Answered step by step

Verified Expert Solution

Question

1 Approved Answer

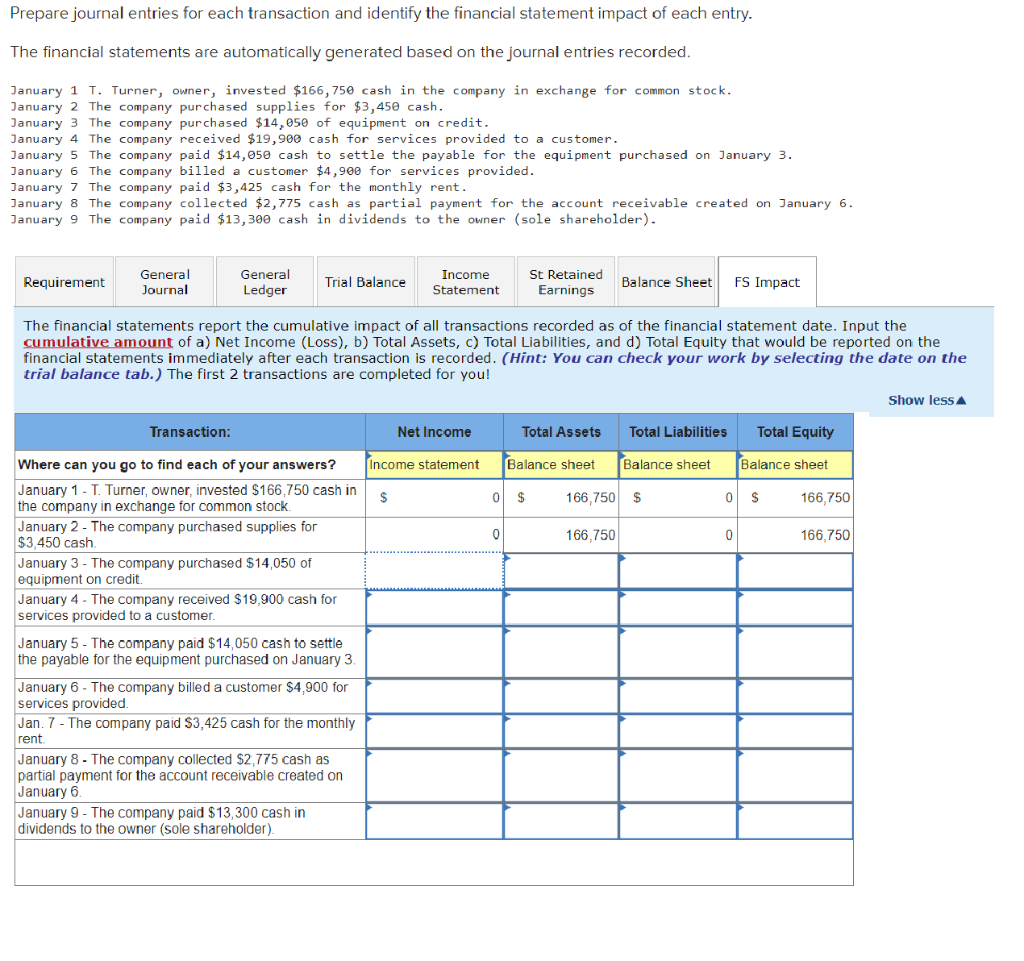

Prepare journal entries for each transaction and identify the financial statement impact of each entry. The financial statements are automatically generated based on the journal

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management Reporting Und Behavioral Accounting Verhaltenswirkungen Des Berichtswesens Im Unternehmen

Authors: Andreas Taschner

2nd., 2nd. Auflage Aufl. 2019 Edition

3658234911, 978-3658234911