Answered step by step

Verified Expert Solution

Question

1 Approved Answer

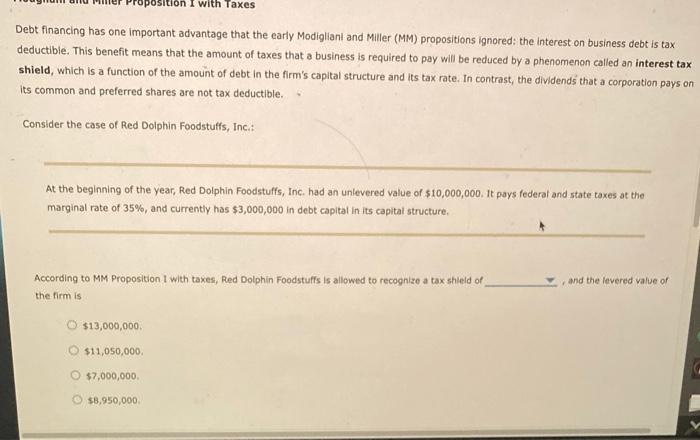

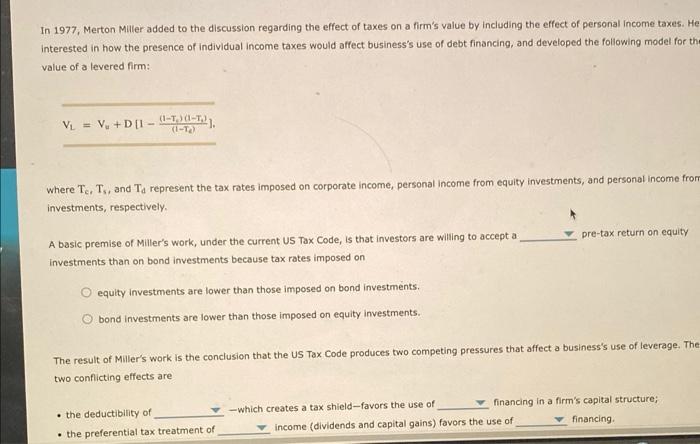

position I with Taxes Debt financing has one important advantage that the early Modigliani and Miller (MM) propositions ignored the interest on business debt is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Numerical Solution Of The American Option Pricing Problem Finite Difference And Transform Approaches

Authors: Carl Chiarella, Boda Kang , Gunter H Meyer

1st Edition

9814452610,9814452637