Question

Prepare a proper estate plan using the following rules A first-party trust is designed to hold a beneficiary's own assets. While the beneficiary is living,

Prepare a proper estate plan using the following rules

A first-party trust is designed to hold a beneficiary's own assets. While the beneficiary is living, the funds in the trust are used for the beneficiary's benefit, and when the beneficiary dies, any assets remaining in the trust are used to reimburse the government for the cost of medical care. Use and established a special needs trust, with a life insurance policy can pay directly into it, and it does not have to go through probate or be subject to estate tax. Be sure to review the beneficiary designation to make sure it names the trust, not the child.

ABLE Account An Achieving a Better Life Experience (ABLE) account allows people with disabilities who became disabled before they turned 26 to set aside up to $15,000 a year in tax-free savings accounts without affecting their eligibility for government benefits. This money can come from the individual with the disability or anyone else who may wish to give him money.

Created by Congress in 2014 and modeled on 529 savings plans for higher education, these accounts can be used to pay for qualifying expenses of the account beneficiary, such as the costs of treating the disability or for education, housing and health care, among other things. ABLE account programs have been rolling out on a state-by-state basis, but even if your state does not yet have its own program, many state programs allow out-of-state beneficiaries to open accounts. (For a directory of state programs, click here.)

Although it may be easy to set up an ABLE account, there are many hidden pitfalls associated with spending the funds in the accounts, both for the beneficiary and for her family members. In addition, ABLE accounts cannot hold more than $100,000 without jeopardizing government benefits like Medicaid and SSI. If there are funds remaining in an ABLE account upon the death of the account beneficiary, they must be first used to reimburse the government for Medicaid benefits received by the beneficiary, and then the remaining funds will have to pass through probate in order to be transferred to the beneficiary's heirs.

