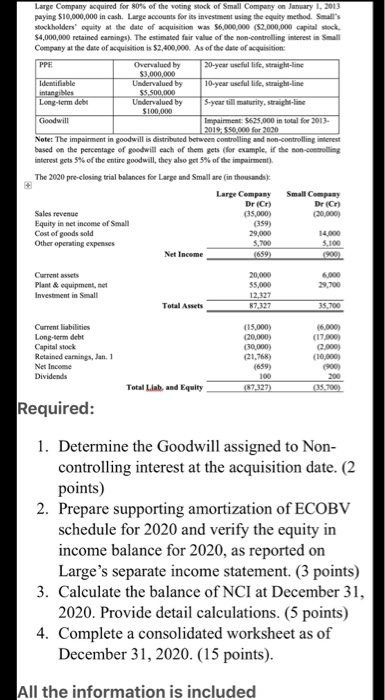

PPE Large Company acquired for 80% of the voting stock of Small Company on January 1, 2013 paying $10,000,000 in cash. Large accounts for its investment using the equity method. Small's stockholders' equity at the date of acquisition was 56,000,000 (52,000,000 capital stock $4,000,000 retained earnings). The estimated fair value of the non-controlling interest in Small Company at the date of acquisition is $2,400,000. As of the date of acquisition: Overvalued by 20-year useful life, straight-line $3,000,000 Identifiable Undervalued by 10-year useful life, straight-line intangibles $5.500,000 Long-term debe Undervalued by S-year till maturity, straight-line $100,000 Goodwill Impairment: 5625.000 in total for 2013- 2019-550.000 for 2020 Note: The impairment in goodwill is distributed between controlling and non-controlling interest based on the percentage of goodwill each of them gets (for example, if the non-controlling interest gets 5% of the entire goodwill, they also get 5% of the impairment). The 2020 pre-closing trial balances for Large and Small are (in thousands): Large Company Small Company Dr (Cr) Dr (Cr) Sales revenue (35,000) (20,000) Equity in net income of Small (359) Cost of goods sold 29.000 14.000 Other operating expenses 3.700 5.100 Net Income (659) 6.000 Current assets Plant & equipment, net Investment in Small 29.700 20,000 55,000 12.327 87.327 Total Assets (17000) Current liabilities Long-term debe Capital stock Retained earnings, Jan. 1 Net Income Dividends (15.000) (20,000) (30,000) (21,768) 659) (10,000) 900 Total Limb and Equity (87.327) (35,700) Required: 1. Determine the Goodwill assigned to Non- controlling interest at the acquisition date. (2 points) 2. Prepare supporting amortization of ECOBV schedule for 2020 and verify the equity in income balance for 2020, as reported on Large's separate income statement. (3 points) 3. Calculate the balance of NCI at December 31, 2020. Provide detail calculations. (5 points) 4. Complete a consolidated worksheet as of December 31, 2020. (15 points). All the information is included PPE Large Company acquired for 80% of the voting stock of Small Company on January 1, 2013 paying $10,000,000 in cash. Large accounts for its investment using the equity method. Small's stockholders' equity at the date of acquisition was 56,000,000 (52,000,000 capital stock $4,000,000 retained earnings). The estimated fair value of the non-controlling interest in Small Company at the date of acquisition is $2,400,000. As of the date of acquisition: Overvalued by 20-year useful life, straight-line $3,000,000 Identifiable Undervalued by 10-year useful life, straight-line intangibles $5.500,000 Long-term debe Undervalued by S-year till maturity, straight-line $100,000 Goodwill Impairment: 5625.000 in total for 2013- 2019-550.000 for 2020 Note: The impairment in goodwill is distributed between controlling and non-controlling interest based on the percentage of goodwill each of them gets (for example, if the non-controlling interest gets 5% of the entire goodwill, they also get 5% of the impairment). The 2020 pre-closing trial balances for Large and Small are (in thousands): Large Company Small Company Dr (Cr) Dr (Cr) Sales revenue (35,000) (20,000) Equity in net income of Small (359) Cost of goods sold 29.000 14.000 Other operating expenses 3.700 5.100 Net Income (659) 6.000 Current assets Plant & equipment, net Investment in Small 29.700 20,000 55,000 12.327 87.327 Total Assets (17000) Current liabilities Long-term debe Capital stock Retained earnings, Jan. 1 Net Income Dividends (15.000) (20,000) (30,000) (21,768) 659) (10,000) 900 Total Limb and Equity (87.327) (35,700) Required: 1. Determine the Goodwill assigned to Non- controlling interest at the acquisition date. (2 points) 2. Prepare supporting amortization of ECOBV schedule for 2020 and verify the equity in income balance for 2020, as reported on Large's separate income statement. (3 points) 3. Calculate the balance of NCI at December 31, 2020. Provide detail calculations. (5 points) 4. Complete a consolidated worksheet as of December 31, 2020. (15 points). All the information is included