Answered step by step

Verified Expert Solution

Question

1 Approved Answer

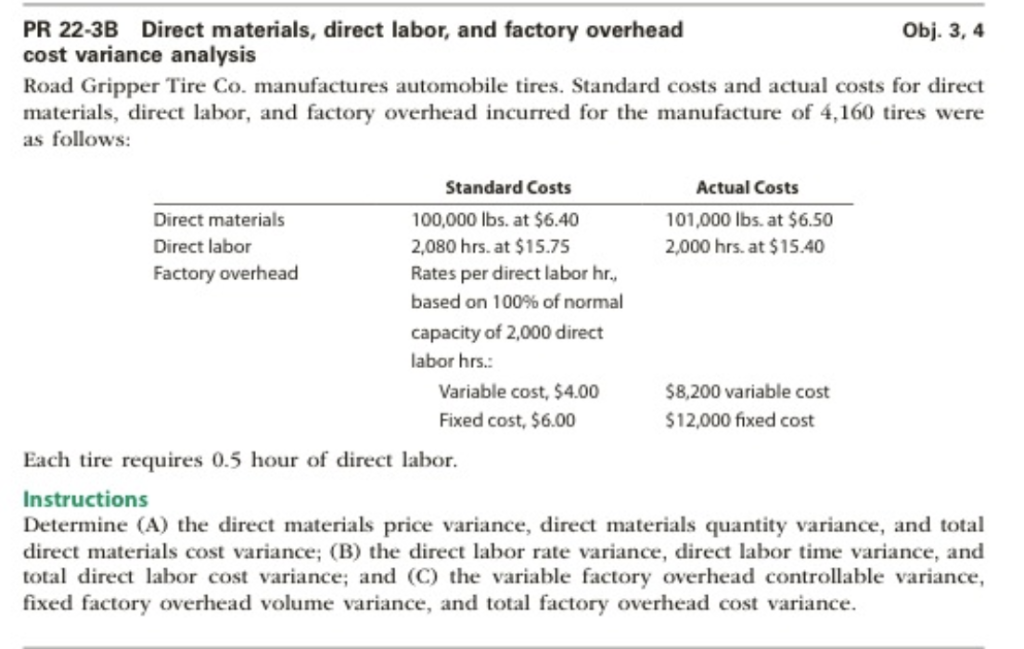

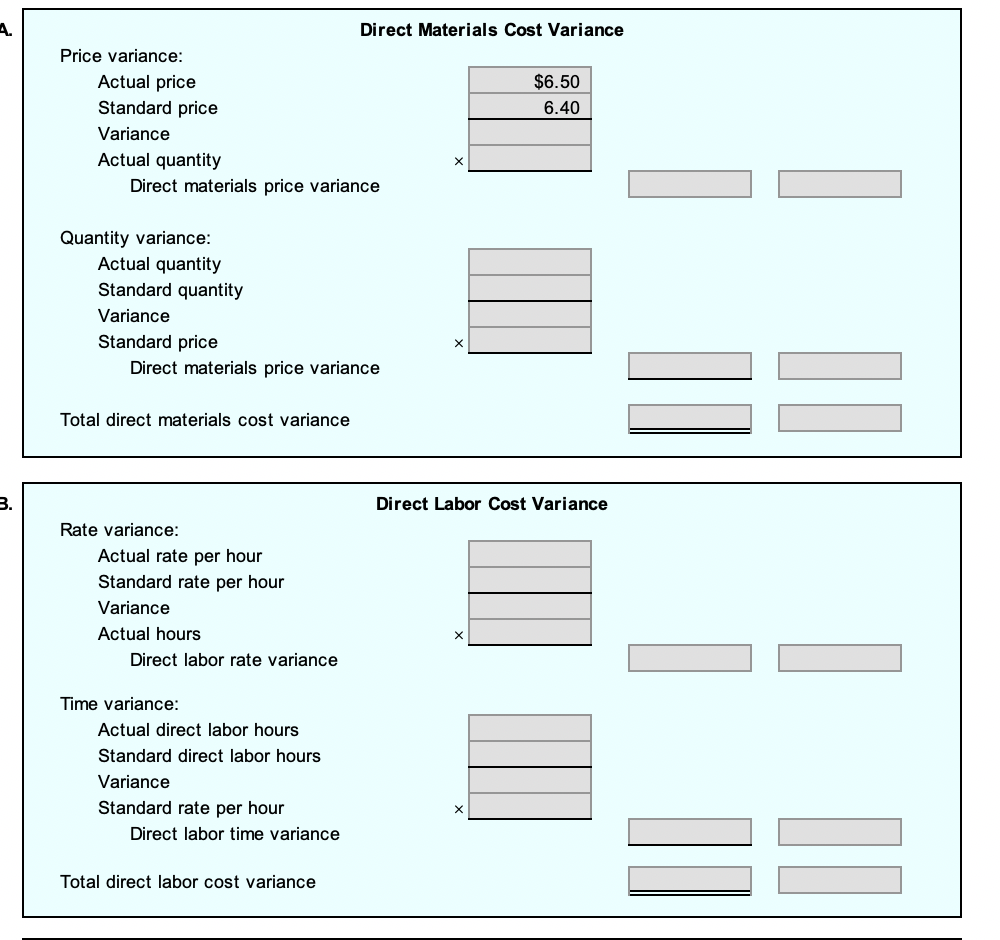

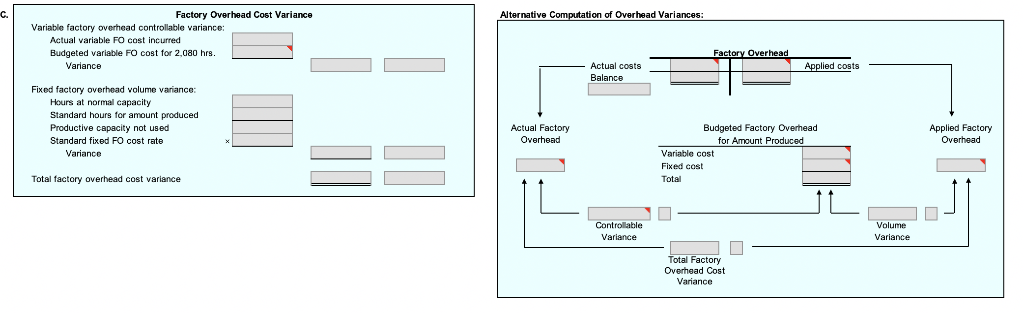

PR 22-3B Direct materials, direct labor, and factory overhead Obj. 3, 4 cost variance analysis Road Gripper Tire Co. manufactures automobile tires. Standard costs and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Actuarial Science

Authors: John James Hardy

1st Edition

1332733697, 978-1332733699