1. Minimize estate taxes.

2. Fund college education for the five grandchildren.3. Set up a special needs trust for Ivans future needs.

3. Set up a special needs trust for Ivans future needs.

4. Ensure that the vacation home is a permanent family home for children and grandchildren.

5. Keep 100 percent of business interests in the family.

6. Maintain control of the business until retirement at which time James and Joe will take over.

7. Transfer an additional $2 million to the Wounded Warrior Project some time in the future.

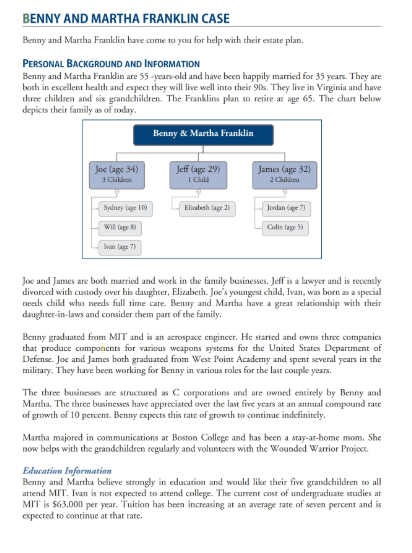

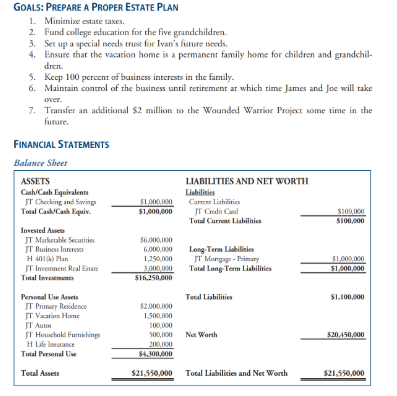

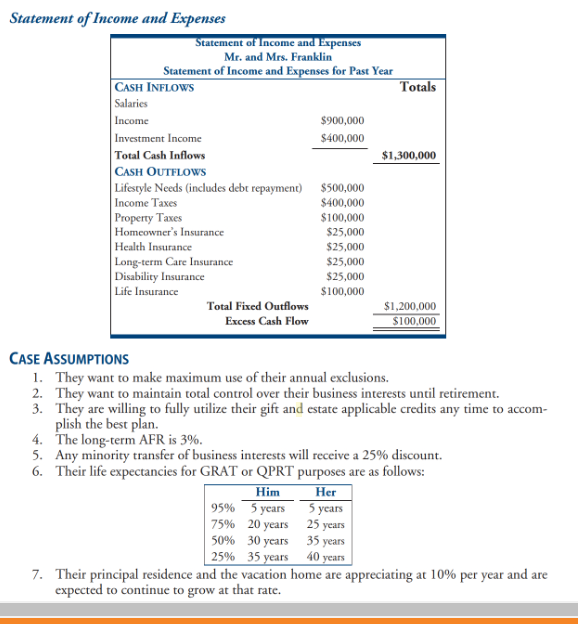

BENNY AND MARTHA FRANKLIN CASE Benny and Martha Franklin have come to you for help with their estate plan. PERSONAL BACKGROUND AND INFORMATION Benny and Martha Franklin are 55 years old and have been happily married for 35 years. They are boch in excellent health and expect they will live well into their 90s. They live in Virginia and have three children and six grandchildren. The Franklins plan to retire at age 65. The chart below depicts their family as of today. Benny & Martha Franklin loc (age 3) Clic Jeff (age 29) I Child James (age 32 Sydney 100 Elizabeth Cage 2) Willage Colin ay 5) Joe and James are both married and work in the family businesses. Jeff is a lawyer and is recently divorced with custody over his daughter, ElizabethJoe's youngest child, Ivan, was born as a special needs child who needs full time care. Benny and Martha have a great relationship with their daughter-in-laws and consider them part of the family. Benny graduated from MIT and is an acrospace engineer. He started and owns three companies that produce components for various weapons systems for the United States Department of Defense Joe and James both graduated from West Point Academy and spent several years in the military. They have been working for Benny in various roles for the last couple years. The three businesses are structured as C corporations and are owned entirely by Benny and Martha. The three businesses have appreciated over the last five years at an annual compound rate of growth of 10 percent. Benny expects this rate of growth to continue indefinitely Martha majored in communications at Boston College and has been a stay-at-home mom. She now helps with the grandchildren regularly and volunteers with the Wounded Warrior Project Education Information Benny and Martha believe strongly in education and would like their five grandchildren to all attend MIT. Ivan is not expected to attend college. The current cost of undergraduate studies at MIT is $63,000 per year. Tuition has been increasing at an average rate of seven percent and is expected to continue at that rate. Vacation Home Benny and Martha used to spend summers with friends at a home on Martha's Vineyard. They had such fond memories that once they became successful, they decided to purchase a home on Martha's Vineyard. They spend a substantial amount of time with their children and grandchildren at the vacation home every summer. Life Insurance The life insurance policy is a second-to-die policy on the lives of Benny and Martha. The policy has a death benefit of $2 million. Assume the replacement value of the policy is $200,000. The policy is currently owned by Benny and the three boys are the beneficiaries. Investment Real Estate The investment real estate includes several pieces of commercial real estate held in separate entities. The value is expected to increase at an average rate of 10 percent per year. Estate Planning Documents Benny and Martha have basic wills that make optimal use of testamentary bypass trusts and the marital deduction. The wills were designed to avoid all estate tax at the death of the first spouse and to make use of their lifetime exemptions. They also have durable powers of attorney for health care, advanced medical directives and financial powers of attorney, Prior Gifts In 2000, Benny established a Charitable Remainder Annuity Trust and funded it with highly appreciated publicly-traded stock worth $1,000,000. Benny and Martha were the income beneficiaries and the Wounded Warrior Project was the remainder beneficiary. The trust was set up with a ten-year term. In 2009, Benny established an irrevocable trust for each of the three boys and funded each trust with $1 million. The trusts were set up in such a way as to allow the trustee of cach trust to provide for the health, education, maintenance and support of the beneficiary. The trusts were established as simple trusts. The trustee is directed to not terminate the trust until the beneficiary turns age 45. The trusts were not set up as crummy trusts. The trust name the children (born and unborn) of each of the boys as the contingent beneficiaries for each trust. In 2012, Benny gave Uncle George a gift of $1,013,000 in cash. His uncle had been inspirational when Benny was a kid and has fallen on hard times. Martha has not made any taxable gifts in her past. GOALS: PREPARE A PROPER ESTATE PLAN 1. Minimize estate 2. Fund college education for the five grandchildren. 