Question

Prepare the Mechanical Radiology Manufacturing Ltd Case below and answer the questions specified below (1-3). Write down and specify any major difficulties you might have

Prepare the Mechanical Radiology Manufacturing Ltd Case below and answer the questions specified below (1-3). Write down and specify any major difficulties you might have had.

Mechanical Radiology Manufacturing Ltd (MRM hereafter) provides products for radiological services to hospitals in the UK. They have two operating (revenue-producing) departments, one produces replacement products and the other produces a special radiology scanner. In addition, to the operating departments, MRM Ltd has three supporting service departments: administrative services, maintenance, and cleaning/security services. MEM Ltd allocates Overhead from its service departments to its two operating departments using the 'direct method'. In the operating departments it employs machine hours as the allocation basis for overheads computing predetermined overhead rates.

While working on next year's budget a conflict has surfaced between departments on how the allocation of service department costs affects the evaluation of their performance. The replacement products department argues that the direct cost allocation system makes the performance of the radiology scanner manufacturing department look better than is really the case, and makes the replacement products department look worse. The CEO of MRM is concerned that he may lose the senior managers from Replacement Products, and so has decided that he needs to address the Overheads allocation system and see if it should be revised. He has therefore asked you, as his Management Accountant, to advise him in this matter.

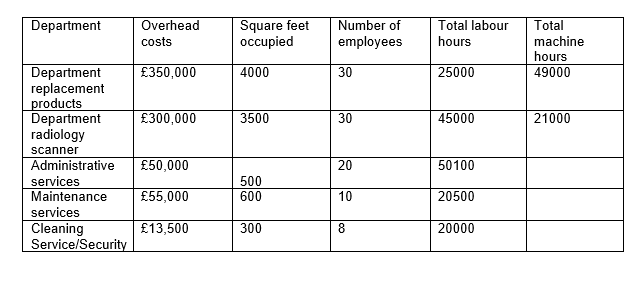

The following table reports overhead costs which have been allocated to each of the five departments, along with information about (i) area (square feet) occupied by each department, (ii) number of employees, (iii) total labour hours and (iv) total machine hours.

Prepare the Mechanical Radiology Manufacturing Ltd Case below and answer the questions specified below (1-3). Write down and specify any major difficulties you might have had.

Mechanical Radiology Manufacturing Ltd (MRM hereafter) provides products for radiological services to hospitals in the UK. They have two operating (revenue-producing) departments, one produces replacement products and the other produces a special radiology scanner. In addition, to the operating departments, MRM Ltd has three supporting service departments: administrative services, maintenance, and cleaning/security services. MEM Ltd allocates Overhead from its service departments to its two operating departments using the 'direct method'. In the operating departments it employs machine hours as the allocation basis for overheads computing predetermined overhead rates.

While working on next year's budget a conflict has surfaced between departments on how the allocation of service department costs affects the evaluation of their performance. The replacement products department argues that the direct cost allocation system makes the performance of the radiology scanner manufacturing department look better than is really the case, and makes the replacement products department look worse. The CEO of MRM is concerned that he may lose the senior managers from Replacement Products, and so has decided that he needs to address the Overheads allocation system and see if it should be revised. He has therefore asked you, as his Management Accountant, to advise him in this matter.

The following table reports overhead costs which have been allocated to each of the five departments, along with information about (i) area (square feet) occupied by each department, (ii) number of employees, (iii) total labour hours and (iv) total machine hours.

Prepare the Mechanical Radiology Manufacturing Ltd Case below and answer the questions specified below (1-3). Write down and specify any major difficulties you might have had.

Mechanical Radiology Manufacturing Ltd (MRM hereafter) provides products for radiological services to hospitals in the UK. They have two operating (revenue-producing) departments, one produces replacement products and the other produces a special radiology scanner. In addition, to the operating departments, MRM Ltd has three supporting service departments: administrative services, maintenance, and cleaning/security services. MEM Ltd allocates Overhead from its service departments to its two operating departments using the 'direct method'. In the operating departments it employs machine hours as the allocation basis for overheads computing predetermined overhead rates.

While working on next year's budget a conflict has surfaced between departments on how the allocation of service department costs affects the evaluation of their performance. The replacement products department argues that the direct cost allocation system makes the performance of the radiology scanner manufacturing department look better than is really the case, and makes the replacement products department look worse. The CEO of MRM is concerned that he may lose the senior managers from Replacement Products, and so has decided that he needs to address the Overheads allocation system and see if it should be revised. He has therefore asked you, as his Management Accountant, to advise him in this matter.

The following table reports overhead costs which have been allocated to each of the five departments, along with information about (i) area (square feet) occupied by each department, (ii) number of employees, (iii) total labour hours and (iv) total machine hours.

The CEO has asked you to analyse the financial data and then also consider other relevant non-financial information and to present a report advising him as to what decision he should make regarding the overhead allocation system. Your report must include the following:

Required:

- Allocate the service department costs to the production departments using the current basis for cost allocation, and using the 'direct method' for allocating service department costs to operating ones.

- Using the list of allocation bases provided above, select a new allocation base for each of the three service departments, based on the service role it plays within the firm. In each case, explain why you have seen the allocation base chosen as appropriate for the service department in question. (NB: Choose a different allocation base for each department).

- Based on your selections, use these allocation bases to recalculate the allocation of overhead costs from the service departments to each of the production departments, again using the 'direct method'.

DATA:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk-Based Internal Audit

Authors: Jason Lee Mefford

1st Edition

1631922629, 9781631922626