Answered step by step

Verified Expert Solution

Question

1 Approved Answer

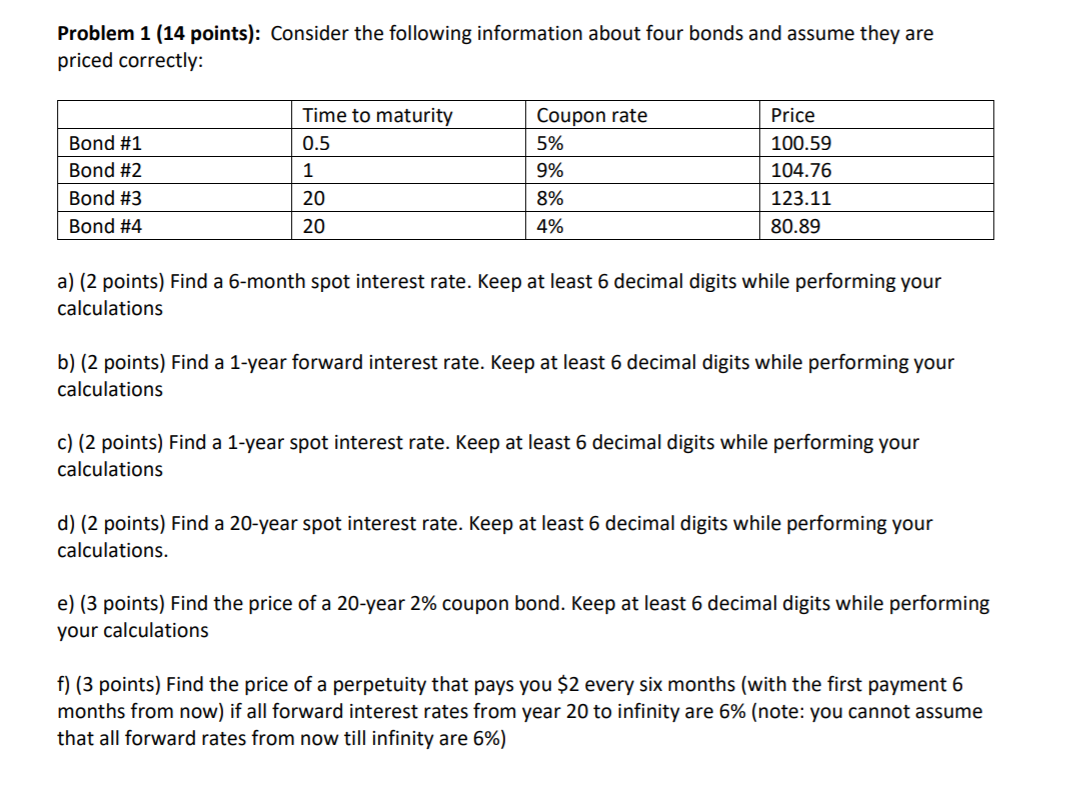

Problem 1 (14 points): Consider the following information about four bonds and assume they are priced correctly: Bond #1 Time to maturity 0.5 Coupon

Problem 1 (14 points): Consider the following information about four bonds and assume they are priced correctly: Bond #1 Time to maturity 0.5 Coupon rate 5% Bond #2 1 9% Bond #3 Bond #4 20 20 8% 4% Price 100.59 104.76 123.11 80.89 a) (2 points) Find a 6-month spot interest rate. Keep at least 6 decimal digits while performing your calculations b) (2 points) Find a 1-year forward interest rate. Keep at least 6 decimal digits while performing your calculations c) (2 points) Find a 1-year spot interest rate. Keep at least 6 decimal digits while performing your calculations d) (2 points) Find a 20-year spot interest rate. Keep at least 6 decimal digits while performing your calculations. e) (3 points) Find the price of a 20-year 2% coupon bond. Keep at least 6 decimal digits while performing your calculations f) (3 points) Find the price of a perpetuity that pays you $2 every six months (with the first payment 6 months from now) if all forward interest rates from year 20 to infinity are 6% (note: you cannot assume that all forward rates from now till infinity are 6%)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Venture capital and the finance of innovation

Authors: Andrew Metrick

2nd Edition

9781118137888, 470454709, 1118137884, 978-0470454701