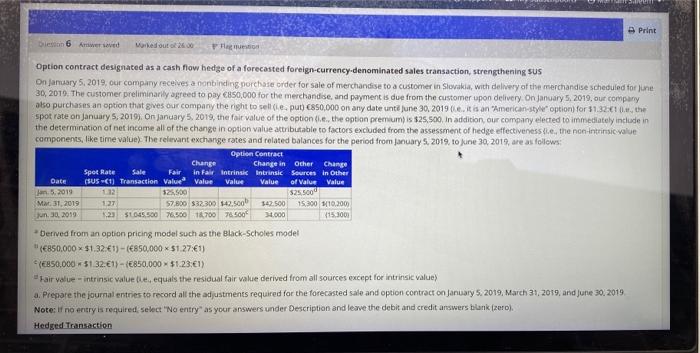

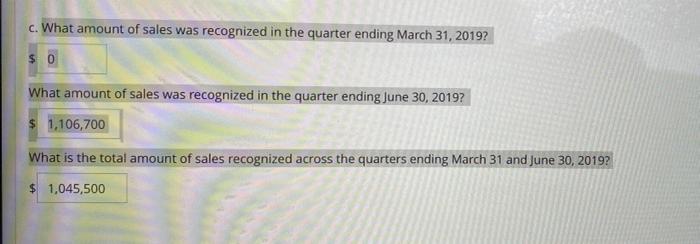

Print bles 6 Awer ved Marked out of 26.00 Option contract designated as a cash flow hedge of a forecasted foreign-currency.denominated sales transaction, strengthening SUS On January 5, 2019, our company receives a nonbinding porchase order for sale of merchandise to a customer in Slovakia, with delivery of the merchandise scheduled for ne 30, 2010. The customer preliminarily agreed to pay 850,000 for the merchandise, and payment is due from the customer upon delivery on January 5, 2019, our company ato purchases an option that gives our company the right to sell put) C850,000 on any date unti June 30, 2019 (e. it is an American styw" option) for $1.32K10, the spot rate on January 5, 2019), on January 5, 2019, the fair value of the option de the option premium) is $25.500. In addition, our company elected to immediately include in the determination of net income all of the change in option value attributable to factors excluded from the assessment of hedge effectiveness the the non-intrinsic value components, like time value). The relevant exchange rates and related balances for the period from January 5, 2019. to June 30, 2019, are as follows: Option Contract Change Change in other change Spot Rate Sale Fair in Fair Intrinsic Intrinsic Sources in Other (SUS (1) Transaction value Value Value Value of Value Value 5.2019 112 525.500 $25.500 Mar 31, 2019 127 57.800532,300 42.500 542.500 15.390 110.300) un 30, 2019 23 50 500 76.500 10700 74.500 34.000 (15.300 -Derived from an option pricing model such as the Black-Scholes model (850.000 $1.32:1) - (850,000 $1.27:41) (E850,000 51.32.61) - 850.000 $1.23.61) "Fair value - intrinsic value tie, equals the residual fair value derived from all sources except for intrinsic value) a. Prepare the journal entries to record all the adjustments required for the forecasted sale and option contract on January 5, 2019, March 31, 2019, and June 30, 2019 Note: If no entry is required, select "No entry" as your answers under Description and leave the debit and credit answers blank (zero). Hedged Transaction Date c. What amount of sales was recognized in the quarter ending March 31, 2019? $ 0 What amount of sales was recognized in the quarter ending June 30, 2019? $ 1,106,700 What is the total amount of sales recognized across the quarters ending March 31 and June 30, 2019? $ 1,045,500 Print bles 6 Awer ved Marked out of 26.00 Option contract designated as a cash flow hedge of a forecasted foreign-currency.denominated sales transaction, strengthening SUS On January 5, 2019, our company receives a nonbinding porchase order for sale of merchandise to a customer in Slovakia, with delivery of the merchandise scheduled for ne 30, 2010. The customer preliminarily agreed to pay 850,000 for the merchandise, and payment is due from the customer upon delivery on January 5, 2019, our company ato purchases an option that gives our company the right to sell put) C850,000 on any date unti June 30, 2019 (e. it is an American styw" option) for $1.32K10, the spot rate on January 5, 2019), on January 5, 2019, the fair value of the option de the option premium) is $25.500. In addition, our company elected to immediately include in the determination of net income all of the change in option value attributable to factors excluded from the assessment of hedge effectiveness the the non-intrinsic value components, like time value). The relevant exchange rates and related balances for the period from January 5, 2019. to June 30, 2019, are as follows: Option Contract Change Change in other change Spot Rate Sale Fair in Fair Intrinsic Intrinsic Sources in Other (SUS (1) Transaction value Value Value Value of Value Value 5.2019 112 525.500 $25.500 Mar 31, 2019 127 57.800532,300 42.500 542.500 15.390 110.300) un 30, 2019 23 50 500 76.500 10700 74.500 34.000 (15.300 -Derived from an option pricing model such as the Black-Scholes model (850.000 $1.32:1) - (850,000 $1.27:41) (E850,000 51.32.61) - 850.000 $1.23.61) "Fair value - intrinsic value tie, equals the residual fair value derived from all sources except for intrinsic value) a. Prepare the journal entries to record all the adjustments required for the forecasted sale and option contract on January 5, 2019, March 31, 2019, and June 30, 2019 Note: If no entry is required, select "No entry" as your answers under Description and leave the debit and credit answers blank (zero). Hedged Transaction Date c. What amount of sales was recognized in the quarter ending March 31, 2019? $ 0 What amount of sales was recognized in the quarter ending June 30, 2019? $ 1,106,700 What is the total amount of sales recognized across the quarters ending March 31 and June 30, 2019? $ 1,045,500