk free asset has to be zoro). The risk free rate for investment is 3.5%. Optimize again to get the weights and the standard deviation for a portfolio with 10% expected return. a. Write down the weights on all the asset classes. Weights are multiplied by the 3.5% cach to be found. a. Asset Clases Weights RI -1.499 Bonds (Lehman Ag9) 1.969 High Yield 0.209 Large Cap Equity 0.282 Small Cap Equity -0.014 (Emerg Mikts. Equity 0.054 b. What happened to the standard deviation (compared to the result you got in the portfolio optimization in (1. a)) and why? The standard deviation increased based on the weights found with the 10%. A B B C D E F G 91 Er SD Weights Pfo El 8.04% 2 Rf 3.50% 0.00% 0.000 Pfo VAR 0.015042 3 Bonds (Lehman Agg.) 5.60% 4.40% 0.200 Pin SD 12.26% 4 High Yield 6.20% 8.80% 0.200 5 Large Cap Equity 9.00% 15.00% 0.200 6 Small Cap Equity 9.60% 20.50% 0.200 7 Emerg. Mkts. Equity 9.80% 23.90% 0.200 8 8 Sum 1.000 9 9 10 Correlations Leh. Agg High Yield Large cap Small Cap EM Equity 11 Bonds (Lehman Agg.) 1.000 0.180 0.170 0.090 -0.010 12 High Yield 0.180 1.000 0.530 0.560 0.580 13 Large Cap Equity 0.170 0.530 1.000 0.840 0.780 14 Small Cap Equity 0.090 0.560 0.840 1.000 0.750 15 Emerg. Mkts. Equity -0.010 0.580 0.780 0.750 1.000 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 Sheet1 Sheet2 Sheet3 + ED 8:32 PM 7C LA 11/2/2021 QUESTION 3 I LU Optimize again with the risk-free asset and find the weights on the asset classes in an efficit # Exe S PortfolioFrontier(1) - Excel Con Bb 274 Con learr Mal Luck M Your Man ham X + Xu Cheng Acrobat 9 G @ https://docs.google.com/docum... B NE ALAA E EE 3751 assignment3 .DOCX J. E ARIMI Xu # trist SH A It T 100% - Calibri 12 + na, 2 1 1 : 2 34 | 5 6 7 1919 10 | 11 | 12 13 14 15 16 16-17 G1 -B2E2 B3 B3 184 E41B5E5 BG E61B74E7 QUESTION 1 Solve the optimization problem for the portfolio frontier of risky asset dasses (without the risk-free asset) using the following four expected returns: 4%, 6%, 8%, 10%. This means that you need to add another constraint to the optimization: that the weight on the risk free asset is equal to zero. For each expected return, you need to redo steps 2 and 3 of the optimization above (in Step 2 you just need to change the constraint on the expected return) Provide a table with the expected returns, standard deviations, and weights of the four portfolios along the portfolio frontier b. Provide an XY scatter chart (connected with a smooth line) of the standard deviation (X-axis) and expected return (Y-axis) of the four portfolios on the risky frontier. QUESTION 2 2 Now add the risk-free asset (i.e., delete the constraint in the Solver that the weight on the risk free asset has to be zoro). The risk free rate for investment is 3.5%. Optimize again to get the weights and the standard deviation for a portfolio with 10% expected return. a. Write down the weights on all the asset classes. Weights are multiplied by the 3.5% cach to be found. a. Asset Clases Weights RI -1.499 Bonds (Lehman Ag9) 1.969 High Yield 0.209 Large Cap Equity 0.282 Small Cap Equity -0.014 (Emerg Mikts. Equity 0.054 b. What happened to the standard deviation (compared to the result you got in the portfolio optimization in (1. a)) and why? The standard deviation increased based on the weights found with the 10%. A B B C D E F G 91 Er SD Weights Pfo El 8.04% 2 Rf 3.50% 0.00% 0.000 Pfo VAR 0.015042 3 Bonds (Lehman Agg.) 5.60% 4.40% 0.200 Pin SD 12.26% 4 High Yield 6.20% 8.80% 0.200 5 Large Cap Equity 9.00% 15.00% 0.200 6 Small Cap Equity 9.60% 20.50% 0.200 7 Emerg. Mkts. Equity 9.80% 23.90% 0.200 8 8 Sum 1.000 9 9 10 Correlations Leh. Agg High Yield Large cap Small Cap EM Equity 11 Bonds (Lehman Agg.) 1.000 0.180 0.170 0.090 -0.010 12 High Yield 0.180 1.000 0.530 0.560 0.580 13 Large Cap Equity 0.170 0.530 1.000 0.840 0.780 14 Small Cap Equity 0.090 0.560 0.840 1.000 0.750 15 Emerg. Mkts. Equity -0.010 0.580 0.780 0.750 1.000 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 Sheet1 Sheet2 Sheet3 + ED 8:32 PM 7C LA 11/2/2021 QUESTION 3 I LU Optimize again with the risk-free asset and find the weights on the asset classes in an efficit # Exe S