3. Set up a special needs trust for Ivan's future needs. 4. Ensure that the vacation home is a permanent family home for children and grandchil dren 5. Keep 100 percent of business interests in the family. 6. Maintain control of the business until retirement at which time James and Joe will take over. 7. Transfer an additional $2 million to the Wounded Warrior Project some time in the future FINANCIAL STATEMENTS Balance Sheet ASSETS Cash Cash Equivalents IT Checking and Swing Total Cacahui $100,000 $1,000,000 LIABILITIES AND NET WORTH Liabilities Cum liahilities IT Credit Card Total Current Liabilities Invested Act JT Market Securities IT Business Interese H4015) Man IT in Real Estate Talle $600.000 6.000.000 1.250,000 3.000.000 S162500D Long Term L ilities IT Morge Primary Total Long-Term Liabilities $1.000000 $1.000.000 Toual Liabilities SL.100.000 $200000 1.500.000 Penal Us IT Primary Residence IT Van Home ITA TT HP HLE Total P al Net Worth 500.000 200.000 Tous $21.550,000 Total Liabilities and Net Worth Statement of Income and Expenses Statement of Income and Expenses Mr. and Mrs. Franklin Statement of Income and Expenses for Past Year CASH INFLOWS Totals Salaries Income $900,000 Investment Income $400,000 Total Cash Inflows $1,300,000 CASH OUTFLOWS Lifestyle Needs includes debt repayment) $500,000 Income Taxes $400,000 Property Taxes $100,000 Homeowner's Insurance $25,000 Health Insurance $25,000 Long-term Care Insurance $25,000 Disability Insurance $25,000 Life Insurance $100,000 Total Fixed Outflows $1,200,000 Excess Cash Flow $100,000 CASE ASSUMPTIONS 1. They want to make maximum use of their annual exclusions. 2. They want to maintain total control over their business interests until retirement. 3. They are willing to fully utilize their gift and estate applicable credits any time to accom- plish the best plan. 4. The long-term AFR is 3%. 5. Any minority transfer of business interests will receive a 25% discount. 6. Their life expectancies for GRAT or QPRT purposes are as follows: Him Her 95% 5 years 5 years 75% 20 years 25 years 50% 30 years 35 years 25% 35 years 40 years 7. Their principal residence and the vacation home are appreciating at 10% per year and are expected to continue to grow at that rate. BENNY AND MARTHA FRANKLIN CASE Benny and Martha Franklin have come to you for help with their estate plan. PERSONAL BACKGROUND AND INFORMATION Benny and Martha Franklin are 55 years old and have been happily married for 35 years. They are boch in excellent health and expect they will live well into their 90s. They live in Virginia and have three children and six grandchildren. The Franklins plan to retire at age 65. The chart below depicts their family as of today. Benny & Martha Franklin loc (age 3) Clic Jeff (age 29) I Child James (age 32 Sydney 100 Elizabeth Cage 2) Willage Colin ay 5) Joe and James are both married and work in the family businesses. Jeff is a lawyer and is recently divorced with custody over his daughter, ElizabethJoe's youngest child, Ivan, was born as a special needs child who needs full time care. Benny and Martha have a great relationship with their daughter-in-laws and consider them part of the family. Benny graduated from MIT and is an acrospace engineer. He started and owns three companies that produce components for various weapons systems for the United States Department of Defense Joe and James both graduated from West Point Academy and spent several years in the military. They have been working for Benny in various roles for the last couple years. The three businesses are structured as C corporations and are owned entirely by Benny and Martha. The three businesses have appreciated over the last five years at an annual compound rate of growth of 10 percent. Benny expects this rate of growth to continue indefinitely Martha majored in communications at Boston College and has been a stay-at-home mom. She now helps with the grandchildren regularly and volunteers with the Wounded Warrior Project Education Information Benny and Martha believe strongly in education and would like their five grandchildren to all attend MIT. Ivan is not expected to attend college. The current cost of undergraduate studies at MIT is $63,000 per year. Tuition has been increasing at an average rate of seven percent and is expected to continue at that rate. Vacation Home Benny and Martha used to