Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Problem 1 2 - 1 0 APT Assume that the returns on individual securities are generated by the following two - factor model: Rit =

Problem APT

Assume that the returns on individual securities are generated by the following twofactor model:

RitERitbeta ijFtbeta iFt

Here:

Rit is the return on Security i at Time t

Ft and Ft are market factors with zero expectation and zero covariance.

In addition, assume that there is a capital market for four securities and the capital market for these four assets is perfect in the sense that there are no transaction costs and short sales ie negative positions are permitted. The characteristics of the four securities follow:

Security beta beta ER

a

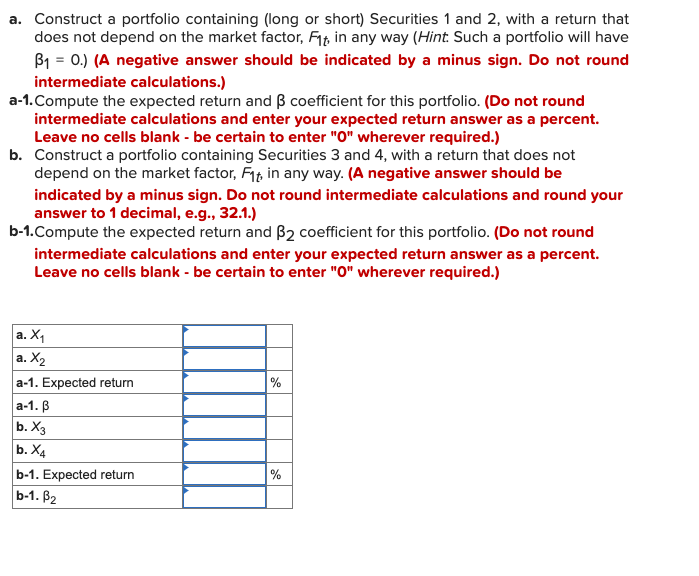

Construct a portfolio containing long or short Securities and with a return that does not depend on the market factor, Ft in any way Hint: Such a portfolio will have beta A negative answer should be indicated by a minus sign. Do not round intermediate calculations.

a Compute the expected return and beta coefficient for this portfolio. Do not round intermediate calculations and enter your expected return answer as a percent. Leave no cells blank be certain to enter wherever required.

b Construct a portfolio containing Securities and with a return that does not depend on the market factor, Ft in any way. A negative answer should be indicated by a minus sign. Do not round intermediate calculations and round your answer to decimal, eg

b Compute the expected return and beta coefficient for this portfolio. Do not round intermediate calculations and enter your expected return answer as a percent. Leave no cells blank be certain to enter wherever required.a Construct a portfolio containing long or short Securities and with a return that

does not depend on the market factor, in any way Hint Such a portfolio will have

A negative answer should be indicated by a minus sign. Do not round

intermediate calculations.

a Compute the expected return and coefficient for this portfolio. Do not round

intermediate calculations and enter your expected return answer as a percent.

Leave no cells blank be certain to enter wherever required.

b Construct a portfolio containing Securities and with a return that does not

depend on the market factor, in any way. A negative answer should be

indicated by a minus sign. Do not round intermediate calculations and round your

answer to decimal, eg

bCompute the expected return and coefficient for this portfolio. Do not round

intermediate calculations and enter your expected return answer as a percent.

Leave no cells blank be certain to enter wherever required.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Jeff Madura, Roland Fox

4th Edition

147372550X, 9781473725508