spend summers with friends at a home on Martha's Vineyard. They had such fond memories that once they became successful, they decided to purchase a home on Martha's Vineyard. They spend a substantial amount of time with their children and grandchildren at the vacation home every summer. Life Insurance The life insurance policy is a second-to-die policy on the lives of Benny and Martha. The policy has a death benefit of $2 million. Assume the replacement value of the policy is $200,000. The policy is currently owned by Benny and the three boys are the beneficiaries. Investment Real Estate The investment real estate includes several pieces of commercial real estate held in separate entities. The value is expected to increase at an average rate of 10 percent per year. Estate Planning Documents Benny and Martha have basic wills that make optimal use of testamentary bypass trusts and the marital deduction. The wills were designed to avoid all estate tax at the death of the first spouse and to make use of their lifetime exemptions. They also have durable powers of attorney for health care, advanced medical directives and financial powers of attorney, Prior Gifts In 2000, Benny established a Charitable Remainder Annuity Trust and funded it with highly appreciated publicly-traded stock worth $1,000,000. Benny and Martha were the income beneficiaries and the Wounded Warrior Project was the remainder beneficiary. The trust was set up with a ten-year term. In 2009, Benny established an irrevocable trust for each of the three boys and funded each trust with $1 million. The trusts were set up in such a way as to allow the trustee of cach trust to provide for the health, education, maintenance and support of the beneficiary. The trusts were established as simple trusts. The trustee is directed to not terminate the trust until the beneficiary turns age 45. The trusts were not set up as crummy trusts. The trust name the children (born and unborn) of each of the boys as the contingent beneficiaries for each trust. In 2012, Benny gave Uncle George a gift of $1,013,000 in cash. His uncle had been inspirational when Benny was a kid and has fallen on hard times. Martha has not made any taxable gifts in her past. GOALS: PREPARE A PROPER ESTATE PLAN 1. Minimize estate 2. Fund college education for the five grandchildren. 3. Set up a special needs trust for Ivan's future needs. 4. Ensure that the vacation home is a permanent family home for children and grandchil dren 5. Keep 100 percent of business interests in the family. 6. Maintain control of the business until retirement at which time James and Joe will take over. 7. Transfer an additional $2 million to the Wounded Warrior Project some time in the future FINANCIAL STATEMENTS Balance Sheet ASSETS Cash Cash Equivalents IT Checking and Swing Total Cacahui $100,000 $1,000,000 LIABILITIES AND NET WORTH Liabilities Cum liahilities IT Credit Card Total Current Liabilities Invested Act JT Market Securities IT Business Interese H4015) Man IT in Real Estate Talle $600.000 6.000.000 1.250,000 3.000.000 S162500D Long Term L ilities IT Morge Primary Total Long-Term Liabilities $1.000000 $1.000.000 Toual Liabilities SL.100.000 $200000 1.500.000 Penal Us IT Primary Residence IT Van Home ITA TT HP HLE Total P al Net Worth 500.000 200.000 Tous $21.550,000 Total Liabilities and Net Worth Statement of Income and Expenses Statement of Income and Expenses Mr. and Mrs. Franklin Statement of Income and Expenses for Past Year CASH INFLOWS Totals Salaries Income $900,000 Investment Income $400,000 Total Cash Inflows $1,300,000 CASH OUTFLOWS Lifestyle Needs includes debt repayment) $500,000 Income Taxes $400,000 Property Taxes $100,000 Homeowner's Insurance $25,000 Health Insurance $25,000 Long-term Care Insurance $25,000 Disability Insurance $25,000 Life Insurance $100,000 Total Fixed Outflows $1,200,000 Excess Cash Flow $100,000 CASE ASSUMPTIONS 1. They want to make maximum use of their annual exclusions. 2. They want to maintain total control over their business interests until retirement. 3. They are willing to fully utilize their gift and estate applicable credits any time to accom- plish the best plan. 4. The long-term AFR is 3%. 5. Any minority transfer of business interests will receive a 25% discount. 6. Their life expectancies for GRAT or QPRT purposes are as follows: Him Her 95% 5 years 5 years 75% 20 years 25 years 50% 30 years 35 years 25% 35 years 40 years 7. Their principal residence and the vacation home are appreciating at 10% per year and are expected to continue to grow at that rateStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISO 27001 Controls A Guide To Implementing And Auditing

Authors: IT Governance

1st Edition

1787781445, 978-1787781443